Understanding and accurately completing your W-4 form is a cornerstone of effective personal finance. This seemingly simple document, often handled with a quick, unthinking check-the-box mentality, holds significant power over your paycheck and your overall financial well-being throughout the year. Claiming the correct withholding is not about “getting more money back” in the traditional sense; it’s about ensuring you’re not overpaying or underpaying taxes to the IRS throughout the year, and optimizing your cash flow. This article will delve into the intricacies of the W-4, guiding you through the decisions that impact your take-home pay and your tax liability.

Understanding the Fundamentals of Withholding

Before diving into the specifics of claiming, it’s crucial to grasp the underlying principles of tax withholding. When you start a new job or experience a significant life change, you’ll be asked to fill out a W-4, Employee’s Withholding Certificate. This form tells your employer how much federal income tax to withhold from each paycheck. The goal is to have your withholdings closely match your actual tax liability for the year.

How Federal Income Tax Withholding Works

The U.S. federal income tax system is a pay-as-you-go system. This means that taxes are collected throughout the year via withholding from wages and estimated tax payments. Your employer uses the information you provide on the W-4 to calculate the amount of income tax to remit to the IRS on your behalf. This calculation is based on your filing status (single, married filing jointly, etc.), the number of dependents you claim, and any additional income or deductions you anticipate.

The Purpose of the W-4 Form

The W-4 form serves as a vital communication tool between you and your employer, and ultimately, the IRS. It allows you to inform your employer about your personal tax situation so they can adjust the amount of tax withheld from your wages. If you claim fewer allowances (which are now represented by dollar amounts based on various factors on the updated W-4), more tax will be withheld. Conversely, claiming more allowances results in less tax being withheld. The updated W-4, implemented in 2020, shifted away from the traditional “allowances” system to a more detailed approach, requiring you to account for various income sources, deductions, and credits more explicitly. This aims to provide greater accuracy and reduce the likelihood of significant over- or under-withholding.

Overpaying vs. Underpaying: The Financial Implications

Overpaying: If you claim too many withholding allowances (or provide information that leads to excessive withholding), you’ll essentially be giving the government an interest-free loan throughout the year. While you will receive a tax refund, this money could have been in your bank account, earning interest, invested, or used to pay down debt. This can significantly impact your monthly cash flow and limit your ability to meet short-term financial goals.

Underpaying: Conversely, if you claim too few allowances (or provide information that leads to insufficient withholding), you may owe taxes when you file your annual return. The IRS charges penalties and interest on underpayments, which can add a substantial financial burden. It’s crucial to avoid this scenario, as penalties can quickly erode any perceived benefit of lower withholdings.

Decoding the W-4: Key Sections and Your Choices

The modern W-4 form, with its emphasis on accuracy, requires a more thoughtful approach to completion. It’s divided into several sections, each designed to capture specific aspects of your financial life that influence your tax liability.

Step 1: Personal Information

This is the foundational step where you identify yourself and your tax situation.

Filing Status

- Single or Married Filing Separately: If you are unmarried, or married but choose to file your taxes separately from your spouse, you’ll select this option. This status generally results in higher tax rates compared to married filing jointly.

- Married Filing Jointly: If you are married and choose to file one tax return with your spouse, you’ll select this. This status often leads to lower tax rates as it allows for income splitting and more favorable tax brackets.

- Qualifying Widow(er): This status is for individuals who were married, their spouse has passed away, and they have a dependent child. It allows them to use the same tax rates and standard deduction as a married couple filing jointly for a limited period.

- Head of Household: This status is for unmarried individuals who pay more than half the cost of keeping up a home for a qualifying child. It offers a lower tax rate than single filers and a larger standard deduction.

Social Security Number

Accurately providing your Social Security number (SSN) for yourself and your spouse (if applicable) is critical for proper tax identification and processing.

Step 2: Multiple Jobs or Spouse Works

This section is designed to address situations where income isn’t solely from one source, which can significantly impact withholding.

If You Have More Than One Job or Your Spouse Works

The goal here is to ensure that the combined tax withheld from all your income sources is sufficient to cover your total tax liability. If you have a second job, or if your spouse earns income, simply applying the standard withholding to each income source will likely result in under-withholding because each job is treated in isolation, and income from multiple sources pushes you into higher tax brackets.

Using the IRS Estimator Tool (Recommended)

The most accurate way to complete Step 2 is to use the IRS Tax Withholding Estimator. This online tool allows you to input information about all your income sources, deductions, and credits to calculate the precise amount of withholding needed. While it requires a bit more effort, it’s the most reliable method to avoid underpayment penalties.

Alternative Methods for Step 2

If you choose not to use the IRS estimator, you can also:

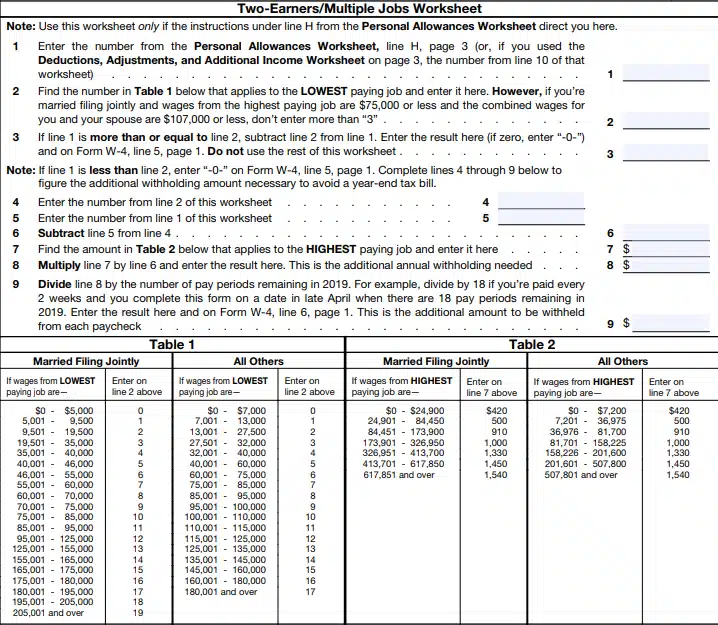

- Use the Table on Page 3 of Form W-4: This method involves looking up the combined income of both you and your spouse (or your multiple jobs) in a provided table and using the corresponding withholding adjustment. This can be less precise than the estimator.

- Check the Box in Step 2(c) (if eligible): This option is available if you are single and have only one job, or if you are married filing jointly and you and your spouse have similar incomes and only one job each. It generally results in higher withholding to account for the possibility of higher tax brackets. However, it’s crucial to understand that this is a simplification and may not be accurate for all situations.

Step 3: Claim Dependents

This section allows you to account for tax credits you may be eligible for related to your dependents.

Calculating the Amount for Dependents

For each qualifying child (under age 17), you can claim a $2,000 tax credit. For other qualifying dependents (e.g., a dependent parent), you can claim a $500 tax credit. The amount you enter in Step 3 is the total dollar amount of these credits you are claiming.

What Constitutes a Qualifying Dependent?

The IRS has specific rules for who qualifies as a dependent, which typically involve factors like age, relationship to you, residency, and financial support provided. It’s essential to refer to IRS Publication 972, “Child Tax Credit and Additional Child Tax Credit,” and Publication 501, “Dependents, Standard Deduction, and Filing Information,” for precise definitions.

Step 4: Other Adjustments

This section is for fine-tuning your withholding based on other aspects of your financial life.

(a) Other Income

If you have income from sources other than your main job (e.g., freelance work, interest, dividends, retirement income), you can list that income here. This ensures that the tax on this extra income is accounted for in your withholding. The idea is to add this income to your taxable income for withholding purposes, effectively increasing the amount withheld from your regular paychecks.

(b) Deductions

This is where you can claim deductions beyond the standard deduction. If you anticipate having itemized deductions (e.g., mortgage interest, state and local taxes up to the limit, medical expenses exceeding a certain percentage of your AGI, charitable contributions) that will exceed the standard deduction for your filing status, you can use this section. By entering your estimated total annual deductions here, your employer will adjust your withholding to reflect these deductions, thus reducing the amount of tax withheld.

(c) Extra Withholding

This is a catch-all for any additional tax you wish to have withheld from each paycheck. This could be for various reasons, such as:

- Ensuring you don’t owe: If you’ve historically owed a significant amount at tax time and want to guarantee a refund or break even.

- Specific tax obligations: You might have specific tax liabilities you want to pre-pay through withholding, such as taxes on certain investments or self-employment income.

- Simplifying tax payments: Some individuals prefer to have more withheld to avoid the hassle of making estimated tax payments throughout the year.

Strategic Withholding: Optimizing Your Financial Workflow

Claiming the right amount of withholding isn’t just about avoiding penalties; it’s a strategic financial decision that can significantly impact your ability to manage your money effectively.

The Case for Aiming for Zero or a Small Refund

The ideal scenario, from a cash flow perspective, is to have your withholding accurately reflect your tax liability, resulting in zero tax owed or a very small refund. This means you are not overpaying the government throughout the year and instead have access to all your earned income.

Maximizing Your Monthly Cash Flow

When you over-withhold, you’re effectively deferring income that could be used for immediate financial needs or opportunities. Having more money in your checking account each month allows for greater flexibility in budgeting, saving, and investing. It can help you cover unexpected expenses, meet debt obligations more easily, or simply provide a greater sense of financial security.

Opportunities for Investment and Debt Reduction

The money you might receive as a large tax refund could be put to work much sooner if it were in your paycheck. Consider the power of compounding: investing a lump sum throughout the year, even small amounts, can yield greater returns than receiving a large refund and investing it all at once. Similarly, using excess funds to make extra principal payments on debt can save you significant interest over time.

When a Larger Refund Might Be Desirable

While aiming for zero refund is generally the financially prudent approach, there are specific circumstances where a larger refund might be intentionally sought.

Forced Savings Mechanism

For individuals who struggle with disciplined saving, a larger tax refund can act as a form of forced savings. If you know you’re prone to overspending, having a significant refund come tax time can provide a substantial boost to your savings goals, whether for a down payment on a house, a major purchase, or long-term investment.

Planning for Specific Large Expenses

Sometimes, a large tax refund can be strategically planned for a specific, anticipated large expense. For example, if you know you’ll need a significant amount of cash for tuition payments, a major home renovation, or a substantial investment in the coming year, aiming for a refund can help ensure that funds are available.

Regularly Reviewing and Adjusting Your W-4

Your tax situation is not static. Life events can dramatically alter your withholding needs. It’s crucial to treat your W-4 as a living document.

Common Life Events Triggering a W-4 Review

- Marriage or Divorce: These significant life events directly impact your filing status and potentially your spouse’s income.

- Birth or Adoption of a Child: This affects your dependent claims and potential tax credits.

- Change in Employment Status: Starting a new job, taking a second job, or your spouse starting or leaving a job necessitates a W-4 review.

- Significant Change in Income: A substantial raise, bonus, or loss of income from a side hustle requires recalculation.

- Major Changes in Deductions or Credits: If you anticipate significant changes in your deductible expenses or eligibility for tax credits, your withholding should be adjusted.

The Importance of an Annual Review

Even without major life events, it’s wise to review your W-4 annually, preferably before the end of the tax year. This allows you to make any necessary adjustments to ensure you’re on track for the current tax year and to prepare for the next.

Tools and Resources for Accurate Withholding

The IRS provides valuable resources to help taxpayers navigate the W-4 and their tax obligations.

The IRS Tax Withholding Estimator

As mentioned, this is the gold standard for determining your correct withholding. It’s available on the IRS website and is regularly updated to reflect current tax laws.

IRS Publications

Various IRS publications offer detailed explanations of tax laws, deductions, credits, and how to complete tax forms. Publications like Pub. 17 (Your Federal Income Tax), Pub. 505 (Tax Withholding and Estimated Tax), and the instructions for Form W-4 itself are invaluable resources.

By taking the time to understand and correctly complete your W-4, you are taking a proactive step towards better financial management. It’s an investment in your financial health that pays dividends throughout the year and at tax time. Don’t let this critical document be an afterthought; let it be a tool that empowers your financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.