Navigating the world of travel insurance, especially when embarking on a cruise, can feel like deciphering a complex map. For many, Royal Caribbean represents the pinnacle of cruise experiences, offering voyages to breathtaking destinations. However, the allure of sun-drenched beaches and exotic ports of call is best enjoyed with the peace of mind that comes from understanding your coverage. This article delves deep into the intricacies of Royal Caribbean’s travel insurance, dissecting what it covers, its limitations, and how it functions as a crucial component of your vacation planning. Understanding your insurance policy isn’t just about financial protection; it’s about ensuring your journey is as seamless and stress-free as possible.

Understanding the Core Components of Cruise Insurance

Cruise insurance, like any other form of insurance, operates on the principle of risk mitigation. For a cruise, the risks are multifaceted, ranging from unforeseen medical emergencies to disruptions in travel plans. Royal Caribbean, in partnership with its insurance providers, aims to address these potential pitfalls by offering a comprehensive suite of coverages designed specifically for the cruise environment. It’s essential to recognize that while Royal Caribbean facilitates the insurance offering, the actual policy is underwritten by a third-party insurance company. This distinction is vital, as the specifics of coverage, claims processes, and customer service will be dictated by that underwriter.

Medical Emergencies and Healthcare at Sea

One of the most critical aspects of any travel insurance, and particularly for a cruise, is the coverage for medical emergencies. When you’re at sea, often far from land-based hospitals, access to immediate and adequate medical care is paramount. Royal Caribbean’s insurance typically includes coverage for:

Emergency Medical Expenses

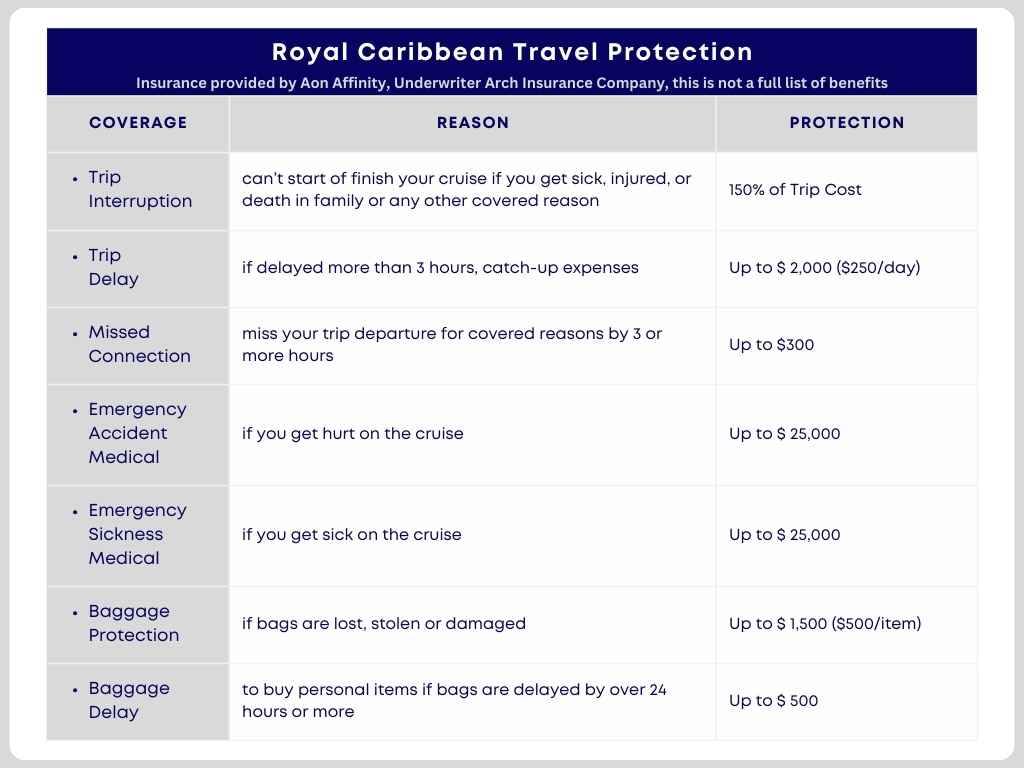

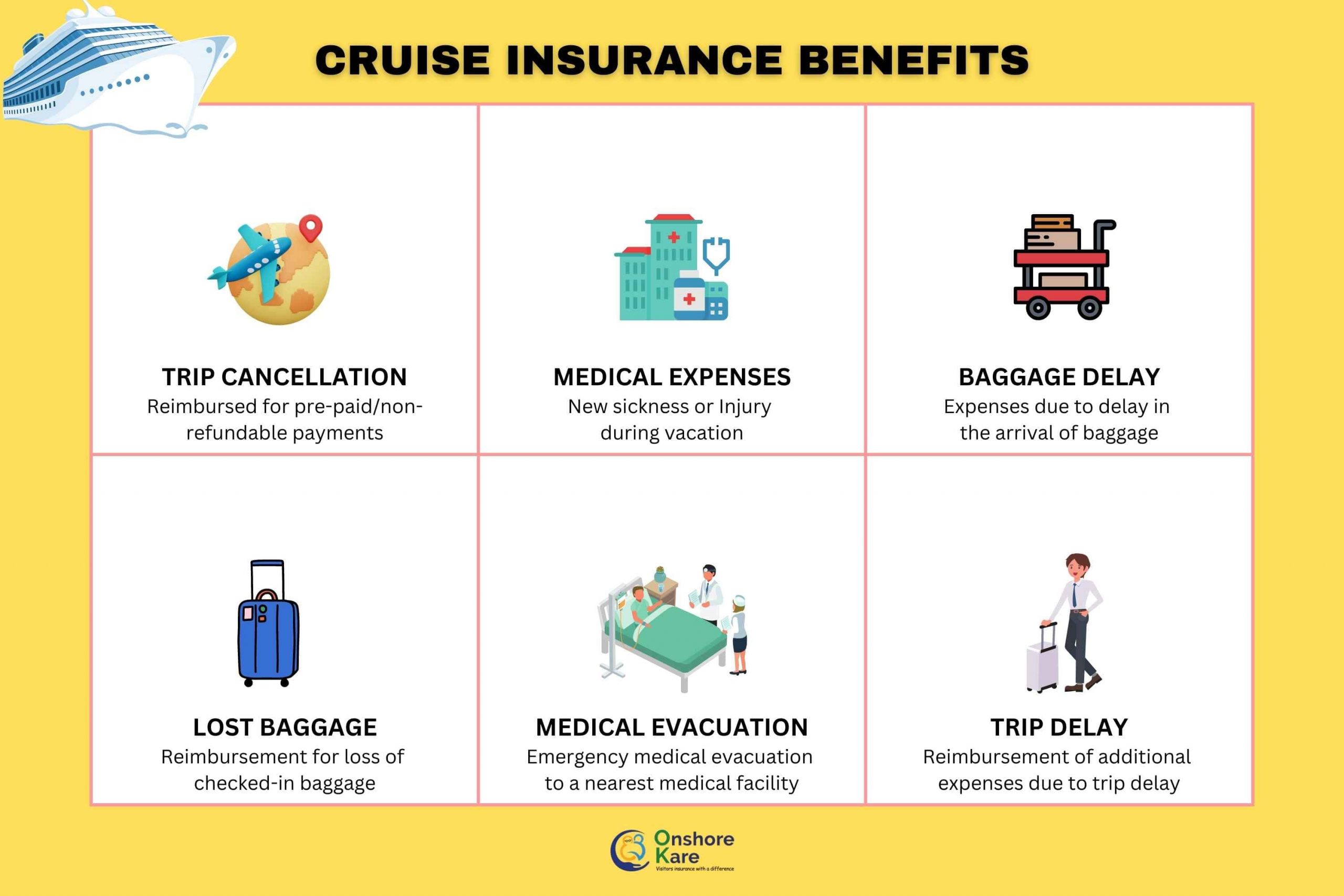

This is arguably the most crucial benefit. If you fall ill or suffer an injury during your cruise, the policy will generally cover expenses incurred for medical treatment on board the ship or at a shore-based facility if deemed necessary by a physician. This can include doctor’s consultations, prescription medications, diagnostic tests, and hospitalization. The cost of medical care on cruise ships can be substantial, making this coverage indispensable. It’s important to note that pre-existing conditions might have specific stipulations, which we will explore later.

Emergency Medical Evacuation

In situations where the medical facilities on board are insufficient to treat your condition, or if you require specialized care not available at sea, emergency medical evacuation becomes vital. This coverage typically handles the cost of transporting you from the ship to the nearest adequate medical facility on land. This can involve helicopters, air ambulances, or other specialized transport, which are incredibly expensive. Without this coverage, the financial burden of such an evacuation could be devastating.

Repatriation of Remains

While a somber consideration, it’s a necessary part of comprehensive insurance. In the unfortunate event of a traveler’s death during the cruise, this benefit covers the cost of returning the deceased’s remains to their home country. This can be a complex and expensive logistical process, and having it covered provides significant relief to grieving families.

Travel Interruption and Cancellation

Beyond health concerns, travel plans can be disrupted by a myriad of unforeseen circumstances. Cruise insurance aims to mitigate the financial losses associated with these disruptions.

Trip Cancellation

This coverage allows you to recoup non-refundable expenses if you need to cancel your trip before its departure due to a covered reason. Covered reasons often include severe illness or injury to yourself, a traveling companion, or a close family member; death of a covered person; jury duty; military reassignment; and certain natural disasters affecting your destination. Understanding what constitutes a “covered reason” is critical for successful claims.

Trip Interruption

If your trip is cut short due to a covered reason after you have already departed, trip interruption coverage can help reimburse you for the unused portion of your prepaid, non-refundable trip expenses. It can also cover additional transportation costs to return home or rejoin your cruise if you were temporarily separated due to a covered event. For instance, if you miss your embarkation port due to a flight delay and need to catch up with the ship at a later port, this coverage can be invaluable.

Travel Delay

Missed connections, flight cancellations, or other unforeseen travel delays can lead to unexpected expenses such as meals, accommodation, and essential toiletries. Travel delay coverage typically reimburses these incidental costs incurred while waiting for your journey to resume. The policy will usually specify a minimum number of hours you must be delayed before this coverage kicks in.

Beyond the Basics: Additional Coverages and Considerations

While medical and cancellation coverages form the bedrock of cruise insurance, comprehensive policies often extend to other areas, offering a more robust safety net. It’s also crucial to understand certain limitations and exclusions that are standard across most insurance policies.

Baggage and Personal Effects

Losing luggage or having personal belongings stolen or damaged during a trip can be a significant inconvenience and financial loss. Royal Caribbean’s insurance often includes coverage for lost, stolen, or damaged baggage and personal effects.

Lost or Damaged Luggage

This benefit typically reimburses you for the cost of replacing essential items if your checked or carry-on luggage is lost, stolen, or damaged by the common carrier (e.g., airline, cruise line). There are usually limits on the maximum payout per item and per bag, as well as a total policy limit.

Baggage Delay

If your luggage is delayed by the carrier for a specified period (e.g., 12 or 24 hours), this coverage can reimburse you for the purchase of essential items you need while waiting for your bags to arrive. This is particularly useful for replacing toiletries, clothing, and other immediate necessities.

Accidental Death and Dismemberment (AD&D)

This is an optional, but often included, benefit that provides a lump-sum payment in the event of death or severe dismemberment (loss of limbs or eyesight) resulting directly from an accident during your trip. The payout amount is typically a fixed sum, with the amount varying based on the severity of the injury.

Rental Car Damage and Other Travel-Related Expenses

Some policies may offer additional ancillary benefits, such as coverage for damage to a rental car (though this is often secondary to your own auto insurance or the rental company’s insurance), or even coverage for identity theft resolution services. These are less common but can add further value to the overall protection.

Understanding Exclusions and Limitations

It’s imperative to read the fine print of your insurance policy. All insurance policies contain exclusions, which are specific circumstances or events that the policy will not cover. Common exclusions for travel insurance include:

- Pre-existing Medical Conditions: Many policies have a look-back period for pre-existing conditions. If you have a medical condition that existed before purchasing the insurance, and it flares up during the trip, coverage may be denied unless you specifically purchased a pre-existing condition waiver or have a policy that covers them.

- High-Risk Activities: Injuries sustained while participating in extreme sports or hazardous activities (e.g., skydiving, scuba diving beyond a certain depth, mountain climbing) are often excluded.

- Acts of War and Terrorism: While some policies may offer limited coverage for certain events, widespread acts of war or terrorism are typically excluded.

- Intoxication or Substance Abuse: Injuries or illnesses directly resulting from being under the influence of alcohol or drugs are generally not covered.

- Unforeseen Events Not Listed: The policy will specify what constitutes a “covered reason” for cancellation or interruption. Events not explicitly listed, even if they cause significant inconvenience, may not be covered.

Navigating Claims and Making the Most of Your Coverage

Even with comprehensive insurance, the claims process can sometimes feel daunting. Understanding how to file a claim and what documentation is required can streamline the process and increase your chances of a successful outcome.

The Claims Process: Step-by-Step

While the specific steps can vary slightly depending on the insurance provider, a general claims process for Royal Caribbean insurance typically involves:

- Immediate Notification: If a covered event occurs, such as a medical emergency or trip interruption, it’s crucial to notify the insurance provider as soon as possible. Many policies require notification within a specific timeframe.

- Gathering Documentation: This is the most critical step. You will need to collect all relevant documentation to support your claim. This includes:

- For Medical Claims: Itemized bills from hospitals or doctors, medical reports detailing the diagnosis and treatment, and proof of payment.

- For Trip Cancellation/Interruption: Proof of non-refundable expenses (e.g., booking confirmations, receipts), documentation of the covered reason for cancellation or interruption (e.g., doctor’s note, death certificate, airline delay notification).

- For Baggage Claims: Baggage tag receipts, a written report from the airline or cruise line detailing the lost or damaged luggage, and receipts for the damaged or lost items.

- Submitting the Claim Form: Most insurance providers have online claim forms or downloadable versions. Ensure you fill out the form completely and accurately, attaching all supporting documents.

- Review and Processing: The insurance company will review your claim and supporting documentation. They may contact you for further information or clarification.

- Payment or Denial: Once the review is complete, the insurance company will either approve your claim and issue payment or deny your claim with a written explanation.

Tips for a Smoother Claims Experience

- Read Your Policy Before You Travel: Familiarize yourself with the coverage details, exclusions, and claims process before your trip.

- Keep Meticulous Records: Store all travel documents, receipts, and correspondence in a safe and organized manner.

- Take Photos: If your luggage is damaged, take clear photos of the damage.

- Be Honest and Accurate: Provide truthful and accurate information on your claim form and to the insurance company.

- Understand Your Deductible: Many policies have a deductible, which is the amount you are responsible for paying before the insurance coverage kicks in.

- Contact Customer Service: If you are unsure about any aspect of the claims process, don’t hesitate to contact the insurance provider’s customer service department.

In conclusion, Royal Caribbean’s travel insurance is designed to provide a comprehensive safety net for your vacation. By understanding the core components, the additional coverages, and the important limitations, you can make an informed decision about securing the right policy. This proactive approach to understanding your insurance coverage transforms a potential worry into a layer of security, allowing you to fully immerse yourself in the incredible experiences that a Royal Caribbean cruise has to offer. Remember, peace of mind is an invaluable part of any journey, and a well-understood insurance policy is a key contributor to that.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.