The journey of buying or selling a property is often punctuated by a term that signals a significant shift: “under contract.” This phrase, while seemingly straightforward, carries a weight of financial implications, legal commitments, and potential opportunities for all parties involved. Understanding precisely what it signifies is crucial for anyone navigating the real estate market, as it marks a transition from active listing to a more committed phase of the transaction. This article delves into the multifaceted meaning of “under contract” within the realm of real estate finance, exploring the financial safeguards, potential pitfalls, and strategic considerations that arise during this pivotal stage.

The Financial Crossroads: What “Under Contract” Truly Entails

When a property is “under contract,” it means that a buyer and seller have formally agreed upon the terms of the sale, and this agreement has been formalized through a legally binding contract, typically referred to as a Purchase Agreement or Sale and Purchase Agreement. From a financial perspective, this signifies a critical juncture where earnest money deposits become relevant, financing contingencies are actively pursued, and the valuation of the property becomes more concrete.

Earnest Money: The Buyer’s Commitment and Seller’s Security

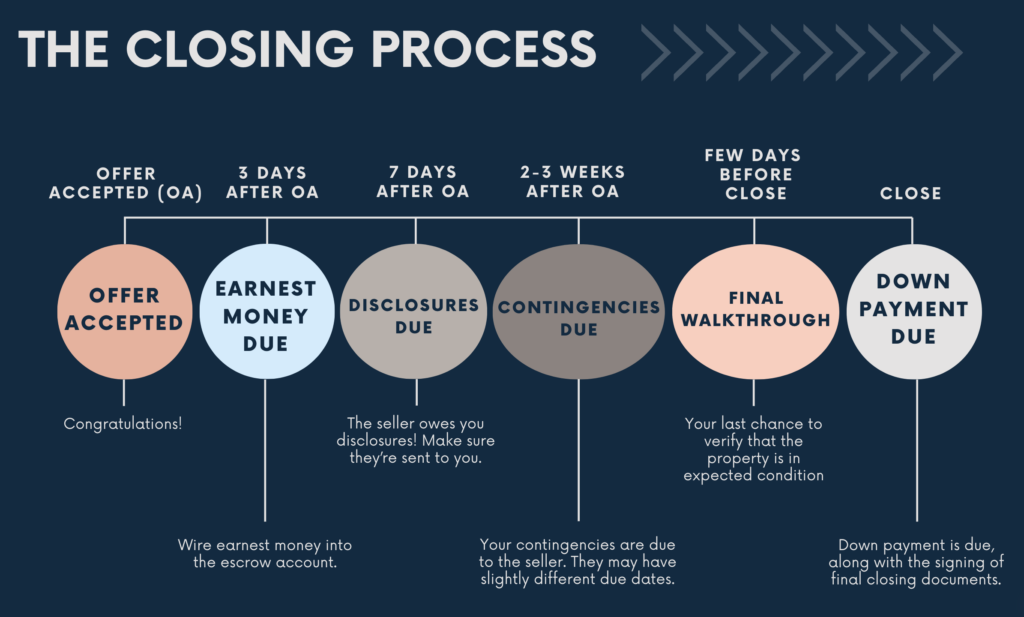

The initial financial commitment from a buyer to demonstrate their serious intent to purchase is the earnest money deposit. This sum, typically a percentage of the purchase price (often 1-5%), is held in an escrow account by a neutral third party, such as an escrow company or attorney. Its presence signifies the buyer’s good faith and provides a degree of financial security for the seller.

Understanding Escrow and Its Role

Escrow is a vital financial mechanism in real estate transactions. The escrow holder acts as a fiduciary, safeguarding the earnest money deposit and other important documents until all conditions of the contract are met. This ensures that neither party can unilaterally withdraw from the deal without incurring financial penalties, as outlined in the contract. The funds remain in escrow until closing, at which point they are applied towards the buyer’s down payment or closing costs.

Forfeiture of Earnest Money: The Financial Stakes

The contract will meticulously detail the conditions under which the earnest money deposit can be forfeited. Typically, if the buyer defaults on the agreement without a valid contingency-based reason, the seller may be entitled to retain the earnest money. This serves as compensation for the seller’s time off the market and potential losses incurred due to the failed transaction. Conversely, if the seller defaults, they may be obligated to return the earnest money and potentially face additional financial penalties.

Contingencies: The Financial Safety Nets and Potential Deal Breakers

Real estate contracts are rarely unconditional. Contingencies are clauses that allow either the buyer or seller to withdraw from the contract without penalty if certain conditions are not met. These contingencies are primarily financial in nature and are designed to protect the buyer from unforeseen circumstances that could jeopardize their ability to complete the purchase.

Financing Contingency: Securing the Necessary Funds

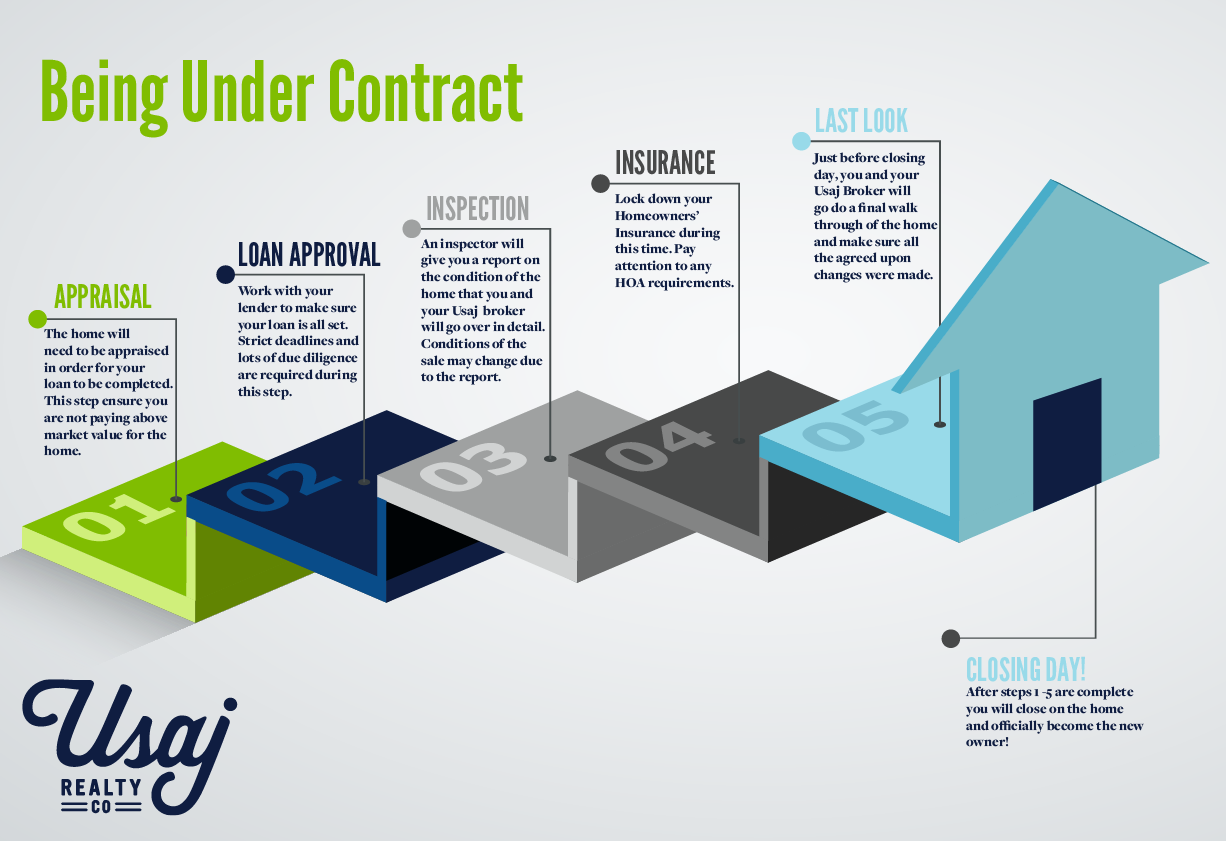

Perhaps the most common and crucial contingency is the financing contingency. This clause allows the buyer a specified period to secure a mortgage loan that will cover the remaining purchase price. If the buyer is unable to obtain the necessary financing within the agreed-upon timeframe, despite making a diligent effort, they can terminate the contract and receive their earnest money back. This contingency is paramount for buyers who are not paying cash, as it prevents them from being locked into a purchase they cannot afford.

The Loan Approval Process: A Financial Gauntlet

The period under contract is when the buyer’s mortgage application undergoes rigorous scrutiny by the lender. This involves extensive financial documentation review, property appraisals, and credit checks. The lender’s commitment to providing the loan is the lynchpin of the financing contingency. If the appraisal comes in lower than the purchase price, it can trigger a renegotiation or even a cancellation of the deal, directly impacting the financial viability of the transaction.

Appraisal Contingency: Verifying the Property’s Value

Closely linked to the financing contingency is the appraisal contingency. This clause ensures that the property is valued by an independent appraiser at or above the agreed-upon purchase price. If the appraisal reveals a significantly lower value, the buyer has several options. They can attempt to renegotiate the purchase price with the seller, pay the difference in cash, or withdraw from the contract and have their earnest money returned. This contingency protects buyers from overpaying for a property.

Inspection Contingency: Uncovering Potential Financial Liabilities

The inspection contingency allows the buyer to conduct a thorough professional inspection of the property. If the inspection uncovers significant structural issues, major repairs, or hidden defects, the buyer can request the seller to make the repairs, offer a credit towards repairs at closing, or, if the issues are substantial and unresolved, withdraw from the contract. This contingency is a financial safeguard, preventing buyers from inheriting costly repair bills shortly after purchase.

The Role of Title Insurance and Surveys: Financial Protection and Clarity

Beyond the immediate financial commitments of the buyer and seller, being under contract also triggers important financial protections related to the property’s title and boundaries.

Title Search and Insurance: Securing Ownership Rights

A critical step once a property is under contract is the ordering of a title search. This involves examining public records to ensure that the seller has clear and marketable title to the property, free from liens, encumbrances, or other claims that could affect ownership. A title company then issues title insurance, a form of indemnity insurance that protects the buyer and their lender against financial loss arising from defects in the title. This is a crucial financial protection, as it ensures the buyer’s ownership rights are secure.

Understanding Liens and Encumbrances

Liens are claims against a property for unpaid debts (e.g., mortgages, tax liens, mechanic’s liens). Encumbrances are restrictions on the use or transfer of a property (e.g., easements, deed restrictions). The title search aims to identify any such issues. If significant liens or encumbrances are found that cannot be resolved by the seller, it can prevent the transaction from closing and lead to a forfeiture of earnest money for the buyer, highlighting the financial importance of a clear title.

Property Surveys: Defining Financial Boundaries

In some transactions, particularly those involving larger parcels of land or properties with complex boundary lines, a property survey may be required. A survey definitively establishes the legal boundaries of the property. This can have financial implications, especially if the survey reveals encroachments by neighboring properties or if the actual lot size differs significantly from what was advertised. Understanding these boundaries ensures the buyer is acquiring exactly what they believe they are purchasing.

Moving Towards Closing: Financial Preparations and Closing Costs

Once all contingencies are satisfied or waived, the transaction progresses towards the final stage: closing. This is where the financial transfer of ownership officially takes place, and a clear understanding of closing costs is essential.

The Closing Disclosure: A Comprehensive Financial Statement

At least three business days before closing, buyers receive a Closing Disclosure (CD). This document, mandated by the Consumer Financial Protection Bureau (CFPB), provides a detailed breakdown of all the financial aspects of the transaction. It outlines the loan terms, monthly payments, and all the fees and charges associated with the sale, from loan origination fees and appraisal costs to title insurance premiums, recording fees, and property taxes.

Understanding and Verifying Closing Costs

It is imperative for buyers to carefully review the Closing Disclosure and compare it to the Loan Estimate they initially received from their lender. Any significant discrepancies should be addressed immediately with the lender or closing agent. Closing costs can add a substantial amount to the overall cost of purchasing a home, typically ranging from 2% to 5% of the loan amount. Understanding these costs beforehand is a key financial planning element.

Negotiating Closing Costs

While many closing costs are standard, some are negotiable. Buyers can often negotiate with their agents, lenders, or title companies on certain fees. Additionally, sellers may agree to contribute towards the buyer’s closing costs as part of the purchase agreement, especially in a buyer’s market. This can significantly reduce the upfront financial burden for the buyer.

The Final Walk-Through: A Last Financial Check

Prior to closing, buyers typically conduct a final walk-through of the property. This is not just a formality; it’s a crucial financial check to ensure that the property is in the same condition as when the contract was signed and that any agreed-upon repairs have been completed. It also confirms that all included fixtures and appliances are still present. This final inspection acts as a last financial safeguard against any last-minute issues.

Beyond the Transaction: Long-Term Financial Considerations of Being Under Contract

The financial implications of being under contract extend beyond the immediate transaction. The period leading up to closing, while focused on satisfying contractual obligations, also provides an opportunity for buyers to refine their long-term financial planning for homeownership.

Budgeting for Homeownership: Beyond the Mortgage Payment

Once under contract, buyers should shift their financial focus from the purchase price to the ongoing costs of homeownership. This includes not just the monthly mortgage payment, but also property taxes, homeowner’s insurance, potential homeowner’s association (HOA) fees, utilities, and regular maintenance and repair expenses. Being under contract provides a concrete timeframe to solidify these long-term financial projections.

The Impact of Property Taxes and Insurance Premiums

Property taxes and homeowner’s insurance premiums are significant ongoing expenses. The exact amounts will be detailed on the Closing Disclosure, allowing buyers to accurately incorporate them into their monthly budgets. Understanding how these costs can fluctuate over time is also a crucial aspect of long-term financial planning.

Homeowner’s Insurance: Protecting Your Financial Investment

Securing homeowner’s insurance is typically a requirement for obtaining a mortgage and is essential for protecting the buyer’s significant financial investment. The lender will need proof of insurance before releasing funds at closing. The cost of this insurance will be factored into the monthly escrow payments, ensuring that the property is adequately protected against damage or loss.

Home Maintenance and Repair Funds: Anticipating Future Expenses

Properties, regardless of their age or condition, will eventually require maintenance and repairs. Being under contract offers a valuable opportunity for buyers to begin setting aside funds specifically for these future expenses. This proactive financial approach can prevent unexpected large expenditures from becoming financial burdens down the line, ensuring the long-term financial health of their homeownership.

In conclusion, the term “under contract” in real estate signifies a crucial transition, marked by legally binding agreements and significant financial commitments. From the earnest money deposit that solidifies buyer intent to the crucial contingencies that act as financial safety nets, every aspect of this phase is deeply intertwined with financial considerations. For both buyers and sellers, understanding these implications, diligently preparing for closing, and looking ahead to the long-term financial responsibilities of homeownership are paramount to a successful and financially sound real estate transaction.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.