The world of credit cards can often feel like navigating a complex financial labyrinth, filled with jargon and intricate details that can leave even the savviest consumer feeling overwhelmed. Among the most fundamental, yet often misunderstood, terms is “Purchase APR.” Understanding this seemingly simple acronym is crucial for anyone who uses a credit card, as it directly impacts the cost of borrowing money. This article will demystify the Purchase APR, breaking down its meaning, how it’s calculated, and its significant implications for your personal finances.

Understanding the Core Concept of Purchase APR

At its heart, the Purchase Annual Percentage Rate (APR) is the interest rate that a credit card issuer charges you on the outstanding balance of purchases you make. It’s the annual cost of carrying a balance from one billing cycle to the next. It’s important to distinguish this from other APRs that might appear on your credit card statement, such as balance transfer APRs or cash advance APRs, which often have different rates and terms.

What Exactly Does “Annual Percentage Rate” Mean?

The term “Annual Percentage Rate” is designed to provide a standardized way of comparing the cost of borrowing across different credit products. While it’s stated as an annual rate, the interest it represents is typically calculated and applied on a daily or monthly basis. This means that even if you pay off your balance before the year is out, the APR still dictates the rate at which interest accrues.

The Difference Between Purchase APR and Other APRs

Credit cards often come with a menu of APRs, each applying to different types of transactions. The most common ones to be aware of include:

- Purchase APR: This is the rate applied to purchases you make with your credit card. It’s the most frequently used APR for most cardholders.

- Balance Transfer APR: This is the rate charged on balances you transfer from another credit card to this one. Often, introductory balance transfer APRs are 0% for a specific period, after which a higher standard rate applies.

- Cash Advance APR: This is the rate applied to cash withdrawals made using your credit card. Cash advance APRs are typically higher than purchase APRs, and interest often begins to accrue immediately with no grace period.

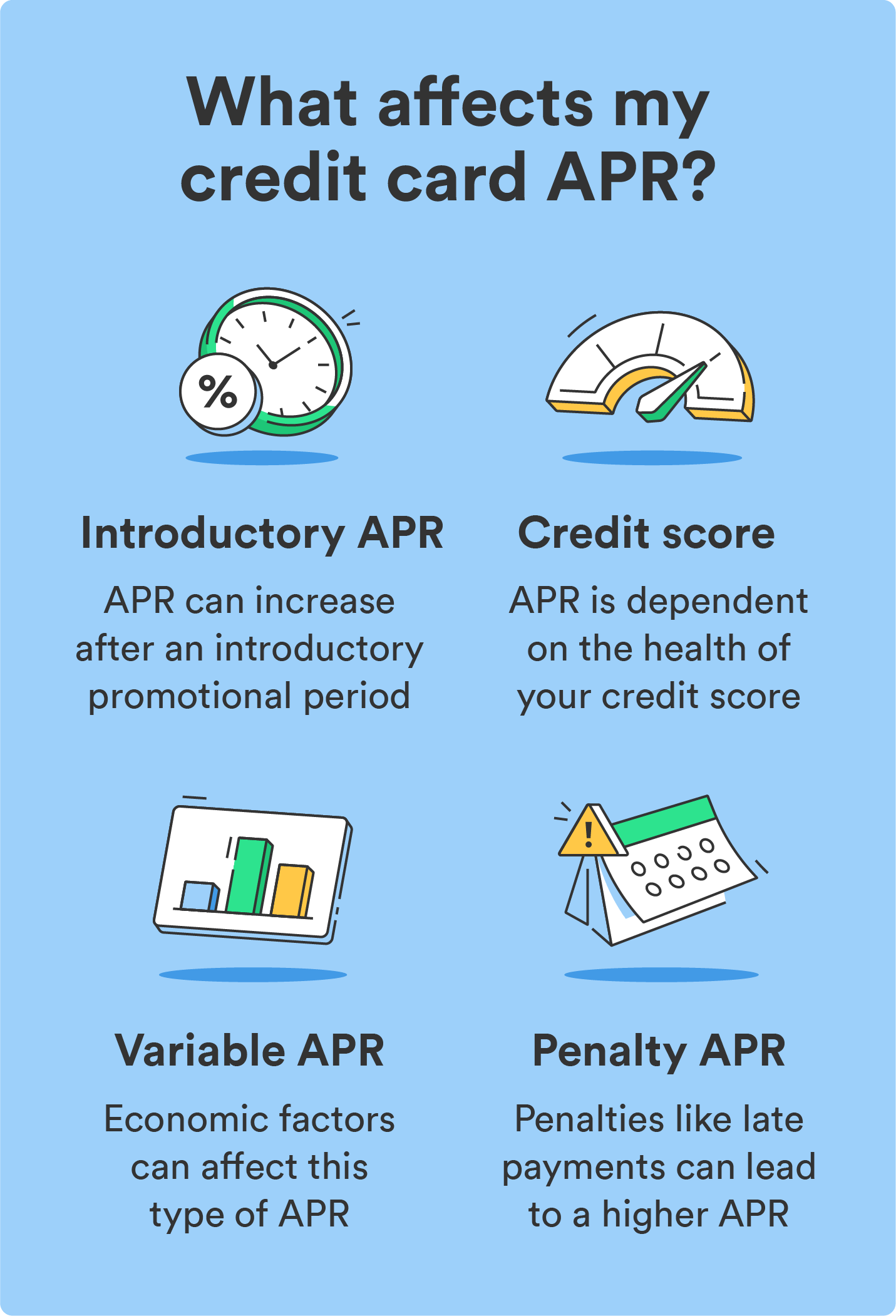

- Penalty APR: This is a punitive rate that can be applied if you miss a payment or violate other terms of your credit card agreement. Penalty APRs are usually significantly higher than standard APRs and can remain in effect for an extended period.

Understanding these distinctions is paramount. For instance, carrying a balance on purchases might be manageable at a certain purchase APR, but the same balance would be far more expensive if it were a cash advance.

How Purchase APR is Calculated and Applied

The calculation and application of your purchase APR might seem complex, but it’s based on a straightforward methodology. The issuer uses your creditworthiness to determine your specific APR, and then applies it to your outstanding balance.

The Role of Your Credit Score in Determining Your APR

When you apply for a credit card, the issuer will assess your credit history and credit score. A higher credit score generally indicates a lower credit risk to the lender, which typically translates into a lower purchase APR. Conversely, individuals with lower credit scores may be offered cards with higher APRs, reflecting the increased risk for the issuer. Credit card companies use your credit score as a primary indicator of your ability and willingness to repay borrowed money. Lenders see a higher credit score as a sign of financial responsibility.

Daily Periodic Rate and its Impact

While your purchase APR is an annual rate, the interest you are actually charged is calculated on a daily basis. This is known as the Daily Periodic Rate (DPR). To find your DPR, you divide your purchase APR by 365 (or sometimes 360, depending on the issuer’s practice).

For example, if your purchase APR is 18%, your DPR would be:

18% / 365 = 0.0493% (approximately)

This daily rate is then multiplied by your average daily balance for that billing cycle. The sum of these daily interest charges over the billing cycle is added to your account. This daily accrual means that even if you plan to pay off your balance, interest is accumulating from the moment you make a purchase, unless you are within a grace period.

The Significance of the Grace Period

A crucial element related to purchase APR is the grace period. This is a timeframe, typically between the end of your billing cycle and the payment due date, during which you can pay your entire balance without incurring any interest charges on new purchases. However, this grace period is usually forfeited if you carry a balance from the previous billing cycle. If you don’t pay your statement balance in full by the due date, you’ll start accruing interest on your purchases immediately, and often on new purchases made during that billing cycle as well. This is why paying your statement balance in full and on time is the most effective way to avoid paying interest on your credit card purchases.

The Financial Implications of Purchase APR

Understanding your purchase APR is not just an academic exercise; it has direct and significant consequences for your financial health. How you manage your credit card balance in relation to your APR can either save you money or cost you a substantial amount over time.

How Interest Accumulates on Your Balance

When you don’t pay your credit card balance in full by the due date, the remaining balance begins to accrue interest at your purchase APR. This interest is added to your principal balance, meaning that in subsequent billing cycles, you’ll be paying interest not only on your original purchases but also on the accumulated interest. This compounding effect can cause your debt to grow rapidly, making it increasingly difficult to pay off.

Let’s illustrate with a simple example:

Suppose you have a balance of $1,000 on your credit card, with a purchase APR of 20% (DPR of approximately 0.0548%).

If you only make the minimum payment and don’t add any new purchases for several months, the interest alone will continue to accrue. If you carry this $1,000 balance for a full year without making any payments, you would incur approximately $200 in interest charges. However, due to compounding, it would be even more if interest is calculated daily and added to the principal. The longer you carry a balance, the more interest you will pay, significantly increasing the overall cost of your purchases.

Strategies to Minimize Interest Costs

The most effective strategy to avoid paying interest on your credit card purchases is to pay your statement balance in full and on time every month. This ensures you take advantage of the grace period and incur no interest charges.

If paying in full isn’t always feasible, here are other strategies to consider:

- Pay more than the minimum payment: While paying only the minimum will keep your account in good standing, it extends the repayment period significantly and racks up substantial interest. Paying even a little more can make a big difference in the long run.

- Target high-interest debt: If you have balances on multiple credit cards, prioritize paying down the card with the highest purchase APR first. This is known as the “debt avalanche” method, and it’s the most mathematically efficient way to save money on interest.

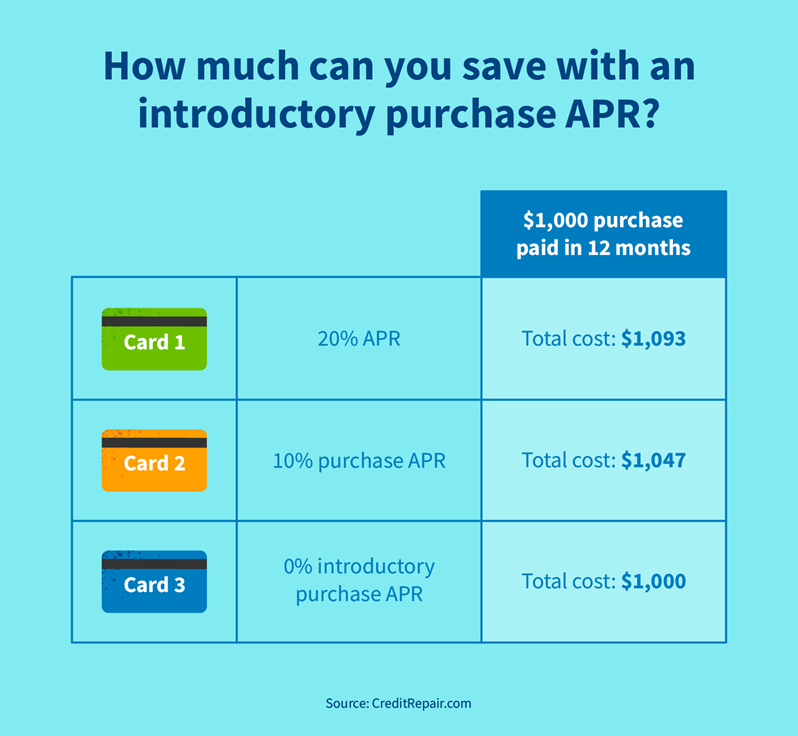

- Consider a balance transfer: If you have a significant balance with a high APR, you might be able to save money by transferring it to a new credit card that offers a 0% introductory APR on balance transfers. Be sure to understand the balance transfer fee and the APR that will apply after the introductory period ends.

- Negotiate with your issuer: In some cases, if you have a good payment history, you may be able to call your credit card issuer and request a lower purchase APR.

How Purchase APR Affects Your Credit Utilization Ratio

While not directly calculating interest, understanding your purchase APR is intrinsically linked to responsible credit card management, which in turn impacts your credit utilization ratio. Your credit utilization ratio is the amount of credit you are using compared to your total available credit. Keeping this ratio low (ideally below 30%) is crucial for maintaining a good credit score.

If you carry a high balance due to your purchase APR, your credit utilization will increase. This can negatively affect your credit score, making it harder to qualify for future loans or credit cards, or potentially leading to even higher APRs on existing or new credit. Therefore, actively managing your spending and paying down balances to keep your utilization low is a key component of maximizing the benefits of your credit card while minimizing its costs, which are directly influenced by your purchase APR.

Navigating Credit Card Offers and APRs

When comparing different credit cards, the purchase APR is one of the most critical factors to consider, alongside fees, rewards, and benefits. A lower APR can translate into significant savings, especially if you anticipate carrying a balance occasionally.

Key Factors to Consider When Choosing a Card

Beyond the purchase APR, several other factors should influence your credit card selection:

- Annual Fee: Some cards come with an annual fee, which may be offset by rewards or benefits. Determine if the value you receive justifies the cost.

- Rewards Programs: Many cards offer rewards like cashback, travel miles, or points. Evaluate if these align with your spending habits and if they offer genuine value.

- Introductory Offers: Look for introductory 0% APR periods on purchases or balance transfers, but always understand the terms and the APR that applies after the introductory period expires.

- Other Fees: Be aware of fees for late payments, cash advances, foreign transactions, and over-limit transactions.

The Importance of Reading the Fine Print

Credit card agreements can be lengthy and complex, but it is imperative to read and understand the “fine print.” This is where you’ll find the details about your purchase APR, how it’s calculated, any introductory APR periods, penalty APRs, and the specific terms under which you might lose your grace period. Failing to understand these terms can lead to unexpected costs and financial strain. Pay close attention to the section detailing the APRs and how they are applied.

Making Informed Decisions for Financial Well-being

Your purchase APR is a dynamic figure that can change over time. Credit card issuers may adjust your APR based on market conditions, your payment history, and changes in your creditworthiness. It’s wise to periodically review your credit card statements and offers to ensure you are still getting the best possible rate. By staying informed about your purchase APR and employing smart borrowing habits, you can harness the convenience of credit cards without falling victim to high interest charges, thereby contributing to your overall financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.