The world of real estate transactions, while exciting for buyers and sellers, can often feel complex and laden with jargon. At the heart of this intricate process stands the Mortgage Loan Originator (MLO), a professional who bridges the gap between individuals seeking to finance their property dreams and the financial institutions that provide the necessary capital. Far from being a mere transactional intermediary, an MLO plays a multifaceted role, offering guidance, expertise, and a crucial helping hand to navigate the often-daunting landscape of mortgage lending. Their work directly impacts a buyer’s ability to secure a home, influencing not just the acquisition of property but also a significant financial decision that shapes their future.

The MLO’s Role: A Financial Architect for Homeownership

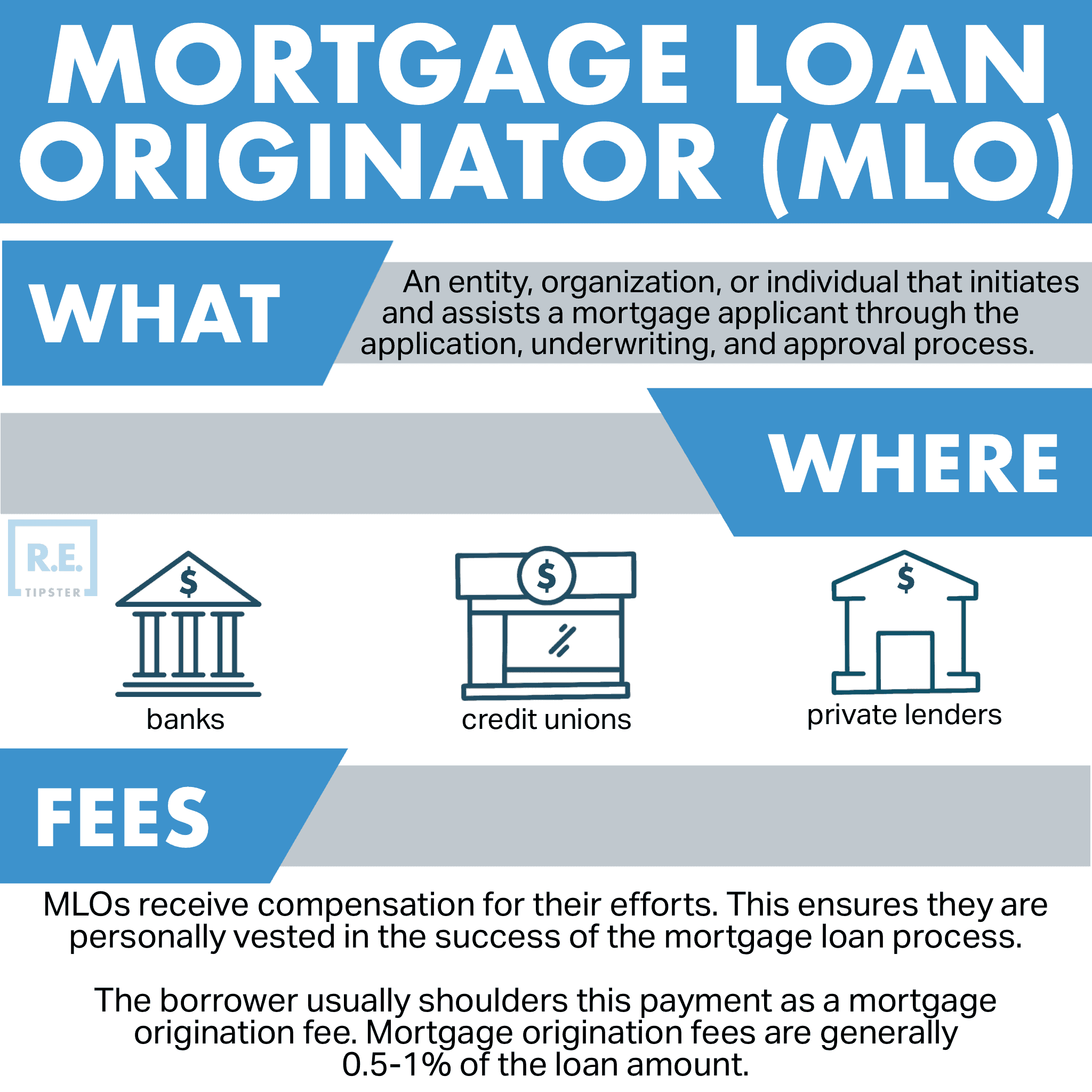

At its core, the primary function of a mortgage loan originator is to facilitate the process of obtaining a mortgage loan. This involves a comprehensive suite of activities designed to assess a borrower’s financial standing, match them with suitable loan products, and shepherd their application through the approval pipeline. They are the frontline representatives of lenders, tasked with understanding a borrower’s unique financial situation and recommending the best possible loan solutions. This requires a deep understanding of various loan programs, interest rates, and lending regulations.

Understanding Borrower Needs and Financial Assessment

The journey begins with an in-depth consultation where the MLO aims to understand the borrower’s specific needs and financial capacity. This involves discussing the purpose of the loan (e.g., purchase, refinance), the desired loan amount, and the borrower’s timeline. Crucially, the MLO will then delve into a thorough assessment of the borrower’s financial health. This typically includes reviewing credit reports to gauge creditworthiness, analyzing income documentation (pay stubs, tax returns), verifying employment history, and examining existing assets and liabilities. The goal is to gain a holistic picture of the borrower’s ability to manage debt and repay a mortgage. This meticulous evaluation is essential for both the borrower, ensuring they don’t overextend themselves, and the lender, mitigating their risk.

Sourcing and Presenting Loan Products

Once the borrower’s profile is established, the MLO’s expertise comes into play as they identify and present suitable loan products. Lenders offer a diverse range of mortgage options, including fixed-rate mortgages, adjustable-rate mortgages (ARMs), FHA loans, VA loans, USDA loans, and jumbo loans, each with its own set of terms, interest rates, and eligibility requirements. The MLO acts as a knowledgeable advisor, explaining the nuances of each option in plain language, highlighting the pros and cons relative to the borrower’s situation, and helping them understand the implications of different interest rate structures and repayment terms. This guidance is invaluable in empowering borrowers to make informed decisions.

Guiding Through the Application Process

The mortgage application process itself can be lengthy and complex, involving numerous forms, documents, and disclosures. The MLO is responsible for guiding the borrower through each step, ensuring that all necessary paperwork is accurately completed and submitted in a timely manner. This includes gathering required documentation such as proof of income, bank statements, and identification. The MLO will explain the purpose of each document and disclosure, ensuring the borrower understands the commitments they are making. They act as a liaison between the borrower and the various departments within the lending institution, such as underwriting and processing, to ensure a smooth and efficient workflow.

The Technical and Regulatory Landscape of Loan Origination

The role of a mortgage loan originator is deeply intertwined with a complex web of technology and stringent regulations. Modern MLOs leverage sophisticated software and digital tools to streamline their operations, enhance accuracy, and ensure compliance. Furthermore, their activities are governed by a robust framework of federal and state laws designed to protect consumers and maintain the integrity of the financial system.

Leveraging Technology for Efficiency and Accuracy

In today’s digital age, technology is an indispensable asset for MLOs. They utilize specialized Loan Origination Software (LOS) systems that automate many aspects of the application process. These systems allow for the electronic collection and storage of borrower data, the generation of loan documents, and the tracking of application progress. Online portals and mobile applications are often used to facilitate secure document sharing between borrowers and originators, enhancing convenience and responsiveness. Furthermore, automated underwriting systems (AUS) employed by lenders often rely on data inputs provided by the MLO to provide preliminary loan eligibility assessments. This technological integration not only speeds up the process but also significantly reduces the likelihood of human error, ensuring greater accuracy in loan applications.

Navigating Regulatory Compliance

The mortgage industry is heavily regulated to protect consumers from predatory lending practices and ensure the stability of the housing market. MLOs must possess a thorough understanding of these regulations, which include laws like the Truth in Lending Act (TILA), the Real Estate Settlement Procedures Act (RESPA), and the Dodd-Frank Wall Street Reform and Consumer Protection Act. These regulations govern disclosure requirements, advertising practices, and fair lending standards. MLOs are required to be licensed and often undergo rigorous background checks and ongoing continuing education to stay abreast of evolving legal requirements. Compliance is not merely a procedural step but a fundamental ethical obligation that MLOs must uphold to ensure fair and transparent lending practices.

Building Trust and Ensuring Borrower Success

Beyond the technical and regulatory aspects, a significant part of an MLO’s role involves building trust and fostering a positive experience for borrowers. This human element is crucial, as securing a mortgage is a major life event often accompanied by stress and uncertainty. A skilled MLO goes above and beyond to alleviate these concerns and empower borrowers to achieve their homeownership goals.

Effective Communication and Education

Clear and consistent communication is paramount. MLOs are responsible for explaining complex financial concepts and loan terms in a way that is easily understood by borrowers, regardless of their financial literacy. This involves proactive updates on application status, timely responses to inquiries, and a willingness to educate borrowers about the entire mortgage process. By demystifying the jargon and providing transparent information, MLOs empower borrowers to feel confident and in control. This educational approach not only facilitates the current transaction but also equips borrowers with valuable knowledge for future financial decisions.

Problem-Solving and Overcoming Obstacles

Not all mortgage applications proceed without a hitch. Borrowers may encounter unexpected challenges, such as credit score issues, income verification discrepancies, or appraisal concerns. An experienced MLO acts as a problem-solver, working diligently to find solutions. This might involve advising a borrower on steps to improve their credit, exploring alternative loan programs, or collaborating with other parties involved in the transaction to resolve issues. Their ability to anticipate potential roadblocks and proactively address them can be the difference between a loan approval and a denial, ultimately contributing to the borrower’s success in achieving homeownership.

Fostering Long-Term Relationships

While the primary goal is to close a specific loan transaction, many MLOs strive to build lasting relationships with their clients. By providing exceptional service, demonstrating expertise, and acting with integrity, they earn the trust and loyalty of borrowers. This can lead to repeat business through refinancing or future home purchases, as well as valuable referrals from satisfied clients. A strong reputation built on trust and successful outcomes is a key indicator of a successful MLO’s career, extending their impact beyond a single transaction to become a trusted financial advisor in their community.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.