Budgeting is often perceived as a restrictive practice—a financial straitjacket designed to limit enjoyment and enforce austerity. In reality, a well-constructed budget is the ultimate tool for liberation. It is a strategic roadmap that ensures your capital is deployed in alignment with your values and long-term objectives. Whether you are aiming to eliminate debt, build a robust investment portfolio, or simply gain clarity over your monthly cash flow, mastering the art of the budget is the first step toward true financial independence.

The Foundation of Financial Literacy: Why Budgeting is Non-Negotiable

Before diving into spreadsheets and calculations, it is essential to understand the philosophical shift required for successful budgeting. At its core, budgeting is the process of proactive resource allocation. Without a plan, money tends to disappear into the “friction” of daily life—subscriptions you no longer use, impulse purchases, and unoptimized service fees.

Shifting from Scarcity to Stewardship

Many people fail at budgeting because they approach it from a mindset of scarcity. They focus on what they cannot buy. Professional financial management flips this perspective to one of stewardship. By creating a budget, you are taking command of your earnings and deciding, in advance, how they will work for you. This transition from being a passive observer of your bank account to an active manager of your wealth is the psychological foundation of all successful investors and entrepreneurs.

Defining Your Financial North Star

A budget without a goal is merely a list of expenses. To make your budget sustainable, you must identify your “North Star.” This could be a down payment on a home, the seed capital for a side hustle, or a retirement fund that allows you to exit the workforce early. When every dollar saved is tied to a specific, motivating vision, the “sacrifice” of skipping an unnecessary expense transforms into an “investment” in your future self.

The Structural Mechanics: How to Build Your Budget From Scratch

The technical process of creating a budget involves a deep dive into your historical data and a projection of your future needs. This requires honesty, precision, and a willingness to confront your spending habits.

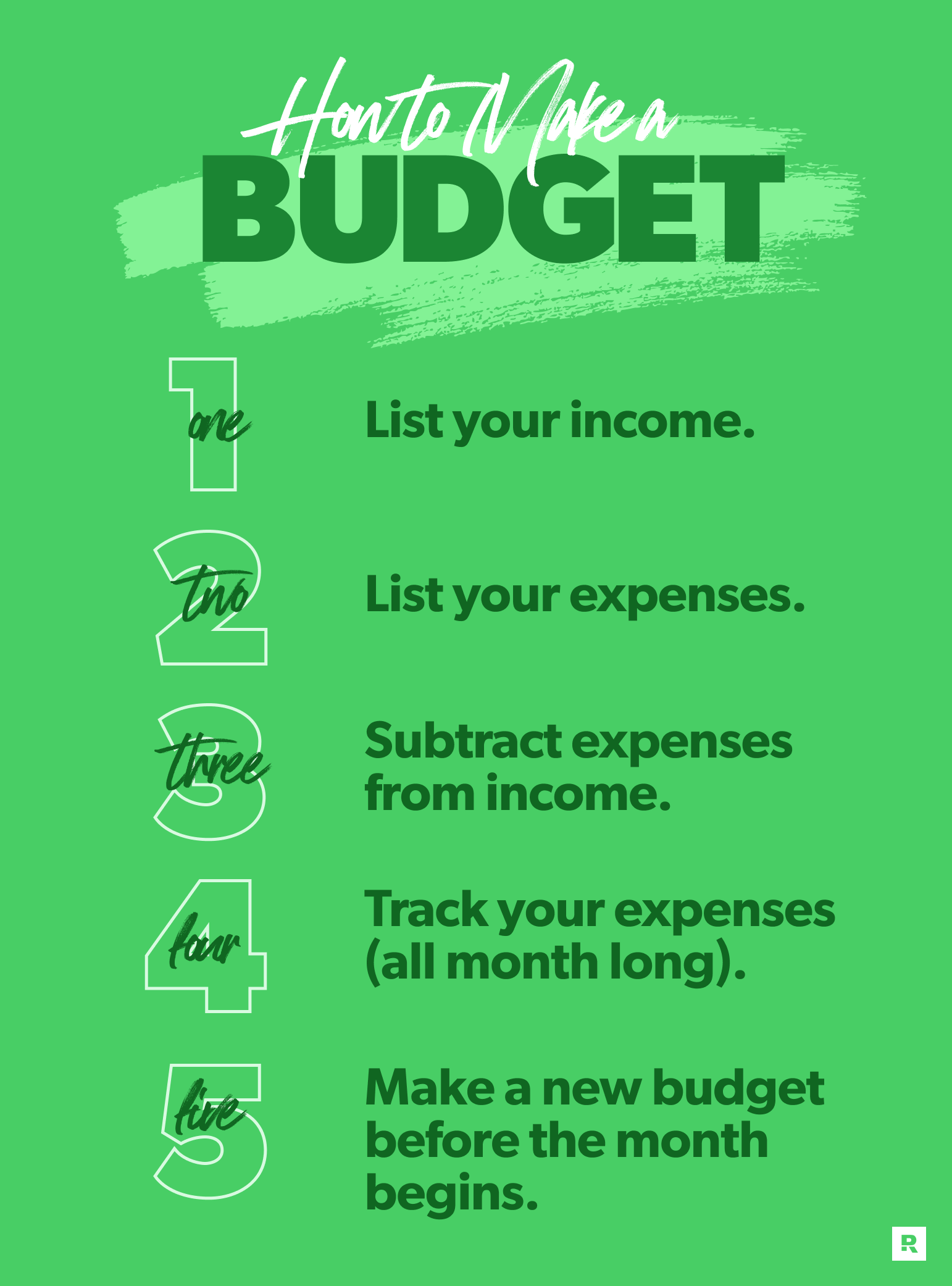

Step 1: Calculate Your True Net Income

The biggest mistake beginners make is budgeting based on their gross salary. Your budget must be built on your “take-home pay”—the amount that actually hits your bank account after taxes, insurance premiums, and retirement contributions. If you are a freelancer or business owner with a fluctuating income, use a conservative average of your last six months of earnings to ensure you don’t over-extend yourself during leaner periods.

Step 2: Categorizing Expenses: Fixed vs. Variable

To gain clarity, you must split your spending into two distinct buckets:

- Fixed Expenses: These are the non-negotiables that remain relatively constant month-to-month. This includes rent or mortgage payments, utilities, insurance, car payments, and minimum debt obligations.

- Variable Expenses: These are costs that fluctuate based on your behavior. This includes groceries, dining out, entertainment, fuel, and personal shopping.

By separating these, you can identify which areas are “locked-in” and which offer “levers” you can pull to increase your savings rate.

Step 3: Accounting for “Sinking Funds”

One of the primary reasons budgets fail is the “surprise” expense—the annual car registration, the holiday gift-giving season, or the semi-annual insurance premium. A sophisticated budget accounts for these through “sinking funds.” You calculate the annual cost of these items, divide by 12, and set that amount aside every month. This ensures that when the “surprise” bill arrives, the money is already waiting.

Choosing the Right Framework: Budgeting Methodologies

There is no one-size-fits-all approach to financial management. The best budget is the one you can actually stick to. Depending on your personality and financial complexity, one of the following frameworks will likely resonate.

The 50/30/20 Rule: The Balanced Approach

Popularized for its simplicity, this method divides your after-tax income into three categories:

- 50% for Needs: Housing, groceries, utilities, and transport.

- 30% for Wants: Hobbies, dining out, and non-essential travel.

- 20% for Financial Goals: Debt repayment, emergency fund building, and investing.

This is an excellent starting point for those who want a high-level overview without tracking every single cent.

Zero-Based Budgeting: The Professional Standard

In zero-based budgeting, every single dollar of your income is assigned a specific job. If you earn $5,000, your expenses, savings, and investments must equal exactly $5,000. This doesn’t mean you have zero dollars in your bank account; it means your “Income minus Outgo” equals zero. This method is highly effective for those who find themselves wondering where their money went at the end of the month, as it demands total accountability for every transaction.

The “Pay Yourself First” Model

This is an “inverse” budgeting style. Instead of calculating what is left over for savings after spending, you decide on a savings/investment goal first (e.g., $1,000 a month). You automate that transfer to occur the moment your paycheck hits. You are then free to spend the remainder of your income however you wish. This is ideal for disciplined earners who want to ensure their wealth grows without the granular tracking of daily expenses.

Optimization: Managing Debt and Building Wealth

Once the basic structure is in place, the budget serves as a tool for optimization. It is here that you move from merely “managing” your money to “multiplying” it.

Strategic Debt Elimination

Your budget should clearly outline your path to becoming debt-free. There are two primary schools of thought here:

- The Debt Snowball: Paying off the smallest balances first to gain psychological momentum.

- The Debt Avalanche: Paying off the highest interest rate debts first to minimize the total cost of borrowing.

By visualizing your available cash flow in your budget, you can see exactly how much “extra” you can throw at these balances to shorten your timeline to freedom.

Integrating Investment and Compound Interest

A budget is the engine that feeds your investment accounts. Professional budgeting views “Investment” as a mandatory expense, not an optional extra. Whether it is a 401(k), an IRA, or a brokerage account, your budget should prioritize these contributions. Seeing the “Investment” line item grow month-over-month provides a sense of progress that no luxury purchase can match.

The Role of the Emergency Fund

A budget is fragile if it isn’t protected by a cash cushion. Financial experts generally recommend keeping three to six months of essential expenses in a high-yield savings account. This fund acts as your “financial insurance,” ensuring that a job loss or medical emergency doesn’t force you to take on high-interest debt and derail your long-term plan.

Maintaining Momentum: The Habit of Financial Discipline

The most detailed budget in the world is useless if it sits in a drawer or an unopened file. Financial mastery is a result of consistent, incremental actions.

The Monthly Audit and Quarterly Refinement

Set a recurring “money date” once a month to review your performance. Did you overspend on dining? Did you forget to cancel a subscription? Use this time not for self-criticism, but for adjustment. Life is dynamic; your budget should be too. If your income increases or your rent changes, update your framework immediately.

Leveraging Automation and Financial Tools

In the modern era, you don’t need to do everything manually. Utilize banking tools that allow for automatic transfers to savings and investment accounts. Use apps that aggregate your spending and categorize it via AI. Automation reduces the “decision fatigue” associated with money management, making it easier to stay on track even when your willpower is low.

The Psychology of Consistency

Understand that you will occasionally “break” your budget. An unexpected social event or a moment of retail therapy might put you over your limit. The key to long-term success is not perfection, but resilience. If you overspend one week, don’t abandon the budget; simply adjust the next week’s spending to compensate.

By following this comprehensive approach to budgeting, you are doing more than just tracking numbers—you are designing your life. A budget gives you the permission to spend guilt-free on the things you love because you have already secured your future. It is the definitive tool for anyone serious about building wealth and achieving lasting financial peace.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.