The passing of a loved one brings a deluge of emotions and an intricate web of responsibilities. Among the many tasks that fall to grieving family members or the appointed executor, understanding and managing the deceased’s financial affairs—particularly outstanding debts like credit card balances—can feel daunting. It’s a common misconception that surviving family members automatically inherit this debt. In reality, the legal and financial landscape is far more nuanced, largely dictated by established financial principles and increasingly influenced by our digital footprint. This article aims to demystify what happens to credit card debt after someone dies, offering clarity, strategic advice, and highlighting how technology and even considerations of personal “brand” intersect with this somber but critical financial process.

The Core Principle: Estate Responsibility, Not Personal Burden

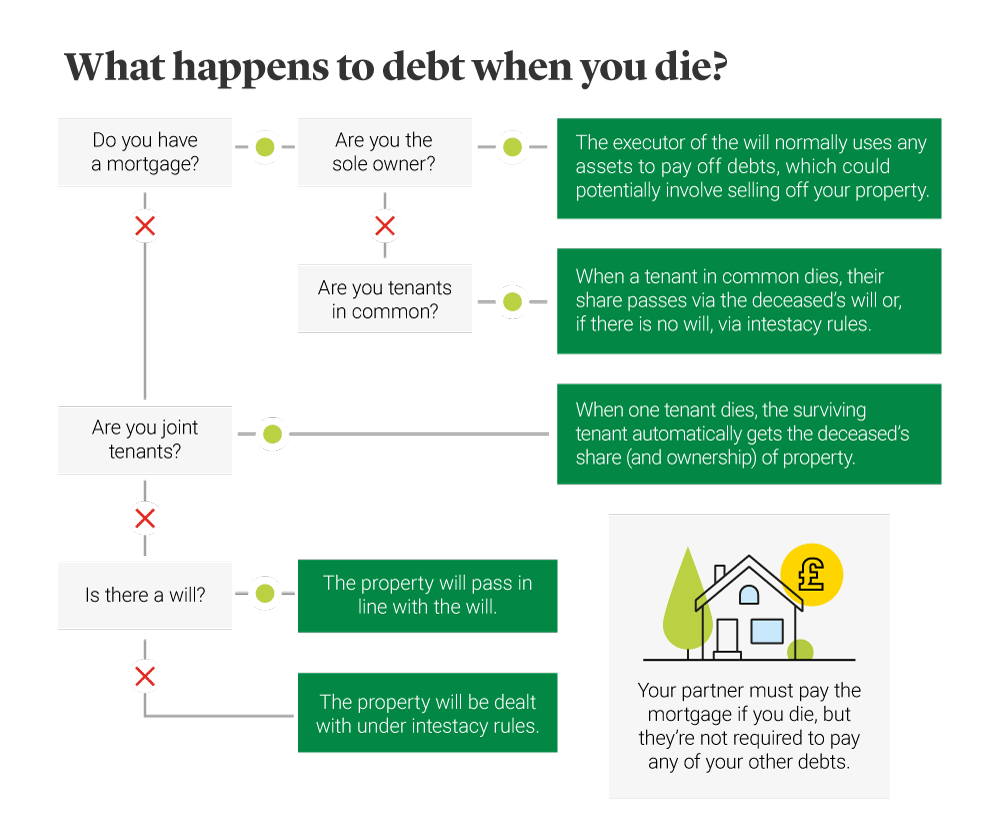

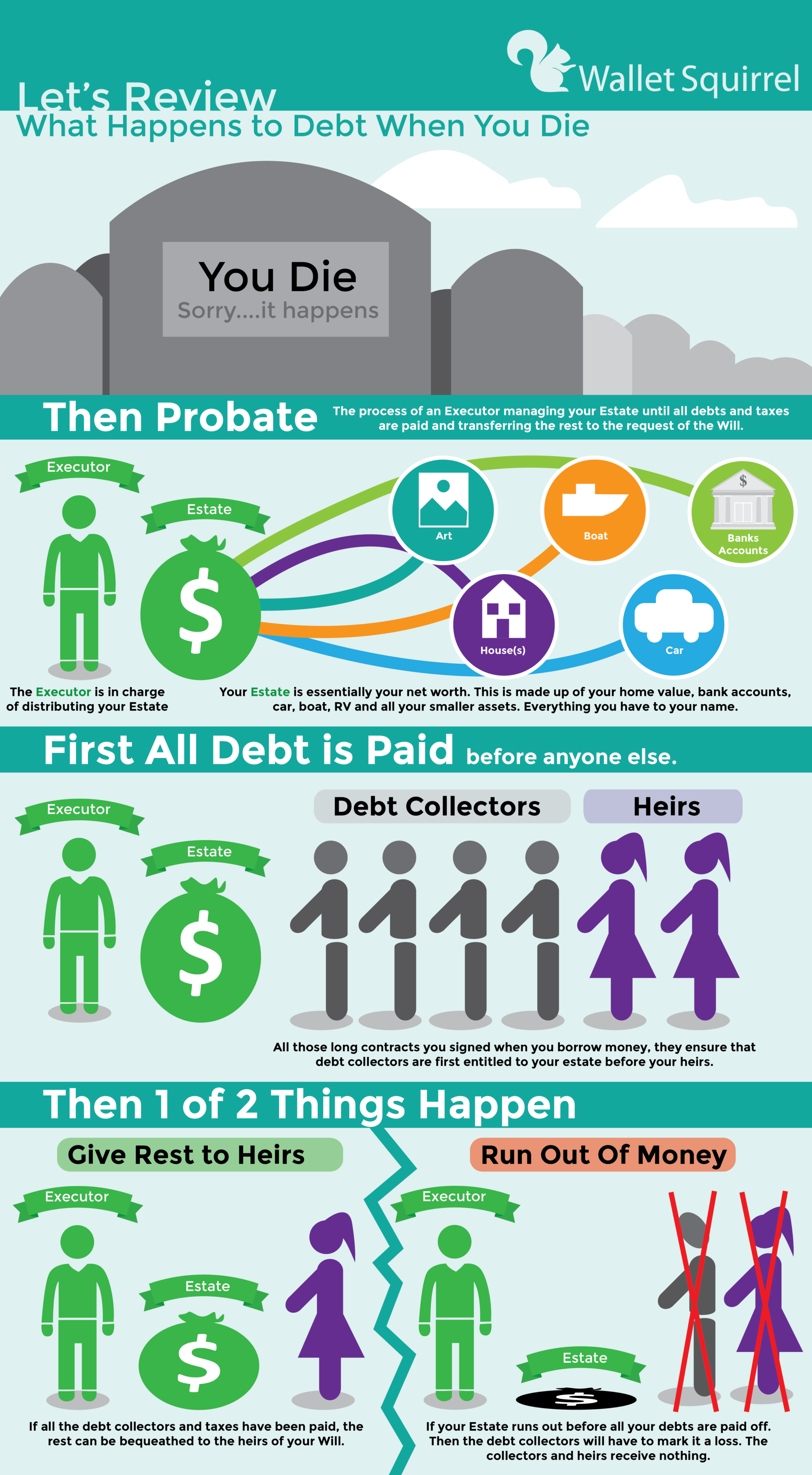

When an individual dies, their personal debts generally do not transfer to their heirs or surviving family members, with a few critical exceptions. Instead, these debts become the responsibility of the deceased person’s “estate.” The estate comprises all assets owned by the individual at the time of their death—everything from bank accounts and investments to real estate, vehicles, and personal possessions. Before any assets can be distributed to beneficiaries, the estate must typically settle all outstanding debts.

Understanding Your Estate and Probate

The process of managing and distributing a deceased person’s estate is known as probate. During probate, an executor (named in a will) or an administrator (appointed by the court if there’s no will) is responsible for identifying and inventorying all assets, determining liabilities (debts), paying taxes, and ultimately distributing the remaining assets according to the will or state law. Credit card debt falls into the category of “unsecured debt,” meaning it’s not tied to a specific asset like a house (mortgage) or car (auto loan).

Creditors, including credit card companies, must typically be notified of the death and have a specific period (which varies by state) to file a claim against the estate. If the estate has sufficient assets, these claims are paid. If the estate is insolvent—meaning its debts exceed its assets—the unsecured creditors, like credit card companies, may only receive a partial payment or nothing at all, after secured creditors and certain priority debts (like funeral expenses or taxes) have been satisfied. Crucially, the executor or administrator uses the estate’s assets to pay these debts, not their own money or the money of the heirs.

When Does Debt Become a Family Burden? Identifying Exceptions

While the general rule protects family members from inheriting credit card debt, there are specific situations where a surviving individual might become responsible. Understanding these exceptions is paramount to avoiding unexpected financial liability.

- Joint Accounts: If you were a joint account holder with the deceased, you are equally responsible for the debt, regardless of who made the purchases. This is because a joint account signifies shared ownership and shared liability. The death of one account holder does not extinguish the other’s obligation.

- Co-signers: Similar to joint accounts, if you co-signed a credit card application with the deceased, you guaranteed repayment. This means you are legally obligated to pay the debt if the primary cardholder (now deceased) cannot.

- Community Property States: In certain states (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin), laws regarding community property can impact spousal debt. In these states, assets acquired during marriage are generally considered community property, and so are debts incurred during the marriage. This means a surviving spouse might be held responsible for community debts, even if they weren’t a joint account holder or co-signer. It’s essential to understand the specific laws of your state.

- Authorized Users: An authorized user on a credit card account is not legally responsible for the debt. They can use the card, but the primary account holder is solely responsible for repayment. Upon the primary cardholder’s death, the authorized user’s access is typically revoked, and they are not liable for any outstanding balance.

- State-Specific Laws and Fraud: There are very rare instances where state laws might impose responsibility, or if there’s evidence of fraudulent activity by surviving family members. For example, if assets were improperly transferred out of the estate to avoid paying creditors, family members could be held liable.

It’s important to emphasize that simply being married to someone or being a beneficiary of their will does not automatically make you responsible for their individual credit card debt. The key distinction lies in whether you had a direct legal connection to the debt itself.

Navigating the Digital Afterlife of Debt: Tech Tools and Considerations

In today’s interconnected world, financial lives are increasingly digital. This shift, while offering convenience in life, adds new layers of complexity when managing an estate, particularly when it comes to identifying and settling debts. The deceased’s digital footprint—online banking portals, email accounts, financial apps, and digital documents—can be both a challenge and a crucial resource for the executor.

The Digital Footprint: Online Accounts and Access

One of the biggest hurdles for an executor is often simply knowing what financial accounts exist. Most people manage multiple credit cards, investment accounts, and other financial services online, often without physical statements. The absence of a clear, organized list of digital assets and liabilities can significantly complicate the probate process.

- Identifying Accounts: Without physical mail, identifying all credit card accounts can be a detective job. Executors may need to scour old emails, check physical mail for stray statements (even if opting for paperless), or look for recurring payments on bank statements. Accessing the deceased’s computer or smartphone, if permission and legal access are granted, might reveal bookmarks, saved passwords (if not secured), or financial apps.

- Accessing Online Portals: Gaining legal access to online banking and credit card portals is essential for checking balances, transaction histories, and initiating communication with creditors. However, strict security protocols, including two-factor authentication and strong passwords, can be significant barriers. While these measures protect us during life, they can inadvertently hinder estate administration after death.

- Digital Estate Planning: This new field recognizes the growing importance of digital assets (social media, cryptocurrencies, cloud storage) and liabilities. Just as individuals prepare a will for physical assets, a “digital will” or a clear plan for digital access can tremendously ease the burden on executors. This includes creating a secure, organized list of online accounts, usernames, and designated contacts for platforms.

Leveraging Financial Tech for Estate Management

While the digital landscape presents challenges, technology also offers powerful tools that can streamline the estate management process, especially for executors.

- Password Managers: These applications are indispensable for managing the myriad of online credentials. A well-organized password manager, where the master password can be securely transmitted to a trusted executor (perhaps through a will or a separate secure document), can provide immediate access to essential financial accounts, including credit card portals. This is far more secure than writing down passwords or sharing them openly.

- Digital Vaults and Secure Cloud Storage: Services designed for secure document storage can house digital copies of important financial documents, wills, insurance policies, and even a list of accounts. Using encrypted cloud storage ensures that vital information is accessible to the authorized executor from anywhere, reducing the need to physically sort through mountains of paper.

- Financial Planning Software and Apps: While the deceased’s financial planning apps might be locked, similar tools can be utilized by the executor. Software designed for personal finance management (e.g., Quicken, Mint) can help an executor track the estate’s finances, categorize transactions, monitor outstanding debts, and generate reports for probate court. Some advanced platforms even offer features for estate planning or integrating with legal services.

- AI Tools (Emerging Role): While still nascent in this specific domain, AI tools are beginning to assist with document analysis and information retrieval. In the future, specialized AI might help executors quickly scan digital records (with appropriate legal access) to identify financial accounts, recurring payments, and potential liabilities, significantly reducing the manual effort involved in piecing together a financial picture. This could evolve into AI-powered virtual assistants for probate navigation, offering guided steps and document preparation support.

- Online Communication Platforms: Email, secure messaging within financial portals, and even video conferencing can facilitate communication between the executor, creditors, lawyers, and financial advisors, speeding up resolution and reducing the need for physical meetings.

The integration of technology into estate management is no longer optional; it’s a necessity. Embracing these tools, both in planning ahead and in the execution phase, can significantly reduce stress and improve efficiency when dealing with post-death financial complexities.

Protecting Your Legacy: Proactive Strategies and Brand Reputation

Beyond the immediate financial and legal implications, how an estate is managed, particularly concerning debts, can subtly affect a family’s reputation and financial stability for generations. Proactive planning isn’t just about minimizing taxes or ensuring smooth asset distribution; it’s about safeguarding peace of mind and preserving the financial “brand” of your family.

The Power of Proactive Estate Planning

Comprehensive estate planning is the cornerstone of responsible financial stewardship. It’s an act of foresight and care that minimizes stress for your loved ones during an already difficult time.

- A Clear Will: A well-drafted will designates an executor and specifies how assets should be distributed. Without a will, state laws dictate asset distribution, which may not align with your wishes, and a court will appoint an administrator, often prolonging the probate process.

- Life Insurance: Life insurance policies are a powerful tool to ensure that your debts, including credit card balances, can be covered without depleting other estate assets. The proceeds typically pass directly to beneficiaries and are often not subject to probate, providing immediate liquidity for survivors to manage expenses or outstanding debts, thereby protecting the core assets intended for heirs. This directly safeguards the financial standing and “brand” of the surviving family members by preventing them from having to liquidate sentimental assets or struggle financially.

- Trusts: Living trusts can allow assets to bypass probate entirely, meaning they can be distributed more quickly and privately, and creditors may have a harder time making claims against them. This can be particularly useful for complex estates or those wanting to ensure certain assets reach beneficiaries efficiently.

- Organized Financial Records: This cannot be stressed enough. Maintaining an updated, accessible list of all financial accounts (bank, investment, credit cards), insurance policies, and digital access information (perhaps in a secure, encrypted digital vault as discussed earlier) is invaluable. Include account numbers, contact information, and details on where to find legal documents. This simple act drastically reduces the executor’s detective work.

- Reviewing Joint Accounts and Co-signed Debts: Periodically review your financial arrangements. If you have joint accounts or have co-signed loans with others, understand the implications for all parties involved should one person pass away.

By taking these proactive steps, individuals not only ensure their wishes are met but also provide a clear, manageable roadmap for their executors. This thoughtful approach shields family members from unnecessary financial burdens and helps preserve their financial “brand” and peace of mind.

Dealing with Creditors: A Strategic Approach

For an executor, managing communication with creditors can be one of the most stressful parts of estate administration. Creditors, including credit card companies, have a right to seek repayment, but executors also have rights and responsibilities to protect the estate.

- Communicate Clearly and Promptly: Once an executor is appointed, they should notify credit card companies of the death, providing a death certificate. This stops interest accumulation in some cases and prevents late fees.

- Understand Legal Obligations: Executors should know that they are not personally responsible for the deceased’s unsecured debts. They should only use estate assets to pay creditors. It’s crucial not to let aggressive collection tactics pressure them into using personal funds.

- Be Wary of Collection Tactics: Unfortunately, some debt collectors may attempt to pressure grieving family members into paying debts they are not legally obligated to pay. They might imply responsibility or use emotionally manipulative language. Executors and family members should know their rights under consumer protection laws. Do not agree to pay debts that are not your legal responsibility. Request all communications in writing.

- Prioritize Debts: The executor must follow a specific order for paying debts as mandated by state law. Typically, funeral expenses, probate costs, and taxes are paid first, followed by secured debts, and then unsecured debts like credit cards. If there aren’t enough assets to pay everyone, unsecured creditors may receive only a pro-rata share or nothing.

- Seek Legal Counsel: When in doubt, especially if the estate is complex, insolvent, or if creditors are particularly aggressive, consulting an estate attorney is always the wisest course of action. They can advise on state-specific laws, creditor negotiation, and ensure the executor fulfills their duties without personal liability.

Effectively navigating these interactions not only protects the estate’s finances but also safeguards the family’s reputation from the potential fallout of aggressive collection practices or financial mismanagement. It’s about maintaining dignity and financial integrity during a challenging period.

Legal Guidance and Moving Forward

The complexities surrounding credit card debt after death underscore the importance of both proactive planning and informed decision-making during probate. It’s a field where general knowledge is good, but specific legal and financial advice is often essential.

When to Seek Professional Expertise

While this article provides a comprehensive overview, every estate is unique.

- Estate Attorney: If the estate is substantial, complex, potentially insolvent, or if there are disputes among heirs or aggressive creditors, an estate attorney is indispensable. They can guide the executor through probate, interpret wills, handle creditor negotiations, and ensure all legal obligations are met.

- Financial Advisor: For long-term financial planning, wealth management, and structuring assets to minimize future probate issues, a financial advisor can provide invaluable insights, helping individuals plan their estates effectively and protect their beneficiaries.

- Tax Professional: Estate taxes can be complex, and a tax professional can help ensure all tax obligations are met accurately, avoiding penalties.

Rebuilding and Learning: Lessons for Financial Health

The experience of dealing with a deceased loved one’s finances offers profound lessons for the living. It highlights the critical importance of:

- Financial Literacy: Understanding how debt works, the role of an estate, and the probate process empowers individuals to plan better for their own futures and assist others.

- Proactive Planning: The greatest gift you can leave your loved ones is not just your assets, but a clear, organized roadmap for managing your affairs after you’re gone. This includes a will, life insurance, and accessible financial records.

- Open Communication: Discussing financial matters with trusted family members or your executor can prevent misunderstandings and emotional distress during an already difficult time.

Ultimately, while the question of “what happens to credit card debt when someone dies” might initially seem grim, it’s an opportunity to emphasize the power of preparation, the protection offered by legal frameworks, and the increasing role of technology in ensuring a smooth and respectful transition of financial legacies. By understanding these dynamics, we can approach life’s inevitable end with greater clarity and peace of mind for ourselves and those we leave behind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.