In the landscape of modern finance, few entities command as much attention, capital, and speculation as Apple Inc. To ask “how much is Apple worth” is to trigger a multi-layered analysis that transcends a simple stock price. While the ticker symbol AAPL provides a real-time number, the true worth of the company is a complex calculation involving massive cash reserves, evolving revenue models, and its unique position within the global economy. As of the mid-2020s, Apple has consistently fluctuated around the $3 trillion market capitalization mark, making it not just a technology company, but a cornerstone of the global financial system.

To understand Apple’s valuation, one must look beyond the hardware and into the mechanics of its balance sheet, its aggressive capital return programs, and its transition from a hardware-reliant manufacturer to a high-margin services behemoth.

The Foundations of Market Capitalization

Market capitalization is the most common metric used to answer the question of a company’s worth. It is the total dollar market value of a company’s outstanding shares of stock. For Apple, this figure is more than just a number; it is a testament to investor confidence and the sheer scale of the organization.

Understanding Share Price and Outstanding Shares

Apple’s market cap is calculated by multiplying its current share price by the total number of outstanding shares. However, what makes Apple’s “worth” in this regard unique is how the company manages those shares. Over the last decade, Apple has been one of the most aggressive practitioners of share buybacks in history. By reducing the number of shares available, Apple increases the “worth” of each remaining share, effectively boosting earnings per share (EPS) even during periods of stagnant revenue growth. This financial engineering is a critical component of why investors value the company so highly despite the law of large numbers making explosive growth difficult.

The Historical Context of Growth

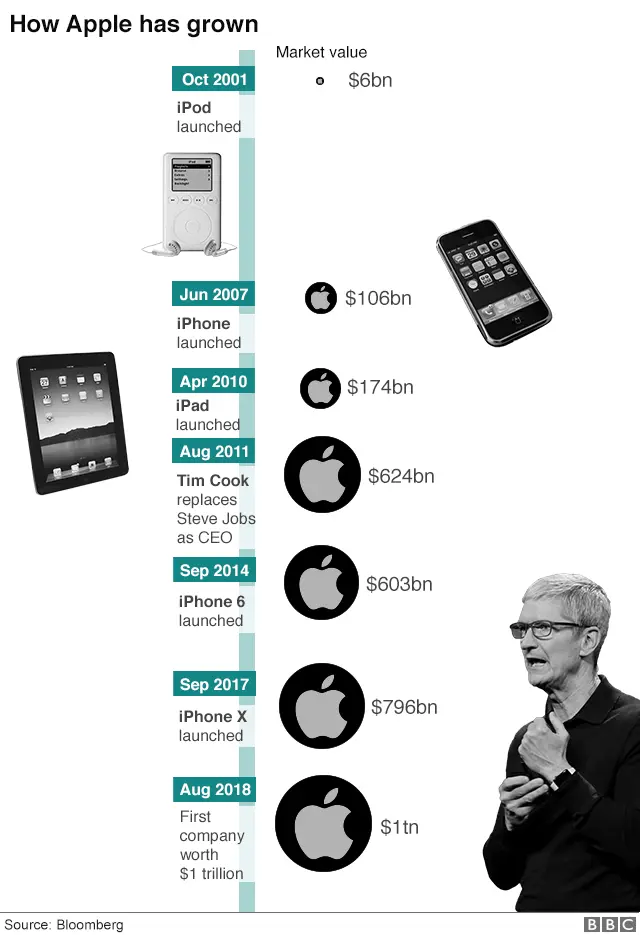

The trajectory of Apple’s valuation is unprecedented. It took the company 42 years to reach a $1 trillion valuation in 2018. It took only two more years to hit $2 trillion in 2020, and roughly 16 months after that to briefly touch the $3 trillion mark. This exponential growth in valuation reflects a shift in how the market views Apple. It is no longer valued as a cyclical hardware company that lives and dies by the next iPhone release; it is now valued as a consumer staples and services giant with incredibly “sticky” recurring revenue.

Diversified Revenue Streams: Beyond the iPhone

A primary driver of Apple’s multi-trillion-dollar valuation is the diversification of its income. While the iPhone remains the sun around which the Apple ecosystem orbits, the company has successfully built a massive secondary economy that justifies a “premium” valuation compared to other hardware makers.

The Services Pivot as a Valuation Multiplier

The “Services” segment—which includes the App Store, iCloud, Apple Music, Apple Pay, and Apple TV+—is perhaps the most important factor in the company’s current worth. From a financial perspective, Services are highly attractive because they offer high gross margins (often exceeding 70%) and recurring revenue. When a company has a predictable stream of income from a billion-plus user base, the “quality” of its earnings improves. Investors are willing to pay a higher Price-to-Earnings (P/E) ratio for Services than they are for hardware, because hardware sales are subject to supply chain shocks and changing consumer tastes.

Wearables and the “Other Products” Category

Apple’s “Wearables, Home, and Accessories” segment, which includes the Apple Watch and AirPods, has grown into a business the size of a Fortune 100 company on its own. By creating a multi-device ecosystem, Apple increases the “switching costs” for consumers. If a user owns an iPhone, an Apple Watch, and AirPods, the financial and logistical cost of switching to an Android ecosystem becomes prohibitive. This ecosystem lock-in provides a “moat” that protects Apple’s valuation by ensuring long-term customer lifetime value.

Fundamental Analysis and Financial Health

When institutional investors determine what Apple is worth, they look deep into the company’s fundamental financial health. Apple’s balance sheet is often described as a “fortress,” providing the company with a level of flexibility that few other entities on earth possess.

The Power of the Balance Sheet

Apple generates an enormous amount of Free Cash Flow (FCF). FCF is the cash a company produces through its operations, minus the cost of expenditures on assets. Apple’s ability to generate nearly $100 billion in FCF annually allows it to self-fund its research and development, acquire smaller companies without taking on massive debt, and weather economic downturns. This liquidity reduces the risk for investors, adding a “safety premium” to its overall valuation. Even in a high-interest-rate environment, Apple’s massive cash pile generates significant interest income, further bolstering its bottom line.

Share Repurchases and Dividend Strategy

Apple’s capital return program is a cornerstone of its financial identity. Since 2012, Apple has returned over $800 billion to shareholders through buybacks and dividends. For a value-oriented investor, Apple’s worth is tied to this consistent return of capital. The dividend provides a yield that attracts conservative income investors, while the buybacks provide a floor for the stock price. This dual approach makes the stock attractive to a wide variety of investment funds, ensuring high demand for the shares.

Risk Factors and Future Valuation Drivers

No valuation is static, and Apple faces significant challenges that could impact its worth in the coming decade. To accurately assess Apple’s value, one must weigh its massive potential against emerging macroeconomic and regulatory threats.

Macroeconomic Headwinds and Geopolitical Risks

Apple’s valuation is sensitive to global trade dynamics, particularly its relationship with China. China serves as both a critical manufacturing hub and a massive consumer market. Any escalation in trade tensions or regulatory crackdowns on foreign tech in China poses a direct threat to Apple’s revenue. Furthermore, as a global company, Apple’s earnings are subject to currency fluctuations. A strong US dollar can eat into the profits reported from international markets, which account for more than half of Apple’s total revenue.

Innovation Cycles: AI and Spatial Computing

The next frontier for Apple’s valuation lies in Artificial Intelligence (AI) and Spatial Computing (the Vision Pro). Markets are currently pricing in Apple’s ability to integrate “Apple Intelligence” across its device lineup to spark a massive hardware upgrade cycle. If Apple successfully positions the iPhone as the primary portal for consumer AI, its valuation could see another leg up. Conversely, if it falls behind in the AI arms race, the market may de-rate the stock, assigning it a lower P/E ratio more in line with a mature utility company rather than a growth-oriented tech leader.

The Investor’s Verdict: Is Apple Overvalued or Undervalued?

Determining if Apple is “worth” its current price requires looking at valuation multiples. Traditionally, Apple traded at a P/E ratio in the mid-teens. In recent years, that multiple has expanded to the high 20s or even 30s.

Comparing P/E Ratios and Growth Rates

The expansion of Apple’s P/E ratio signifies that investors are no longer just buying a phone maker; they are buying a “platform.” When compared to other members of the “Magnificent Seven” (like Microsoft or Nvidia), Apple often trades at a slightly lower multiple because its revenue growth is more modest. However, its stability and massive cash flow often justify the premium over the broader S&P 500 index. Value investors argue that the brand’s pricing power—the ability to raise prices without losing customers—is an intangible asset that isn’t fully captured by traditional accounting but adds billions to its true worth.

Final Financial Outlook

In conclusion, the worth of Apple is a sum of its parts: a dominant hardware business, a rapidly growing services platform, an unparalleled cash-generating engine, and a global brand that commands extreme loyalty. While the market cap provides a headline figure, the “intrinsic value” of Apple lies in its ability to extract a “rent” from the modern digital life of billions of people. As long as the company continues to dominate the pocket, the wrist, and the home, its financial valuation will likely remain at the pinnacle of the corporate world. Whether it is worth $3 trillion or $4 trillion in the future depends on its ability to navigate the transition to AI and maintain its iron grip on the premium consumer market. For now, Apple remains the gold standard for what a modern, fiscally disciplined corporate empire can achieve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.