The concept of “public charge” is a critical, often misunderstood, aspect of U.S. immigration law with profound implications for individuals seeking to live and work in the United States. Far from a mere bureaucratic formality, it’s a rule designed to assess whether an individual is likely to become primarily dependent on government assistance for subsistence. Understanding what benefits fall under this scrutiny, and equally important, which do not, is paramount for anyone navigating the complex immigration landscape. In an increasingly digital and interconnected world, achieving and demonstrating self-sufficiency requires a strategic blend of savvy financial planning, astute leveraging of technology, and the cultivation of a robust personal “brand” that speaks to one’s economic independence.

This article aims to demystify the public charge rule, detailing the specific benefits that can trigger inadmissibility, while also exploring modern strategies — drawn from the realms of tech, brand, and money — to ensure financial resilience and successful integration for immigrants and their families.

Understanding the Public Charge Rule: Definition and Implications

At its core, the public charge rule is a ground of inadmissibility under U.S. immigration law. This means that if an immigration officer determines an applicant is likely to become a “public charge” in the future, that person may be denied a visa, admission to the U.S., or adjustment of status (e.g., obtaining a green card). The rule is not new, tracing its roots back to the late 19th century, but its interpretation and enforcement have evolved over time, causing significant confusion and anxiety among immigrant communities.

Deconstructing the “Public Charge” Definition

The defining characteristic of a “public charge” is an individual who is primarily dependent on the government for subsistence, either through direct cash assistance for income maintenance or through long-term institutionalization at government expense. It’s crucial to emphasize “primarily dependent.” This isn’t about occasional, temporary use of a benefit or services available to the general public for specific, non-subsistence purposes. Instead, the focus is on whether an individual relies on public funds as their main source of financial support over an extended period.

Immigration officials apply a “totality of the circumstances” test when making a public charge determination. This holistic evaluation considers several factors, including:

- Age: The applicant’s age and its potential impact on their ability to work.

- Health: Any medical conditions that might impair their ability to work or require extensive long-term care.

- Family Status: The number of dependents and their financial needs.

- Assets, Resources, and Financial Status: The applicant’s income, savings, investments, and other financial holdings. This is where personal finance strategies become critical.

- Education and Skills: Their educational background, English language proficiency, and job skills, which speak to their employability and earning potential. This ties into personal branding and skill development.

- Affidavits of Support: For family-based immigrants, a sponsor often files an affidavit of support, legally committing to support the immigrant financially if needed. This is a significant mitigating factor.

The implication is clear: demonstrating a strong capacity for self-sufficiency and financial independence is key to overcoming public charge concerns.

Navigating Specific Benefits: What Counts and What Doesn’t

The anxiety surrounding the public charge rule often stems from a lack of clarity regarding which specific government benefits are considered. It’s vital to differentiate between direct cash assistance and long-term care (which are highly scrutinized) versus a broader array of public services that are generally not counted.

Cash Assistance and Long-Term Institutionalization: The Core Triggers

These are the benefits that primarily lead to a public charge determination if an immigrant is found to be heavily reliant on them:

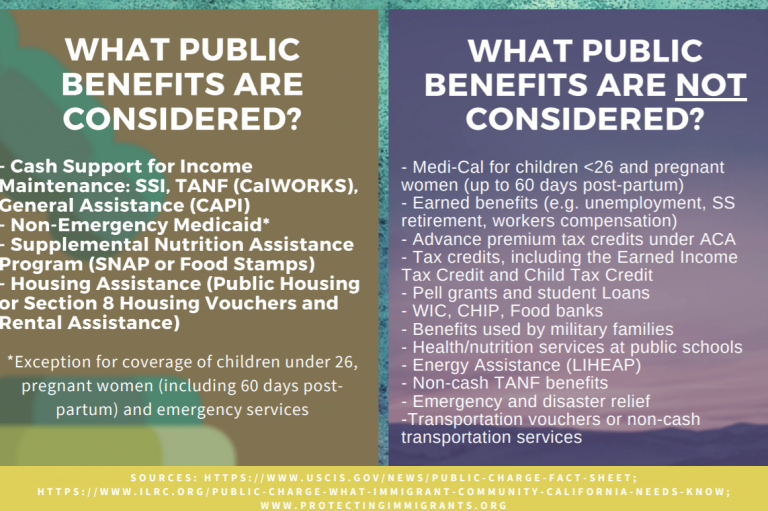

- Supplemental Security Income (SSI): A federal program providing cash assistance to low-income individuals who are aged, blind, or disabled.

- Temporary Assistance for Needy Families (TANF): A federal block grant that provides cash assistance and other benefits to families with children. State and local cash assistance programs that are income-maintenance focused also fall under this category.

- General Assistance (GA): State or local cash benefit programs for low-income individuals who do not qualify for other federal assistance.

- Long-Term Institutional Care at Government Expense: This specifically refers to situations where an individual resides in a nursing home or other long-term care facility, and the primary cost of that care is borne by a government entity (e.g., Medicaid payments for long-term care). Short-term rehabilitation or emergency medical treatment is generally not included.

The common thread among these benefits is their direct provision of cash for daily living expenses or their funding of costly, long-term care that indicates a persistent inability to support oneself.

Essential Services Generally Not Counted: Healthcare, Nutrition, Housing, Education

Fortunately, the vast majority of public benefits and services that promote public health, welfare, and education are not considered for public charge determinations. These are often available to the general public and are designed to improve quality of life and opportunities, rather than provide primary income maintenance. This category includes:

- Medicaid (with exceptions): While long-term institutional care through Medicaid can be counted, most other Medicaid benefits are not. This includes emergency medical care, immunizations, and general healthcare services. Many public health services are exempt because they benefit the entire community.

- Children’s Health Insurance Program (CHIP): Providing low-cost health coverage to children in families who earn too much money to qualify for Medicaid.

- Supplemental Nutrition Assistance Program (SNAP, formerly food stamps): Providing benefits to low-income individuals and families to supplement their grocery budget.

- Special Supplemental Nutrition Program for Women, Infants, and Children (WIC): Providing food, healthcare referrals, and nutrition education for low-income pregnant women, new mothers, and young children.

- Housing Assistance: Public housing, Section 8 housing vouchers, and other forms of housing assistance are generally not counted.

- Educational Benefits: Public K-12 schooling, Head Start, college loans, and other educational assistance are not counted.

- Child Care Services: Subsidies for child care.

- Energy Assistance: Programs to help with heating and cooling costs.

- Emergency Disaster Relief: Aid provided in response to natural disasters.

- Foster Care and Adoption Assistance: Services for children in the child welfare system.

The rationale behind these exemptions is that these programs serve broader public policy goals, such as ensuring a healthy and educated populace, and do not necessarily indicate a primary dependence on government for subsistence. Understanding this distinction is crucial to avoid undue fear and ensure eligible individuals access necessary, non-triggering services.

Building a Foundation of Self-Sufficiency: A Tech, Brand, and Money Blueprint

In an era where economic independence is paramount for immigrants, a proactive and multifaceted strategy is essential. This involves not only understanding financial pitfalls but actively leveraging modern tools and approaches from the worlds of technology, personal finance, and branding.

Smart Money Management: Budgeting, Savings, and Investment Strategies

Financial literacy is the bedrock of self-sufficiency. Immigrants, perhaps more than others, benefit from meticulous financial planning to demonstrate stability and avoid reliance on public benefits.

- Budgeting with Digital Tools: Apps like Mint, YNAB (You Need A Budget), or Simplifi can help individuals track income and expenses, identify areas for savings, and adhere to a financial plan. These tools offer visual dashboards and automated categorization, making complex financial data accessible.

- Building an Emergency Fund: Establishing a robust emergency fund (typically 3-6 months of living expenses) is critical. This safety net prevents individuals from needing to access cash assistance programs during unexpected job loss, illness, or other crises. High-yield savings accounts or automated savings apps like Acorns can facilitate this.

- Strategic Investing: Beyond savings, understanding basic investment principles can help grow wealth. Micro-investing apps and robo-advisors (e.g., Betterment, Wealthfront) make investing accessible, even for those with limited capital. Investing in skills development, through online courses or certifications, can also be viewed as a financial investment that boosts earning potential.

- Debt Management: Proactively managing and reducing debt, especially high-interest consumer debt, frees up cash flow and strengthens overall financial health. Debt snowball or avalanche methods, often trackable through personal finance apps, can be highly effective.

Leveraging Technology for Financial Independence

Technology offers unprecedented opportunities for generating income, enhancing skills, and managing finances, all contributing to a strong case for self-sufficiency.

- Online Income and Side Hustles: The gig economy thrives on technology. Platforms like Upwork, Fiverr, TaskRabbit, Etsy, or even ride-sharing/delivery apps (Uber, DoorDash) provide avenues for individuals to earn income outside traditional employment. This demonstrates initiative and reduces reliance on a single income source.

- E-commerce and Digital Entrepreneurship: Technology has lowered the barrier to entry for starting online businesses. From drop-shipping and selling handmade goods on platforms like Shopify or Etsy, to creating digital products, immigrants can build robust revenue streams.

- Skill Development and Remote Work: Online learning platforms (Coursera, edX, LinkedIn Learning) offer certifications and courses that can upskill individuals, making them more competitive in the job market. This also opens doors to remote work opportunities, providing flexibility and access to a broader range of employment options regardless of location.

- AI Tools for Productivity and Job Search: AI-powered resume builders, cover letter generators, and job matching platforms can significantly enhance an immigrant’s job search efficiency and effectiveness, helping them secure employment faster.

Cultivating Your Personal Brand for Economic Stability

In today’s competitive landscape, a strong personal brand is not just for entrepreneurs; it’s a vital asset for anyone seeking employment and demonstrating competence. For immigrants, it’s a powerful way to signal self-sufficiency.

- Professional Online Presence: Platforms like LinkedIn are indispensable. A well-crafted LinkedIn profile showcasing skills, work history, and recommendations serves as a digital resume and networking tool. It allows potential employers to verify professional capabilities and commitment.

- Storytelling and Portfolio Development: Immigrants often bring unique skills, multilingual abilities, and diverse experiences. A personal brand strategy involves effectively telling this story through a portfolio (for creative professions), a personal website, or even professional blogs. This highlights transferable skills and adaptability.

- Networking and Community Engagement: While digital, networking still revolves around human connection. Participating in online professional groups, virtual conferences, and local community events (if applicable) can open doors to job opportunities and mentorship, reinforcing an image of active engagement and resourcefulness.

- Reputation Management: In the digital age, one’s online footprint matters. Ensuring a professional and positive online presence is part of building a strong personal brand that underscores reliability and economic potential, countering any negative stereotypes associated with public charge concerns.

The Digital Frontier: Data, Security, and AI in Immigration Finance

As immigration processes and personal finance increasingly move online, understanding the intersection of technology, data, and security becomes paramount for immigrants. The responsible use of digital tools can empower individuals, while neglecting security can create vulnerabilities.

Digital Security and Data Privacy for Immigrants

The collection and storage of personal and financial data are inherent in modern immigration applications and financial management. Immigrants must be particularly vigilant.

- Protecting Sensitive Information: Using strong, unique passwords, two-factor authentication, and secure networks is non-negotiable when dealing with immigration forms, bank accounts, or financial apps. Phishing scams and identity theft pose significant risks.

- Understanding Data Sharing: Immigrants should be aware of how their data is collected, stored, and shared by various platforms—from immigration agencies to financial institutions and social media. Using privacy-focused browsers and being mindful of permissions granted to apps can mitigate risks.

- Secure Financial Transactions: When engaging in online income-generating activities or managing investments, using reputable and secure payment gateways (e.g., PayPal, Stripe, secure bank transfers) is essential to protect funds and personal financial details.

AI and Automation for Informed Decision-Making

Artificial intelligence and automation are transforming how individuals access information and make decisions, offering a potentially powerful ally for immigrants navigating complex financial and legal landscapes.

- AI-Powered Legal Research and Guidance: While not a substitute for legal counsel, AI tools can help process vast amounts of immigration regulations and financial guidelines, providing quick summaries or identifying relevant sections. This can help immigrants better understand their rights and responsibilities regarding public charge.

- Automated Financial Advising: Robo-advisors use AI to manage investments based on an individual’s financial goals and risk tolerance, offering a cost-effective alternative to traditional financial advisors. This can help build assets efficiently.

- Predictive Analytics for Financial Planning: Some advanced financial tools can use AI to analyze spending patterns and income fluctuations, offering predictive insights to help individuals budget more effectively and anticipate potential financial shortfalls, thus proactively avoiding situations that might necessitate public benefits.

- Language Translation and Accessibility: For non-English speakers, AI-powered translation tools integrated into financial or legal platforms can significantly improve comprehension and access to critical information, leveling the playing field.

The responsible adoption of these technologies, coupled with a healthy dose of skepticism and verification, can significantly empower immigrants to make informed choices, secure their data, and solidify their path to self-sufficiency.

In conclusion, the “public charge” rule is a nuanced and significant aspect of U.S. immigration policy. While certain cash benefits and long-term institutional care can trigger inadmissibility, a wide array of essential public services are exempt. For those seeking to establish themselves in the U.S., a proactive approach to demonstrating self-sufficiency is paramount. This involves not just understanding the specific rules but actively building a resilient financial future. By strategically employing smart money management techniques, leveraging the vast opportunities presented by modern technology for income generation and skill development, and cultivating a strong personal brand, immigrants can navigate this complex terrain with confidence, ensuring they are well-prepared to contribute to their new communities without relying on the public purse. The journey to immigration success in the 21st century is undeniably intertwined with financial literacy, digital prowess, and a clear vision for personal and economic independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.