In the world of finance, percentages are the universal language of value, growth, and risk. Whether you are analyzing a stock portfolio, managing a corporate budget, or simply trying to optimize your personal savings, the ability to calculate and interpret percentages is perhaps the most critical mathematical skill a professional can possess. Percentages allow us to normalize data, making it possible to compare a small-cap startup’s growth to a blue-chip giant’s performance on an even playing field.

Understanding how to calculate percentages goes far beyond basic arithmetic; it involves understanding the narrative behind the numbers. This guide will walk you through the fundamental formulas and apply them to the sophisticated contexts of personal finance, investment strategy, and business operations.

The Fundamentals of Financial Percentages

Before diving into complex investment strategies, one must master the basic mechanics of percentage calculations. In finance, we primarily deal with three types of percentage problems: finding the percentage of a total, calculating percentage change (growth or decay), and determining the original value after a change has occurred.

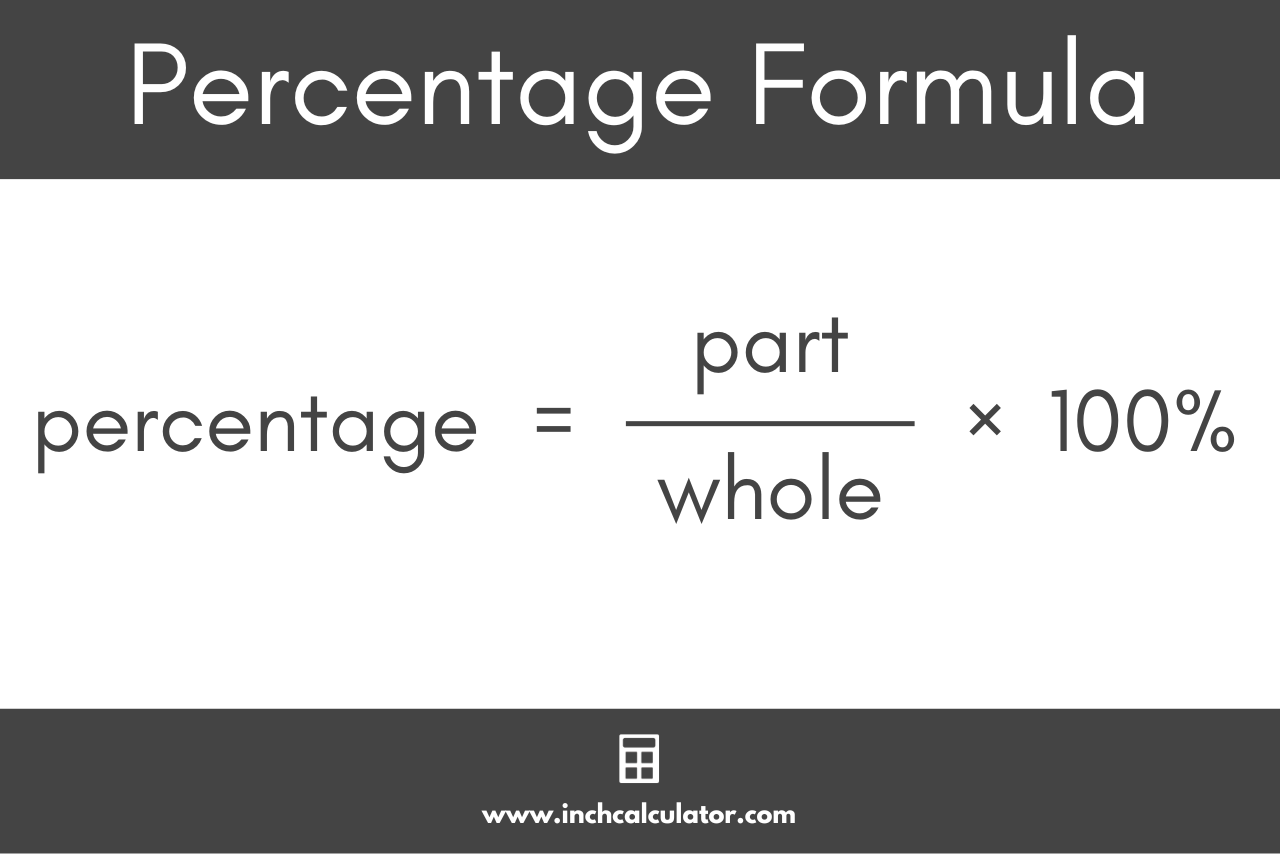

Finding the Base Percentage (The Part over Whole)

The most basic calculation is determining what percentage a specific amount represents within a larger total. In a financial context, this is often used for asset allocation. If you have a total portfolio of $100,000 and $20,000 is invested in gold, what is your gold exposure?

The formula is: (Part / Whole) × 100 = Percentage.

In this scenario: ($20,000 / $100,000) × 100 = 20%. This fundamental calculation helps investors ensure they are not over-leveraged in a single asset class, maintaining a balanced risk profile.

Calculating Percentage Increases (Growth)

In finance, we are constantly looking for growth. To calculate the percentage increase between an initial value and a final value—such as the growth of a retirement account over a year—we use the “New minus Old” formula.

The formula is: [(New Value – Old Value) / Old Value] × 100 = Percentage Increase.

If your account grew from $50,000 to $57,500:

- $57,500 – $50,000 = $7,500 (The absolute gain)

- $7,500 / $50,000 = 0.15

- 0.15 × 100 = 15% increase.

Calculating Percentage Decreases (Losses and Discounts)

Understanding losses is even more critical for capital preservation. The formula remains the same, but the result will be negative, indicating a decrease. A common mistake in finance is failing to realize that a percentage decrease requires a larger percentage increase to “break even.”

For example, if a stock drops by 50%, it does not need a 50% gain to return to its original price; it needs a 100% gain. This mathematical reality is why professional money managers focus heavily on “drawdown” percentages—the peak-to-trough decline during a specific period.

Percentages in Personal Wealth Management

Applying percentage calculations to your daily financial life is the difference between “guessing” and “planning.” From budgeting to managing debt, percentages provide a framework for healthy financial habits.

The 50/30/20 Rule: Percentage-Based Budgeting

One of the most effective ways to manage personal cash flow is through the 50/30/20 rule. This strategy allocates after-tax income into three percentage-based categories:

- 50% for Needs: Housing, utilities, groceries, and insurance.

- 30% for Wants: Dining out, hobbies, and travel.

- 20% for Financial Goals: Debt repayment, emergency funds, and retirement contributions.

By calculating these percentages monthly, you can quickly identify if your “Needs” are eating into your “Goals,” allowing for data-driven adjustments to your lifestyle.

Debt-to-Income (DTI) Ratios

When you apply for a mortgage or a car loan, lenders calculate your Debt-to-Income ratio. This is a percentage that compares your monthly debt payments to your gross monthly income.

The formula is: (Total Monthly Debt Payments / Gross Monthly Income) × 100.

Most lenders prefer a DTI ratio below 36%, with no more than 28% of that debt going toward a mortgage or rent. Understanding this percentage helps you see your creditworthiness through the eyes of a financial institution, allowing you to pay down debts strategically before seeking new credit.

The Rule of 72 and Compound Interest

While not a direct percentage calculation, the Rule of 72 is a mental shortcut used to determine how long it will take for an investment to double at a fixed annual percentage rate of interest. You simply divide 72 by the annual rate of return.

For instance, if your investment yields a 6% annual return, it will take approximately 12 years (72 / 6) for your money to double. This highlight’s the power of the “annual percentage rate” (APR) and why even a 1% difference in interest rates can result in tens of thousands of dollars in lost or gained wealth over a lifetime.

Investment Mathematics: ROI and Portfolio Performance

For the serious investor, percentages are the primary metric for success. They allow for the comparison of disparate assets, such as real estate, stocks, and crypto-assets.

Return on Investment (ROI) vs. Annualized Return

The most common calculation in the investing world is ROI. It measures the efficiency of an investment.

The formula is: [(Current Value – Cost of Investment) / Cost of Investment] × 100.

However, professional investors often prefer “Annualized Return” because ROI does not account for time. If Investment A returns 20% over five years and Investment B returns 15% in one year, Investment B is the superior performer. Calculating the Compound Annual Growth Rate (CAGR) provides a more accurate percentage of yearly growth, allowing for a better comparison between long-term and short-term holdings.

Understanding Dividend Yields

For income-focused investors, the dividend yield is a crucial percentage. It represents how much a company pays out in dividends each year relative to its stock price.

The formula is: (Annual Dividends per Share / Price per Share) × 100.

A high dividend yield might look attractive, but if the percentage is unusually high (e.g., 15%), it may signal that the stock price has plummeted due to underlying business trouble. Calculating this percentage helps investors balance the need for immediate cash flow with the necessity of capital stability.

Inflation Adjustments: Real vs. Nominal Returns

If your savings account pays 4% interest but inflation is running at 5%, you are actually losing purchasing power. To calculate your “Real” return, you subtract the inflation percentage from your nominal (stated) return.

- Nominal Return: 4%

- Inflation: 5%

- Real Return: -1%

Understanding this percentage-based relationship is vital for long-term retirement planning, as it ensures you are calculating your future wealth based on what that money will actually buy, rather than just the number on the screen.

Business Finance and Profitability Metrics

In a corporate or entrepreneurial setting, calculating percentages is essential for measuring the health and sustainability of a business. Revenue is a “vanity metric”; percentages like profit margins are “sanity metrics.”

Gross vs. Net Profit Margins

A business may generate millions in sales, but if its margins are thin, it is at high risk.

- Gross Profit Margin: This calculates the percentage of revenue exceeding the cost of goods sold (COGS). Formula: [(Revenue – COGS) / Revenue] × 100.

- Net Profit Margin: This is the “bottom line”—the percentage of revenue left after all expenses, including taxes and interest, have been paid. Formula: (Net Income / Revenue) × 100.

A software company might have a 90% gross margin but a 10% net margin due to high research and marketing costs. Monitoring these percentages helps business owners decide where to cut costs or when to scale operations.

Effective Tax Rates

Businesses and high-net-worth individuals rarely pay the “statutory” tax rate (the rate listed in the tax code). Instead, they calculate their “Effective Tax Rate,” which is the actual percentage of their income paid in taxes after deductions and credits.

The formula is: (Total Tax Paid / Taxable Income) × 100.

Knowing this percentage is vital for cash flow forecasting, as it allows a business to set aside the correct amount of capital for quarterly tax obligations.

Market Share Analysis

Percentages also define a company’s competitive standing. Market share is calculated by taking the company’s sales over a period and dividing it by the total sales of the industry over the same period.

Formula: (Company Sales / Total Industry Sales) × 100.

This percentage tells investors whether a company is a dominant leader or a niche player, which significantly influences the stock’s valuation and perceived risk.

Tools for Precision in Financial Calculation

While manual calculation is a vital skill for quick decision-making, professional-grade financial management requires tools that minimize human error and handle complex variables.

Leveraging Financial Calculators

Specialized financial calculators (like the HP 12C or TI BA II Plus) are designed specifically to handle percentage-based financial functions, such as Net Present Value (NPV) and Internal Rate of Return (IRR). These tools allow users to input interest rates as percentages to solve for future value, making them indispensable for mortgage brokers and investment bankers.

Spreadsheet Mastery (Excel and Google Sheets)

For most professionals, Excel is the primary tool for percentage calculations. Using formulas like =SUM(A1:A10)/B1 or the built-in percentage formatting allows for the processing of massive datasets. Furthermore, Excel’s “What-If Analysis” allows you to see how changing one percentage—such as a 1% increase in interest rates—will ripple through an entire 30-year financial model.

Conclusion: Empowerment Through Mathematical Literacy

Calculating percentages is more than just a mathematical exercise; it is a fundamental pillar of financial empowerment. When you understand how to calculate growth, analyze margins, and assess risk through the lens of percentages, you move from being a passive observer of your finances to an active architect of your wealth.

Whether you are calculating the ROI of a new venture or ensuring your personal budget adheres to the 50/30/20 rule, these percentages provide the clarity needed to make informed, professional, and ultimately profitable decisions. In the world of money, those who master the percentage master the game.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.