At its core, the Allowance for Doubtful Accounts (ADA) is a contra-asset account on a company’s balance sheet. This might sound like a purely technical accounting term, but its implications reach far beyond the ledger, touching upon a business’s financial health, technological adoption, and even its brand reputation in an increasingly complex and interconnected global economy. In essence, ADA serves as a vital financial safeguard, reflecting management’s best estimate of the portion of accounts receivable that may not be collected. It’s a critical component of accurate financial reporting, allowing businesses to present their net realizable value of receivables, thereby offering a more realistic picture of their assets and liquidity.

However, understanding ADA today requires a perspective that integrates finance with the transformative power of technology and the strategic imperatives of brand building. In an era where digital transactions dominate, AI-driven analytics are commonplace, and customer perception can make or break a business, the management of doubtful accounts has evolved from a mere accounting exercise into a strategic function. This article will delve into the fundamental nature of ADA, explore how technology is revolutionizing its management, and examine its profound impact on a company’s brand and overall business strategy, providing a holistic view relevant to modern enterprises navigating the realms of money, tech, and brand.

Unpacking the “Allowance for Doubtful Accounts”: A Core Financial Concept

To truly grasp the significance of ADA, we must first understand its foundational role in financial accounting. It’s not just an arbitrary number; it’s a meticulously calculated estimate designed to uphold the integrity of financial statements and provide stakeholders with a truthful representation of a company’s assets.

Understanding the Basics: What is ADA?

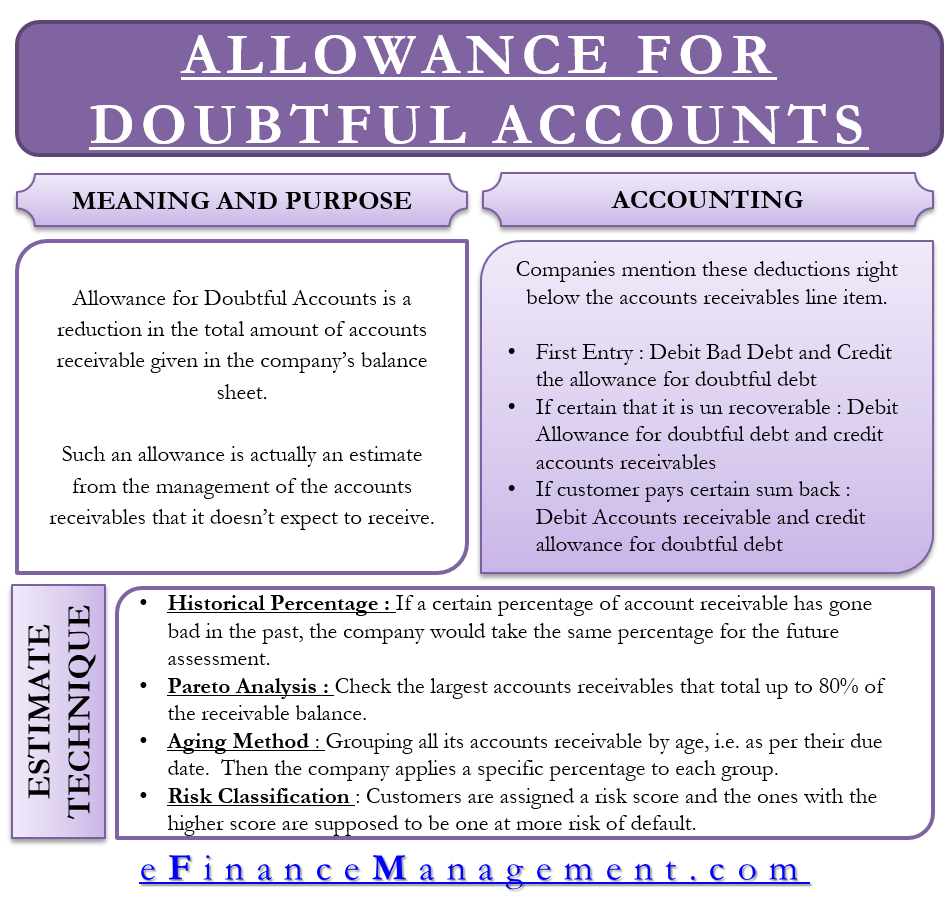

The Allowance for Doubtful Accounts (ADA) is a valuation account associated directly with Accounts Receivable. When a business sells goods or services on credit, it records an Accounts Receivable, an asset representing the money owed to it by customers. However, not all customers will pay their debts. Some might default due to financial difficulties, disputes, or even bankruptcy. Rather than waiting for these defaults to occur, which could distort financial reporting, GAAP (Generally Accepted Accounting Principles) and IFRS (International Financial Reporting Standards) mandate that companies estimate these uncollectible amounts in advance.

This is where ADA comes in. It’s a “contra” account because it reduces the gross amount of Accounts Receivable to arrive at the net realizable value – the amount the company realistically expects to collect. Think of it as a financial buffer, a realistic provision for potential losses from credit sales. Its existence adheres to the matching principle in accounting, which dictates that expenses (like bad debt expense) should be recognized in the same period as the revenues they helped generate. Therefore, the estimated cost of uncollectible sales made on credit is recognized in the period the sale occurred, not necessarily when the actual uncollectible debt is identified and written off.

The Mechanics: How ADA Works in Accounting

The operational mechanics of ADA involve a few key steps and journal entries that illustrate its dynamic nature:

- Estimating Bad Debt Expense: At the end of an accounting period (e.g., month, quarter, year), a company estimates the portion of its current accounts receivable that will likely be uncollectible. This estimate is based on historical data, industry trends, economic conditions, and specific customer analyses. The two most common methods are the “percentage of sales method” (estimating bad debt as a percentage of credit sales) and the “aging of receivables method” (analyzing receivables based on how long they’ve been outstanding, with older receivables generally having a higher probability of default).

- Adjusting Entry: Once the estimate is made, an adjusting journal entry is recorded. This involves:

- Debiting Bad Debt Expense: This account appears on the income statement, reducing net income.

- Crediting Allowance for Doubtful Accounts: This increases the ADA balance on the balance sheet.

This entry reflects the expense of potential uncollectible accounts in the period the revenue was earned.

- Writing Off an Actual Uncollectible Account: When a specific customer’s account is deemed absolutely uncollectible (e.g., they declare bankruptcy), the company writes it off. This involves:

- Debiting Allowance for Doubtful Accounts: This reduces the ADA balance.

- Crediting Accounts Receivable: This removes the specific customer’s balance from the total Accounts Receivable.

Crucially, this write-off does not affect Bad Debt Expense or Net Income at this point, as the expense was already recognized in the period of the initial estimate. It only adjusts the balance sheet accounts.

- Recovery of Previously Written-Off Accounts: Occasionally, a customer whose account was previously written off might later pay their debt. In such cases, two entries are typically made:

- Reinstating the Account: Debiting Accounts Receivable (for the specific customer) and Crediting Allowance for Doubtful Accounts.

- Recording the Cash Collection: Debiting Cash and Crediting Accounts Receivable (for the specific customer).

This sequence ensures accurate record-keeping and reverses the impact of the initial write-off.

Why It Matters: Implications for Financial Health

The diligent management and accurate estimation of ADA are paramount to a company’s financial health and its credibility among stakeholders.

- Accurate Financial Reporting: ADA ensures that Accounts Receivable are presented at their “net realizable value,” giving a truthful picture of the assets a company truly expects to convert into cash. Without ADA, assets would be overstated, leading to an artificially inflated perception of financial strength.

- Informed Decision-Making: Investors, creditors, and internal management rely on accurate financial statements to make crucial decisions. A realistic ADA allows investors to assess a company’s risk exposure and efficiency in collecting debts. Lenders use this information to evaluate creditworthiness. Internally, it helps management identify issues with credit policies, sales practices, or collection efforts.

- Compliance and Governance: Adhering to accounting standards (GAAP/IFRS) through proper ADA estimation is essential for regulatory compliance, avoiding penalties, and maintaining good corporate governance.

- Profitability and Cash Flow: While ADA itself isn’t a cash transaction, it directly impacts the Bad Debt Expense, which reduces reported net income. A high Bad Debt Expense can signal inefficiencies in credit management, impacting profitability. Ultimately, uncollected receivables reduce actual cash flow, making ADA a proxy for a future cash flow challenge.

The Digital Frontier: Tech’s Transformative Role in Managing Doubtful Accounts

The process of estimating and managing ADA, once a largely manual and historical data-dependent task, has been profoundly transformed by technological advancements. In today’s digital landscape, technology is not just an enabler but a fundamental pillar for efficient, accurate, and proactive doubtful accounts management.

Leveraging Accounting Software and ERP Systems

Modern businesses rely heavily on sophisticated accounting software and Enterprise Resource Planning (ERP) systems. These platforms integrate various business functions, including sales, inventory, purchasing, and finance, providing a centralized repository for data. For ADA, these systems offer several critical advantages:

- Automated Record-Keeping: Sales made on credit are automatically recorded as Accounts Receivable, reducing manual errors and increasing efficiency.

- Real-time Data Access: Finance teams can access up-to-the-minute data on outstanding receivables, customer payment histories, and aging reports. This real-time visibility is invaluable for making timely collection decisions and preparing more accurate ADA estimates.

- Integration with CRM: Many ERPs integrate with Customer Relationship Management (CRM) systems, allowing a holistic view of customer interactions, purchase history, and payment behavior, which provides richer data for credit risk assessment.

- Cloud-Based Solutions: Cloud accounting software offers accessibility, scalability, and automatic updates, making advanced financial management tools available even to small and medium-sized businesses without significant upfront IT infrastructure investments. These platforms facilitate collaboration and remote access, crucial for distributed teams.

AI and Predictive Analytics for Credit Risk Assessment

Perhaps the most revolutionary impact of technology on ADA management comes from Artificial Intelligence (AI) and predictive analytics. Instead of merely reacting to past defaults, AI allows businesses to anticipate them with remarkable accuracy.

- Sophisticated Credit Scoring: AI algorithms can analyze vast datasets, including traditional credit scores, payment histories, industry-specific benchmarks, macroeconomic indicators, social media sentiment, and even unstructured data from news articles or customer reviews. This allows for more granular and dynamic credit risk assessment for new and existing customers.

- Early Warning Systems: Machine learning models can identify patterns and anomalies in payment behavior that precede default. This enables companies to implement early intervention strategies, such as offering payment plans, sending proactive reminders, or adjusting credit limits, before accounts become critically overdue.

- Optimized ADA Estimation: By providing more accurate forecasts of uncollectible accounts, AI helps refine the ADA estimation process. This moves beyond simplistic historical percentages to a more data-driven, forward-looking approach, reducing the likelihood of over- or under-provisioning.

- Automated Collection Strategies: AI can segment customers based on their risk profile and likelihood of responding to different collection methods, automating personalized communication sequences (emails, SMS, calls) to improve collection rates while minimizing human intervention and costs.

Data-Driven Insights and Automation

Beyond AI, the broader field of data analytics provides invaluable insights, while automation streamlines the entire receivables management process.

- Dashboard and Reporting: Interactive dashboards provide finance managers with a clear, visual overview of key metrics related to accounts receivable, such as aging categories, average collection period, and bad debt trends. These tools facilitate quicker identification of problem areas and performance tracking.

- Automated Reminders and Communication: Systems can automatically send out payment reminders, overdue notices, and even customized follow-up messages based on predefined rules and customer segments, improving collection efficiency.

- Trend Analysis: Data analytics helps in identifying long-term trends in customer payment behavior, seasonal fluctuations in bad debt, and the effectiveness of different credit policies, informing future strategic decisions.

- Fraud Detection: Advanced analytics can also play a role in identifying potential fraudulent transactions that might lead to uncollectible accounts, adding another layer of security and risk mitigation.

Digital Security and Confidentiality of Financial Data

With the increased reliance on technology to manage sensitive financial data, digital security becomes paramount. When implementing tech solutions for ADA, businesses must prioritize data protection.

- Data Encryption: Ensuring all financial data, especially customer payment information and credit histories, is encrypted both in transit and at rest.

- Access Control: Implementing robust access controls to ensure that only authorized personnel can view or modify sensitive financial records.

- Compliance: Adhering to relevant data privacy regulations like GDPR, CCPA, and industry-specific standards, which dictate how personal and financial data must be handled and protected.

- Cybersecurity Measures: Employing strong firewalls, intrusion detection systems, regular security audits, and employee training to prevent cyberattacks and data breaches. A data breach involving customer financial information can have catastrophic consequences for a company’s brand and legal standing, far outweighing the savings from optimized ADA.

Beyond the Balance Sheet: ADA’s Influence on Brand and Business Strategy

While ADA is fundamentally a financial concept, its accurate management extends its influence significantly to a company’s brand reputation, stakeholder trust, and overarching business strategy. A realistic approach to doubtful accounts isn’t just about financial prudence; it’s about projecting an image of reliability, ethical conduct, and strong governance.

Building Trust: Transparency and Financial Reporting

For investors, creditors, and other stakeholders, financial statements are the primary window into a company’s health and performance. A meticulously calculated and transparent Allowance for Doubtful Accounts signals financial integrity.

- Investor Confidence: Investors look for consistency and realism in financial reporting. An ADA that appears too low might suggest management is overly optimistic or even attempting to inflate assets, leading to skepticism. Conversely, an excessively high ADA might signal underlying issues with sales quality or credit policies. A balanced, well-supported ADA fosters trust, assuring investors that the company’s reported assets are genuinely convertible to cash.

- Lender Relationships: Banks and other lending institutions critically evaluate a company’s accounts receivable and ADA when assessing loan applications. A strong, transparent ADA helps lenders accurately gauge credit risk and a company’s ability to service debt, potentially leading to more favorable lending terms.

- Ethical Governance: Proper ADA management is a cornerstone of ethical corporate governance. It demonstrates a commitment to fair and accurate representation, preventing misleading financial portrayals that could harm stakeholders. Financial scandals often involve misrepresentation of assets, and an inadequate ADA can be a red flag.

Customer Relationships and Credit Policy as a Brand Touchpoint

The process of extending credit and managing collections is a direct touchpoint with customers, significantly impacting their perception of the brand. The underlying philosophy behind ADA informs these interactions.

- Balancing Risk and Customer Experience: A company’s credit policy, which directly influences the likelihood of needing an ADA, needs to strike a delicate balance. Too strict, and it might deter potential customers, limiting sales. Too lenient, and it increases bad debt risk, leading to higher ADA and potentially aggressive collection efforts. The brand must define its acceptable level of risk, which in turn shapes its ADA provision.

- Collection Practices: How a company handles overdue accounts is a crucial brand determinant. Aggressive or unethical collection tactics, while potentially effective in the short term, can severely damage customer relationships, generate negative publicity, and erode brand loyalty. Conversely, a flexible, empathetic, and professional approach to collections, enabled by a realistic ADA and well-defined policies, can preserve customer goodwill, even with those struggling to pay.

- Brand Promise of Reliability: Companies that offer credit are essentially extending trust to their customers. A well-managed ADA allows them to do so sustainably, reinforcing a brand image of reliability and fair dealing. It ensures the company can afford to extend credit without jeopardizing its financial stability, thereby maintaining its ability to serve all customers effectively.

Ethical Considerations in Debt Management and Collections

The very existence of ADA brings with it ethical considerations, especially concerning how businesses manage and attempt to collect on doubtful accounts.

- Fair Practices: Companies have an ethical obligation to ensure their collection practices are fair, transparent, and respectful of customer rights. This means avoiding harassment, deceptive practices, or undue pressure. Technology can facilitate this by ensuring consistent and trackable communication, but human oversight remains critical.

- Data Privacy and Security: As mentioned, using technology for credit assessment and collection involves handling sensitive personal financial data. Ethical guidelines and strict security measures are essential to protect customer privacy and prevent misuse of information, maintaining the brand’s trustworthiness.

- Social Responsibility: In certain industries or economic climates, a compassionate approach to debt collection, such as offering hardship plans or extended payment options, can reinforce a brand’s commitment to social responsibility, potentially yielding long-term brand benefits even if short-term collection is delayed.

Investor Confidence and Corporate Reputation

Ultimately, ADA contributes to the broader narrative of corporate reputation. A company known for its financial prudence, transparency, and ethical conduct is likely to command higher investor confidence and a stronger market position.

- Signal of Competent Management: Accurate ADA reflects management’s ability to assess risk, implement effective credit policies, and foresee potential financial challenges. This signals competence and strong internal controls, which are highly valued by investors and analysts.

- Reduced Volatility: Companies with robust ADA management tend to have more stable earnings, as unexpected bad debt write-offs are minimized. This stability is attractive to investors seeking predictable returns and contributes positively to long-term corporate reputation.

- Competitive Advantage: In competitive markets, a reputation for sound financial management, bolstered by transparent ADA practices, can be a differentiator. It attracts capital, talent, and business partners, providing a distinct competitive edge.

Navigating the Future: Best Practices and Evolving Landscape

The management of Allowance for Doubtful Accounts is not static; it’s a dynamic process that must continually adapt to changing economic conditions, technological advancements, and evolving business strategies. Embracing best practices and a forward-thinking approach is crucial.

Estimating Doubtful Accounts: Methods and Challenges

While technology aids significantly, the core challenge of estimating uncollectible accounts remains.

- Methods: Companies commonly use the “percentage of sales” method (e.g., 1% of credit sales are estimated as uncollectible) and the “aging of receivables” method (classifying receivables by age and applying different uncollectibility percentages to each age bracket). The aging method is generally considered more accurate as it accounts for the increasing risk of default with age.

- Challenges: Estimation is inherently subjective and requires significant judgment. It’s influenced by economic downturns, industry-specific risks, changes in customer demographics, and the effectiveness of a company’s own credit and collection policies. The goal is to strike a balance between conservatism (not overstating assets) and realism (not being overly pessimistic). Regular review and adjustment of estimation methods are vital.

Integrating ADA into Business Operations

Effective ADA management requires an integrated approach across various departments, not just finance.

- Cross-Functional Collaboration: Sales teams need to understand credit policies to avoid selling to high-risk customers unnecessarily. Customer service can play a role in identifying potential payment issues early. Legal teams may be involved in complex collection cases. Finance acts as the central hub, synthesizing information and setting the ADA.

- Proactive Credit Management: Instead of only reacting to overdue accounts, businesses should implement proactive credit vetting processes, establish clear credit limits, and monitor customer payment behavior continuously. This reduces the number of accounts that become doubtful in the first place.

- Continuous Improvement: Regularly review the accuracy of ADA estimates against actual write-offs. Analyze collection efficiency, identify bottlenecks, and refine credit policies based on performance data. This iterative process ensures that ADA remains a relevant and accurate reflection of credit risk.

The Future of Doubtful Accounts Management

The trajectory for ADA management is clearly moving towards greater automation, intelligence, and integration.

- Hyper-Personalization in Collections: AI will enable even more nuanced and personalized communication strategies, tailoring messages and timing to individual customer profiles for maximum effectiveness while preserving positive relationships.

- Blockchain for Supply Chain Finance: While still nascent, blockchain technology could potentially revolutionize credit risk assessment and payment processing in supply chains, offering greater transparency and reducing the incidence of doubtful accounts through smart contracts and immutable transaction records.

- Real-time Risk Adjustment: The ability to dynamically adjust ADA estimates in real-time, based on live economic indicators, market shifts, and customer behavior signals, will become more sophisticated, offering unparalleled accuracy.

- ESG Integration: As Environmental, Social, and Governance (ESG) factors become more critical, the ethical dimensions of debt collection and transparent financial reporting (including ADA) will gain even greater prominence, influencing brand perception and investor decisions.

In conclusion, the Allowance for Doubtful Accounts is far more than a simple accounting entry. It is a critical financial barometer, a testament to a company’s technological prowess, and a significant contributor to its brand equity. In an increasingly digital and interconnected world, mastering ADA means not just managing numbers, but strategically leveraging technology, fostering trust, and building a resilient, reputable business for the long term.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.