Navigating the world of car insurance can feel like deciphering a foreign language, filled with jargon and seemingly endless forms. However, understanding the essential requirements is the first step towards securing the right coverage and peace of mind on the road. This guide will demystify the process, outlining the key information and documentation you’ll need to gather before you even start comparing quotes. Ultimately, obtaining car insurance is a financial transaction that hinges on accurate personal and vehicle data, designed to assess risk and determine your premium.

Gathering Your Personal and Vehicle Information

Before you can effectively shop for car insurance, you need to have a clear picture of who you are as a driver and the vehicle you intend to insure. This foundational information is crucial for any insurance provider to accurately assess risk and calculate your premium. Insurers use this data to understand your driving history, the likelihood of you filing a claim, and the potential cost of replacing or repairing your vehicle. Think of it as building your financial profile in the eyes of the insurance company.

Driver Information: Establishing Your Identity and History

Insurance companies need to know exactly who will be driving the insured vehicle. This extends beyond just your name and address; it encompasses a detailed look at your driving history and personal circumstances, which are all factors in determining your risk profile.

Driver’s License and Identification: The Legal Requirement

The most fundamental requirement is a valid driver’s license. This not only proves your legal right to operate a vehicle but also provides a unique identifier that insurance companies can use to verify your identity and driving record. They will typically ask for your driver’s license number, which is linked to your driving history, including any accidents, tickets, or suspensions. In some cases, other forms of identification may be requested to confirm your identity and residency.

Driving History: A Look at Your Past Performance

Your driving history is perhaps the most significant factor in determining your car insurance premiums. Insurers want to see how responsibly you’ve operated a vehicle in the past. This typically includes:

- Accident History: Details of any past accidents you’ve been involved in, including the date, nature of the accident, and whether you were found at fault. Even minor incidents can influence your rates.

- Traffic Violations: A record of any speeding tickets, DUIs, reckless driving charges, or other traffic violations. A clean driving record generally leads to lower premiums, while a history of violations can significantly increase your costs.

- Years of Driving Experience: The longer you have been licensed and driving, the more experience you are perceived to have, which can sometimes translate to lower rates, especially if your record is clean.

- Previous Insurance Coverage: Information about your past insurance policies, including the dates of coverage and any lapses. Gaps in coverage can be seen as an increased risk by insurers.

Age and Gender: Statistical Risk Factors

While some aspects of insurance pricing are becoming more nuanced, age and gender have historically been significant factors due to statistical data showing differing accident rates among various demographics. Younger, less experienced drivers, and historically, male drivers, have been associated with higher risk, which can impact premiums.

Marital Status: Another Data Point for Risk Assessment

Marital status is another piece of demographic information that insurance companies may consider. Statistically, married individuals have sometimes been shown to have lower accident rates, which could influence their premiums.

Location: Where You Drive Matters

The address where you primarily park your car is a critical piece of information. Insurance rates vary significantly by location due to factors like:

- Theft and Vandalism Rates: Areas with higher rates of car theft or vandalism will typically have higher insurance premiums.

- Traffic Congestion and Accident Frequency: Densely populated urban areas with more traffic often experience higher accident rates, leading to increased insurance costs.

- Weather Conditions: Regions prone to severe weather events like hurricanes, hail, or flooding may see higher premiums to account for potential weather-related damage claims.

- Local Laws and Regulations: State-specific insurance laws and regulations can also influence pricing.

Vehicle Information: Describing the Asset You’re Insuring

The specifics of the car you wish to insure are just as important as your personal details. Each vehicle has unique characteristics that affect its risk profile and the potential cost of claims.

Make, Model, and Year: The Foundation of Vehicle Data

You will need to provide the exact make (e.g., Toyota, Ford), model (e.g., Camry, F-150), and year of manufacture for each vehicle you want to insure. This information allows insurers to access databases that provide details about the vehicle’s safety features, reliability, repair costs, and typical performance.

Vehicle Identification Number (VIN): The Unique Identifier

The Vehicle Identification Number (VIN) is a unique 17-character code that identifies your specific car. It’s essentially the car’s fingerprint and is crucial for insurers to accurately identify the vehicle and pull up its detailed specifications. You can usually find the VIN on the driver’s side dashboard, the driver’s side doorjamb, or on your vehicle’s registration documents.

Safety Features: Reducing Risk with Technology

Modern vehicles come equipped with a variety of safety features that can significantly reduce the risk of accidents and the severity of injuries. Information about these features is important for insurers:

- Anti-lock Braking System (ABS): Helps maintain steering control during hard braking.

- Airbags: Crucial for occupant protection in a collision.

- Electronic Stability Control (ESC): Helps prevent skids and loss of control.

- Advanced Driver-Assistance Systems (ADAS): Features like automatic emergency braking, lane departure warning, and blind-spot monitoring can help prevent accidents.

Anti-Theft Devices: Deterring Crime

The presence of anti-theft devices can lower your risk of vehicle theft, which can translate to lower insurance premiums. This can include:

- Car Alarms: Factory-installed or aftermarket alarm systems.

- Immobilizers: Devices that prevent the engine from starting without the correct key.

- GPS Tracking Systems: Allows for the recovery of stolen vehicles.

Mileage and Usage: How Much You Drive

The estimated annual mileage you drive can also be a factor. Drivers who cover fewer miles are generally considered lower risk, as they spend less time on the road and have fewer opportunities for accidents. You may also be asked about the primary use of your vehicle (e.g., commuting to work, pleasure, business) as this can influence your risk profile.

Current Condition and Modifications: Any Changes from Stock

If your vehicle has undergone any modifications, such as performance upgrades, custom bodywork, or specialized equipment, you must disclose these to your insurance provider. Modifications can increase the value of your vehicle or alter its performance characteristics, potentially affecting repair costs and risk. Similarly, if your vehicle has sustained significant damage, this may need to be disclosed.

Understanding Your Insurance Needs and Policy Options

Once you’ve compiled your personal and vehicle information, the next crucial step is to determine the type and level of car insurance coverage that best suits your financial situation and risk tolerance. This involves understanding the different types of policies available and considering factors that will impact your premium.

Types of Coverage: Building Your Protective Shield

Car insurance policies are not one-size-fits-all. They are composed of various coverage types, each designed to protect you in different scenarios. You’ll need to decide which of these are most important for your needs.

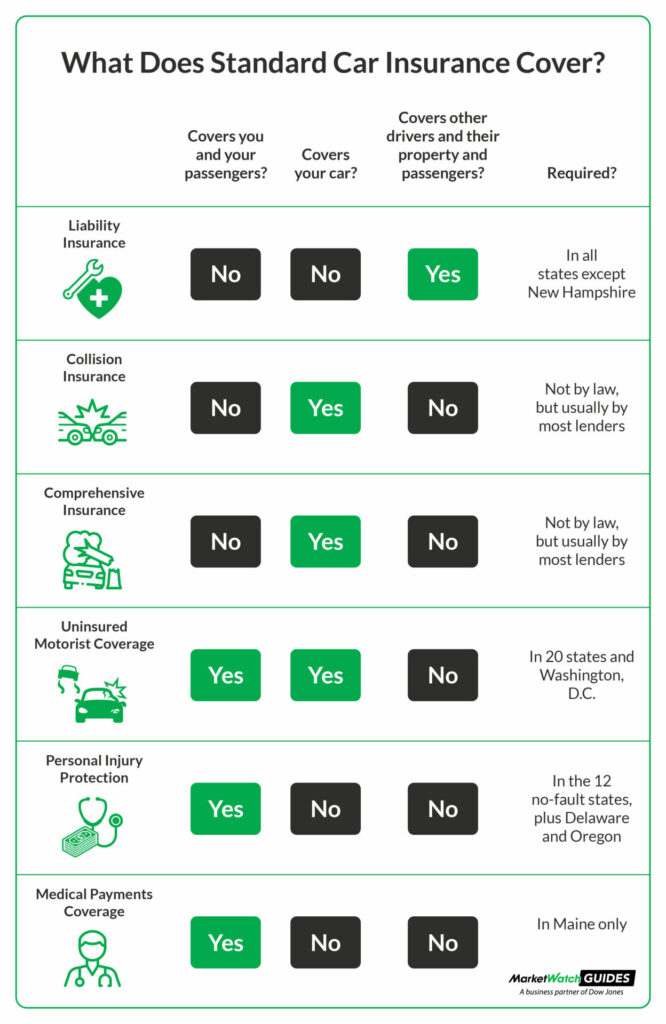

Liability Coverage: Protecting Others and Yourself Financially

Liability coverage is a fundamental component of car insurance and is legally mandated in most states. It’s divided into two parts:

- Bodily Injury Liability: This coverage pays for medical expenses, lost wages, and legal fees for individuals injured in an accident that you cause.

- Property Damage Liability: This coverage pays for damage to another person’s property (e.g., their car, a fence) in an accident that you cause.

You’ll need to choose the limits for your liability coverage, which represent the maximum amount the insurance company will pay out per person, per accident, or for property damage. Higher limits offer greater financial protection but will increase your premium.

Collision Coverage: Repairing Your Own Vehicle After an Accident

Collision coverage helps pay for the repair or replacement of your own vehicle if it’s damaged in a collision with another vehicle or object, regardless of who is at fault. This coverage is often optional unless you have a loan or lease on your vehicle.

Comprehensive Coverage: Protection Beyond Collisions

Comprehensive coverage protects your vehicle from damage caused by events other than collisions. This includes:

- Theft: If your car is stolen.

- Vandalism: Damage caused by intentional destruction.

- Fire: Damage caused by a fire.

- Natural Disasters: Damage from events like hail, floods, or falling trees.

- Animal Collisions: Damage caused by hitting an animal.

Like collision coverage, comprehensive coverage is often optional for vehicles that are owned outright.

Uninsured/Underinsured Motorist (UM/UIM) Coverage: Protection When Others Are Unprepared

This coverage protects you if you’re involved in an accident with a driver who has no insurance (uninsured) or not enough insurance (underinsured) to cover your damages.

- Uninsured Motorist Bodily Injury (UMBI): Covers your medical expenses and lost wages if an uninsured driver injures you.

- Uninsured Motorist Property Damage (UMPD): Covers damage to your vehicle if an uninsured driver hits you.

- Underinsured Motorist (UIM): Covers the difference between the at-fault driver’s insufficient coverage and the cost of your damages.

Medical Payments (MedPay) or Personal Injury Protection (PIP): Covering Your Medical Costs

- Medical Payments (MedPay): This coverage helps pay for medical expenses for you and your passengers, regardless of who is at fault for the accident.

- Personal Injury Protection (PIP): Similar to MedPay, but PIP can also cover lost wages and other related expenses, such as rehabilitation services. PIP is mandatory in some “no-fault” states.

Deductibles: Your Share of the Cost

A deductible is the amount of money you agree to pay out-of-pocket before your insurance coverage kicks in for a claim. You typically choose a deductible for collision and comprehensive coverage. A higher deductible generally results in a lower premium, while a lower deductible means a higher premium. It’s important to select a deductible that you can comfortably afford to pay in the event of a claim.

Factors Influencing Your Premium: Beyond the Basics

While the information you provide is the primary driver of your premium, several other factors come into play:

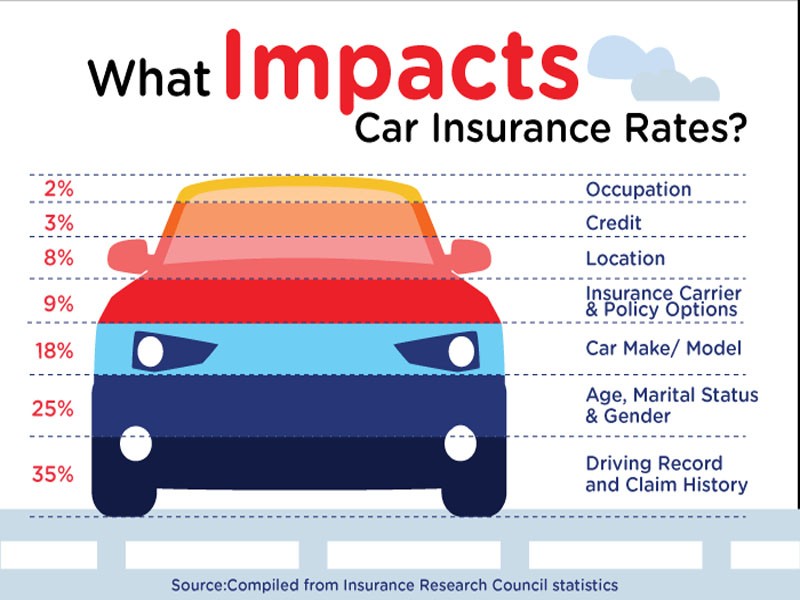

- Driving Record: As mentioned earlier, a history of accidents and violations significantly increases your premium.

- Credit Score (in some states): In many states, insurance companies use credit-based insurance scores to help predict the likelihood of a claim. A higher credit score often leads to lower premiums.

- Vehicle Type and Value: More expensive vehicles, sports cars, or those with higher repair costs will generally have higher premiums.

- Coverage Limits and Deductibles: Higher coverage limits and lower deductibles will result in higher premiums.

- Usage and Mileage: Driving more miles or using your vehicle for business purposes typically increases your premium.

- Location: The ZIP code where your car is garaged plays a significant role due to varying risk factors.

- Discounts: Insurers offer a variety of discounts, such as for safe driving, multi-policy bundles (e.g., home and auto), good student discounts, and low mileage. Actively inquire about available discounts.

Finalizing Your Policy: Quotes, Comparisons, and Documentation

With a clear understanding of the necessary information and your insurance needs, the final steps involve shopping for the best policy and ensuring all your documentation is in order. This stage is crucial for securing not just insurance, but the right insurance at a competitive price.

Obtaining Quotes: The Shopping Process

This is where you actively seek out insurance providers and request price estimates based on your gathered information.

Online Quoting Tools: Convenience and Speed

Most major insurance companies and independent agents offer online quoting tools on their websites. These platforms allow you to input your details and receive an estimated premium in minutes. This is an efficient way to gather initial quotes from multiple providers.

Independent Agents and Brokers: Personalized Assistance

Independent insurance agents or brokers work with various insurance companies. They can help you navigate your options, explain policy details, and find the best coverage at the most competitive price, especially if your situation is complex.

Direct Insurers: Cutting Out the Middleman

Some insurance companies operate on a direct-to-consumer model, meaning you interact with them directly without an agent. This can sometimes lead to lower prices but may offer less personalized guidance.

Comparing Quotes: Making an Informed Decision

Once you have several quotes, it’s essential to compare them carefully. Don’t just look at the bottom-line price; consider these factors:

- Coverage Limits: Ensure that the coverage limits on each quote meet your needs. A cheaper policy with inadequate coverage is not a good deal.

- Deductibles: Compare the deductibles offered for collision and comprehensive coverage.

- Included Coverage: Verify that all the types of coverage you want are included in the quote.

- Reputation and Customer Service: Research the insurer’s reputation for handling claims and their customer service ratings. Online reviews and consumer satisfaction surveys can be valuable resources.

- Discounts Applied: Make sure all applicable discounts have been factored into the premium.

Documentation and Payment: The Final Steps

Once you’ve chosen a policy, you’ll need to finalize the paperwork and arrange for payment.

Proof of Insurance: Your Legal Requirement

Upon purchasing a policy, you will receive an insurance card or certificate of insurance. This document serves as proof that you have the legally required insurance coverage. You should always carry this document with you when driving.

Payment Options: Securing Your Coverage

Insurance premiums can typically be paid in full annually, semi-annually, or in monthly installments. Be aware of any fees associated with monthly payments or automatic withdrawals. Your policy typically won’t be active until your first payment is processed.

By diligently gathering the necessary information, understanding your insurance needs, and carefully comparing quotes, you can confidently secure the car insurance that provides the right protection for your financial well-being and your vehicle.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.