In the landscape of personal finance, few line items are as significant—or as volatile—as health insurance. For the average individual or family, the monthly premium represents a fixed cost that must be balanced against housing, retirement savings, and daily living expenses. However, understanding “how much” health insurance costs per month is rarely as simple as looking at a single price tag. It is a multifaceted calculation involving demographic factors, plan structures, and government subsidies.

As of recent data, the national average for a benchmark Silver plan on the individual marketplace hovers around $450 to $550 per month for a single adult. Yet, this figure can swing wildly from $0 (for those qualifying for heavy subsidies) to over $1,000 for older individuals in high-cost regions. To master your financial planning, you must look beyond the sticker price and understand the mechanics of how these premiums are derived and how they impact your overall net worth.

Understanding the Primary Drivers of Health Insurance Premiums

When a financial advisor looks at a client’s health insurance costs, they aren’t just looking at the monthly bill; they are looking at risk management. The monthly premium is the “subscription fee” for shifting financial risk from the individual to an insurance company. Several regulated factors determine where you fall on the pricing spectrum.

Age and Its Impact on Monthly Rates

Age is perhaps the most influential legal factor in determining premium costs. Under the Affordable Care Act (ACA), insurers are permitted to charge older participants more than younger ones, typically up to a 3:1 ratio. This means a 60-year-old could pay three times what a 21-year-old pays for the exact same coverage. From a personal finance perspective, this necessitates a “healthcare escalator” in your long-term budget, where you must account for rising insurance costs as you age, even before you reach Medicare eligibility at 65.

Geographic Location and Local Market Dynamics

Where you live dictates the level of competition among insurers and the cost of local medical services. For example, a resident of a major metropolitan area like New York City or Chicago may have access to a dozen different providers, driving prices down through competition. Conversely, someone in a rural county might only have one or two options, leading to significantly higher monthly premiums. State regulations also play a role, as some states have “community rating” laws that further restrict how much insurers can vary prices.

Tobacco Use and Premium Surcharges

From a strictly financial standpoint, smoking is one of the most expensive lifestyle choices an individual can make. Insurers are legally allowed to charge tobacco users up to 50% more in premiums than non-smokers. Unlike age-based increases, these surcharges are not covered by federal tax credits, meaning the individual must bear the entire cost of the tobacco surcharge out of pocket. For many, quitting tobacco is the single most effective way to immediately lower their monthly fixed expenses.

Analyzing Plan Categories: Bronze, Silver, Gold, and Platinum

In the individual and small-group markets, plans are categorized into “metal tiers.” These tiers do not reflect the quality of medical care you receive, but rather the “actuarial value” of the plan—essentially, how the financial burden is split between you and the insurer.

Low-Premium, High-Deductible Options (Bronze and Silver)

Bronze plans typically have the lowest monthly premiums but the highest out-of-pocket costs when you actually seek care. These are often the preferred choice for healthy individuals who view health insurance as “catastrophic coverage.” Financially, a Bronze plan makes sense if you have a robust emergency fund to cover a $7,000 or $9,000 deductible should an accident occur.

Silver plans sit in the middle and are the most popular choice because they are the only plans eligible for “cost-sharing reductions.” For many, the Silver tier represents the best balance of monthly affordability and manageable deductibles.

High-Premium, Low-Deductible Options (Gold and Platinum)

Gold and Platinum plans are designed for individuals who anticipate frequent doctor visits or require expensive ongoing prescriptions. While the monthly premium is significantly higher—often 30% to 50% more than a Bronze plan—the insurer pays a much larger portion of medical bills (80% to 90%). For a family with chronic health conditions, paying a higher monthly premium is a strategic move to avoid the financial volatility of high co-pays and deductibles, allowing for a more predictable monthly budget.

The “Metal” Tier Selection Strategy

Choosing a tier is a math problem. To find your true cost, you must calculate:

(Monthly Premium x 12) + Estimated Out-of-Pocket Expenses.

If you are healthy, a lower premium (Bronze) usually results in the lowest annual spend. If you have a planned surgery or chronic illness, the “expensive” Gold plan often results in a lower total annual expenditure because of the reduced cost-sharing.

Employer-Sponsored vs. Individual Marketplace Costs

Where you get your insurance is often more important than what kind of plan you choose. The “cost” of health insurance is frequently hidden in employer-sponsored setups.

The Benefit of Group Rates and Employer Contributions

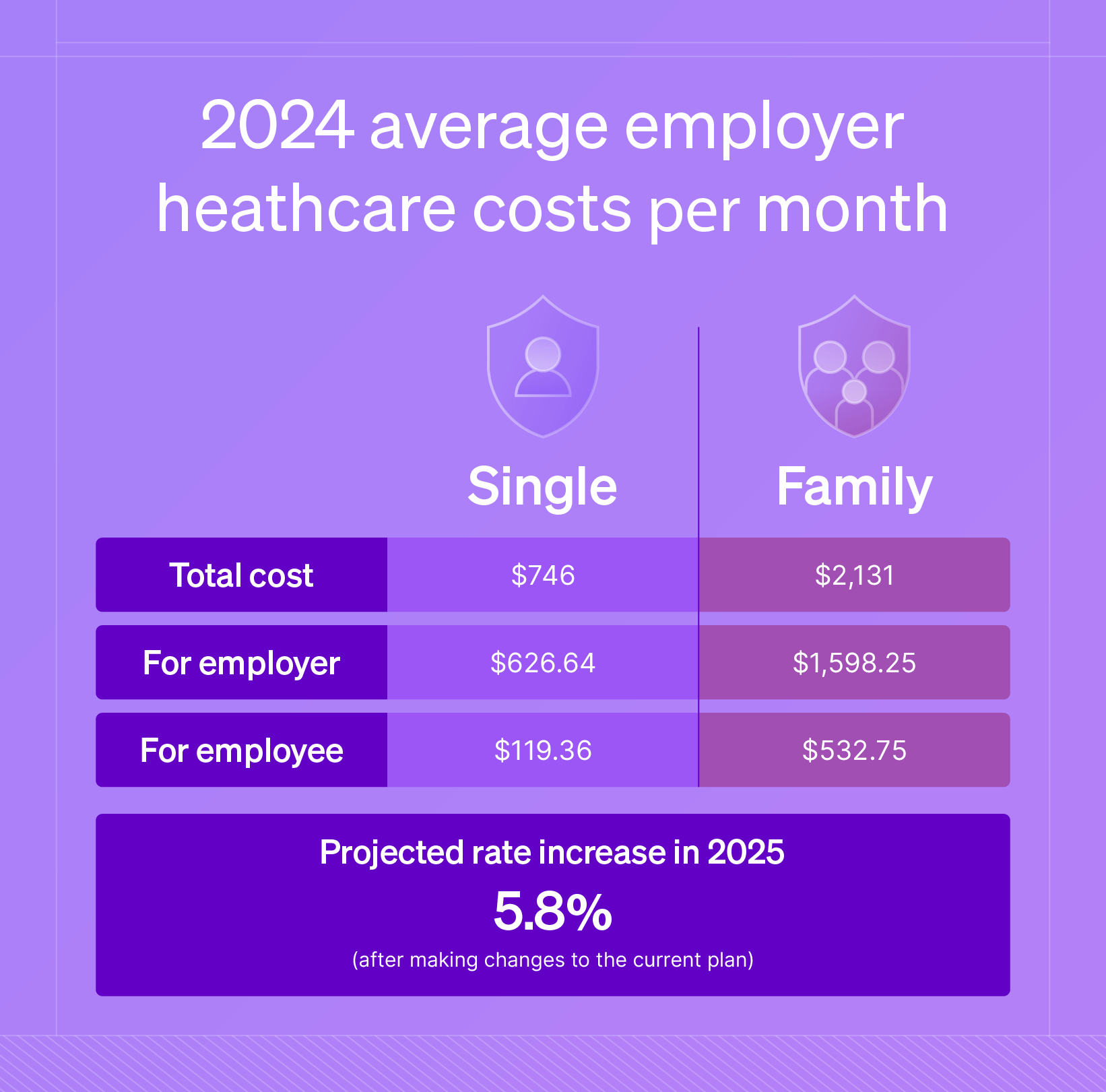

The vast majority of Americans receive insurance through an employer. On average, employers cover about 70% to 80% of the premium for an individual and about 65% for a family plan. If the total cost of a plan is $600 per month, the employee might only see $150 deducted from their paycheck. This is a massive “invisible” benefit. When evaluating a job offer, the quality and cost of the health insurance package can be worth an additional $5,000 to $15,000 in annual “hidden” salary.

Navigating the ACA Marketplace and Private Policies

For the self-employed, freelancers, or those in the “gig economy,” the full cost of health insurance is highly visible. Without an employer to subsidize the premium, individuals must navigate the ACA Marketplace (Healthcare.gov) or buy private off-exchange plans. While the sticker price here is higher, the financial tool known as the “Advanced Premium Tax Credit” (APTC) serves as a vital equalizer for those within certain income brackets.

How Income Impacts Your Monthly Payment: Subsidies and Tax Credits

In the realm of personal finance, health insurance is one of the few products where the price you pay is tied directly to your annual income. This is achieved through federal subsidies that act as a discount on your monthly premium.

Advanced Premium Tax Credits (APTC)

The APTC is a subsidy based on your estimated household income for the year. If your income falls between 100% and 400% of the Federal Poverty Level (and currently even higher due to temporary legislative expansions), the government pays a portion of your premium directly to the insurance company. This can reduce a $500 monthly premium to $50 or even $0. For those managing a tight budget, accurately projecting income is essential to ensure you receive the maximum subsidy without having to pay it back during tax season.

Cost-Sharing Reductions (CSR)

While the APTC lowers your monthly premium, Cost-Sharing Reductions lower your “hidden” costs—deductibles, co-pays, and co-insurance. These are only available on Silver-tier plans for those with incomes below 250% of the Federal Poverty Level. From a financial planning perspective, if you qualify for CSRs, a Silver plan is almost always the most logical choice, as it provides Gold or Platinum-level benefits at a Silver-level price.

Strategic Financial Planning: How to Reduce Your Monthly Health Insurance Outlay

Lowering your health insurance costs requires more than just picking the cheapest plan; it requires utilizing financial tools that provide tax advantages and long-term savings.

Utilizing Health Savings Accounts (HSAs) for Tax Advantages

The Health Savings Account (HSA) is one of the most powerful financial tools available. To qualify, you must be enrolled in a High-Deductible Health Plan (HDHP). While an HDHP might seem risky due to the high deductible, the HSA allows you to contribute pre-tax dollars to pay for medical expenses.

The “Triple Tax Advantage” of an HSA is unmatched:

- Contributions are tax-deductible.

- Growth is tax-free.

- Withdrawals for qualified medical expenses are tax-free.

For those in a high tax bracket, the tax savings alone can effectively “rebate” a portion of their monthly insurance premium.

Comparing Network Types: HMO, PPO, and EPO

The structure of the provider network also dictates the monthly cost.

- HMOs (Health Maintenance Organizations) are usually the cheapest monthly option but require you to stay within a strict network and get referrals for specialists.

- PPOs (Preferred Provider Organizations) offer the most flexibility but come with the highest premiums.

- EPOs (Exclusive Provider Organizations) are a middle ground, offering no out-of-network coverage but generally not requiring referrals.

By choosing an HMO over a PPO, an individual can often save $50 to $100 per month. If your preferred doctors are already in the HMO network, this is an easy way to reduce fixed monthly costs without sacrificing quality of care.

Conclusion

The question of “how much” health insurance costs per month is ultimately a question of how you manage financial risk. Whether you are paying $150 through an employer or $600 on the open market, the goal is the same: to protect your assets from the catastrophic costs of medical care while maintaining monthly liquidity. By understanding the levers of age, location, metal tiers, and subsidies, you can move from being a passive consumer to a strategic manager of your personal finances. In the end, the cheapest plan isn’t always the one with the lowest premium—it’s the one that provides the best total financial protection for your specific life circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.