The arrival of a new driver in the household, whether it’s a teenager fresh from their driving test or an adult who has recently obtained their license, is a significant milestone. Alongside the excitement of newfound independence comes a crucial financial consideration: car insurance. For new drivers, understanding the cost of insurance is paramount, as it often represents a substantial portion of their early automotive expenses. The sticker shock associated with new driver insurance premiums can be considerable, often significantly higher than for experienced drivers. This article delves into the multifaceted factors that contribute to these elevated costs and explores strategies for mitigating them, providing a comprehensive guide for new drivers and their families navigating this essential aspect of car ownership.

The Anatomy of New Driver Insurance Premiums

Insurance premiums are not arbitrary figures; they are meticulously calculated based on a complex algorithm designed to assess risk. For new drivers, this risk assessment is particularly stringent, leading to higher costs. Several key components contribute to this elevated pricing structure.

Inexperience as a Primary Risk Factor

The most significant driver of higher insurance premiums for new drivers is their lack of driving experience. Insurers view any driver with a limited history behind the wheel as inherently riskier. This is due to several factors:

- Unpredictable Behavior: New drivers are still developing their driving habits and judgment. They may be more prone to impulsive decisions, speeding, or distractions.

- Limited Accident History: A long, clean driving record is a testament to a driver’s ability to navigate roads safely. New drivers simply haven’t had the time to build this track record.

- Statistical Data: Insurance companies rely heavily on actuarial data. Statistics consistently show that younger and less experienced drivers are involved in a disproportionately higher number of accidents, often with more severe consequences.

Age and Gender: Statistical Predictors of Risk

While increasingly scrutinized for fairness, age and gender remain significant factors in insurance pricing, particularly for new drivers.

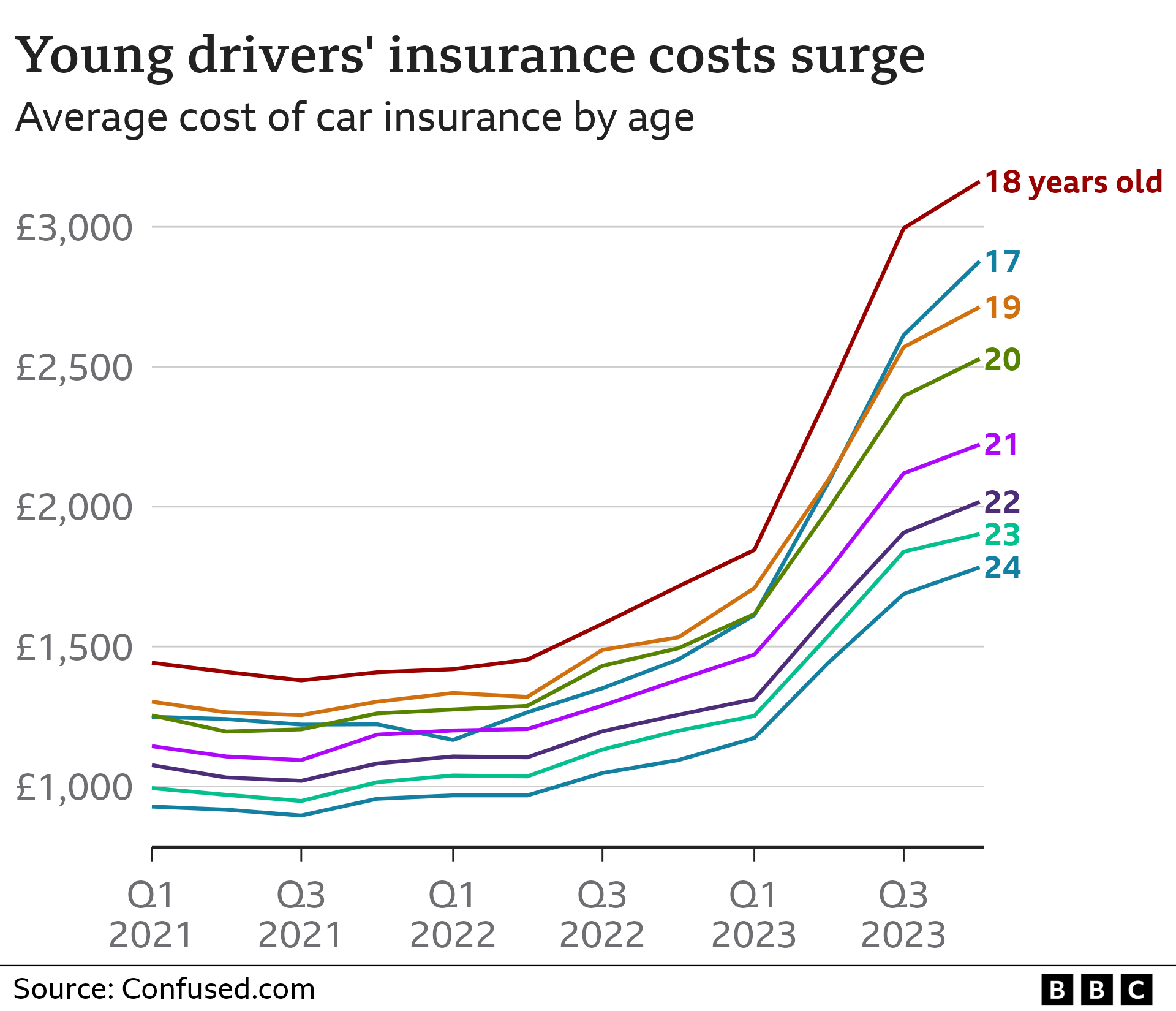

- Younger Drivers (Under 25): This age bracket, especially males, statistically has the highest accident rates. This is often attributed to a combination of factors including impulsivity, risk-taking behavior, and less developed hazard perception skills. Consequently, premiums for drivers under 25 are almost always higher.

- Gender Differences: Historically, male drivers, particularly younger ones, have been found to have higher accident rates than female drivers. While some jurisdictions are moving away from gender-based pricing due to anti-discrimination laws, it can still be a contributing factor in certain regions.

Vehicle Type and Usage: The Impact on Premiums

The type of vehicle a new driver operates and how they use it also play a critical role in determining insurance costs.

- Vehicle Value and Repair Costs: Insuring a high-value or performance-oriented vehicle will naturally be more expensive. These cars often cost more to repair or replace if they are involved in an accident. Insurers factor in the cost of parts, labor, and the likelihood of theft.

- Safety Features: Conversely, vehicles equipped with advanced safety features, such as anti-lock brakes, airbags, electronic stability control, and advanced driver-assistance systems (ADAS), can sometimes lead to slightly lower premiums. These features are designed to prevent accidents or mitigate their severity.

- Annual Mileage: The more miles a driver accumulates, the greater their exposure to potential accidents. Insurers will often ask for an estimate of annual mileage, and higher mileage typically translates to higher premiums.

- Commuting vs. Pleasure Use: Insurers differentiate between vehicles used primarily for commuting to work or school and those used solely for pleasure. Commuting often involves more frequent driving in heavier traffic, potentially increasing risk.

Navigating the Insurance Landscape: Strategies for Cost Reduction

While the initial cost of insuring a new driver can seem daunting, there are several proactive strategies that can help reduce these expenses. These often involve a combination of smart choices regarding insurance policies, vehicle selection, and driving habits.

Policy Adjustments and Discounts

Insurance providers offer a variety of ways to tailor policies and earn discounts, which can significantly impact the final premium.

- Adding to an Existing Policy: For young drivers, being added to a parent’s or guardian’s existing auto insurance policy is often the most cost-effective option. Insurers typically offer a multi-car discount, and the risk is spread across multiple drivers, including experienced ones. This typically leads to a lower per-car premium than purchasing a standalone policy.

- Higher Deductibles: A deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in after an accident. Opting for a higher deductible, while increasing your out-of-pocket expense in the event of a claim, will generally lower your monthly premium. It’s crucial to ensure you can comfortably afford the higher deductible should the need arise.

- Usage-Based Insurance (UBI) Programs: Many insurers now offer UBI programs, also known as telematics or “pay-as-you-drive” insurance. These programs utilize a small device plugged into the car or a smartphone app to track driving habits such as speed, braking, mileage, and time of day. Safe driving can earn significant discounts. However, it’s important to understand what data is being collected and how it will be used.

- Good Student Discounts: For high school and college students, maintaining a good academic record can often qualify them for a “good student” discount. This recognizes that students who are academically motivated may also be more responsible in other areas, including driving. Proof of good grades is typically required.

- Driver Education Courses: Completing an approved driver education or defensive driving course can demonstrate a commitment to safe driving and may result in a discount from some insurers. These courses equip new drivers with advanced skills and knowledge to avoid accidents.

Vehicle Selection and Maintenance: A Financial Double Play

The car itself has a profound impact on insurance costs, and making informed choices can lead to substantial savings.

- Choosing an Insurer-Friendly Vehicle: As mentioned, certain vehicle types are more expensive to insure. Opting for a car that is known for its safety ratings, has lower repair costs, and is less attractive to thieves can lead to lower premiums. Sedans and smaller SUVs generally fall into this category more than sports cars or luxury vehicles.

- Prioritizing Safety Features: When purchasing a vehicle, look for models with excellent safety ratings from organizations like the National Highway Traffic Safety Administration (NHTSA) and the Insurance Institute for Highway Safety (IIHS). Features like automatic emergency braking, lane departure warning, and blind-spot monitoring can not only prevent accidents but might also lead to a slight reduction in insurance costs.

- Vehicle Security: Installing anti-theft devices, such as alarms or tracking systems, can sometimes lead to discounts on comprehensive coverage, which protects against theft and damage.

Building a Positive Driving Record: The Long-Term Strategy

Ultimately, the most effective way to lower insurance costs over time is to build a consistently safe and responsible driving record.

- Adhering to Traffic Laws: The foundation of safe driving is strict adherence to all traffic laws, including speed limits, traffic signals, and rules of the road. Tickets and citations for moving violations will almost certainly lead to increased premiums.

- Avoiding Accidents: The best way to avoid a premium increase due to an accident is to avoid accidents altogether. This means staying alert, defensive driving, and avoiding distractions like mobile phones.

- Demonstrating Responsibility: Insurers value responsibility. This can be demonstrated through consistent safe driving, maintaining a good academic record (if applicable), and actively participating in driver education programs.

- Regular Policy Review: As a driver gains experience and their circumstances change (e.g., moving, changing vehicles, reaching new age milestones), it’s crucial to regularly review their insurance policy. Insurers may not automatically update premiums to reflect lower risk, so proactive communication can lead to adjustments that reflect the driver’s improved profile.

Understanding the Financial Implications

The cost of insuring a new driver is not just a number; it represents a significant financial commitment that needs to be factored into household budgets. Understanding these implications helps in making informed decisions.

The True Cost of New Driver Insurance

The average cost of car insurance for a new driver can vary dramatically based on location, vehicle, coverage levels, and the insurance provider. However, it’s not uncommon for premiums to be several hundred dollars a month, and sometimes even more. This is a substantial expense, especially for young adults who may be on a tighter budget.

- Geographic Location: Premiums are heavily influenced by the area in which the driver lives. Urban areas with higher traffic density and accident rates typically have higher insurance costs than rural areas. States with more stringent regulations or higher rates of uninsured drivers can also see increased premiums.

- Coverage Levels: The type and amount of coverage chosen significantly impact the premium. Comprehensive and collision coverage, which protect against damage to the vehicle from accidents and other incidents, are typically the most expensive components. Minimum state-required liability coverage will be cheaper but offers less protection.

- Insurance Provider: Different insurance companies have different risk appetites and pricing models. Shopping around and obtaining quotes from multiple providers is essential to find the most competitive rates.

Budgeting for Insurance Costs

New drivers and their families must incorporate insurance costs into their overall financial planning.

- Monthly vs. Annual Payments: Many insurers offer discounts for paying the premium in full annually or semi-annually. While this requires a larger upfront payment, it can save money in the long run compared to monthly installments, which sometimes include administrative fees.

- Emergency Fund for Deductibles: As mentioned, choosing a higher deductible can lower premiums, but it necessitates having an emergency fund to cover that deductible if an accident occurs. This fund should be separate from regular savings and readily accessible.

- Prioritizing Needs: It’s important to balance the need for comprehensive insurance coverage with affordability. For a brand-new driver, especially if they are driving an older, less valuable car, it might be more financially prudent to opt for less comprehensive coverage and focus on liability. However, this decision should be made with a full understanding of the risks involved.

The Future of New Driver Insurance

The insurance industry is constantly evolving, and advancements in technology and data analysis are beginning to reshape how new driver insurance is priced and offered.

Technology’s Role in Risk Assessment

Technological innovations are providing insurers with more granular data to assess risk, potentially leading to more personalized and fairer pricing in the future.

- Telematics and Usage-Based Insurance (UBI): As mentioned, UBI programs are becoming increasingly sophisticated. The data collected can provide a more accurate reflection of an individual’s actual driving behavior, moving beyond broad statistical averages.

- AI and Machine Learning: Artificial intelligence and machine learning are being used to analyze vast datasets, identify emerging risk patterns, and predict future outcomes with greater accuracy. This can lead to more nuanced risk assessments for individual drivers.

- Advanced Vehicle Safety Technology: The increasing integration of ADAS in vehicles is also being factored into insurance models. As these technologies become more prevalent and proven effective, they could contribute to lower premiums for vehicles equipped with them.

Evolving Regulations and Consumer Expectations

Regulatory bodies and consumer demand are also pushing the insurance industry towards more equitable and transparent practices.

- Data Privacy and Ethics: As more personal data is collected, concerns about data privacy and the ethical use of this information are growing. Insurers will need to be transparent about how data is collected, stored, and utilized, and consumers will have more power to control their data.

- Focus on Individual Behavior: The trend is shifting from relying solely on demographic factors to a greater emphasis on actual driving behavior. This offers a more direct path for new drivers to prove their safety and reduce their premiums through responsible actions.

- Digital Transformation of Insurance: The insurance purchasing and management process is becoming increasingly digital. Online portals, mobile apps, and streamlined digital claims processing are making it easier for consumers to compare rates, manage their policies, and interact with their insurers.

In conclusion, insuring a new driver is a significant financial undertaking, but by understanding the underlying factors that contribute to the cost and by proactively implementing strategies for cost reduction, new drivers and their families can navigate this essential aspect of car ownership more effectively. A combination of informed policy choices, responsible vehicle selection, and a commitment to safe driving habits will pave the way for more affordable insurance and, more importantly, safer journeys on the road.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.