Social Security is a cornerstone of retirement income for millions of Americans, but understanding how your benefit amount is determined can feel like navigating a complex financial maze. It’s not a simple fixed percentage or a one-size-fits-all calculation. Instead, it’s a sophisticated system designed to provide a progressive benefit, meaning lower earners receive a proportionally larger replacement of their past income than higher earners. This article will demystify the Social Security calculation process, breaking down the key components and explaining how your individual benefit is ultimately shaped.

The Foundation: Your Lifetime Earnings Record

The most crucial element in calculating your Social Security benefit is your earnings history. The Social Security Administration (SSA) tracks all your earnings subject to Social Security taxes throughout your working life. This record is the bedrock upon which your future benefits are built.

Tracking Your Earnings: The SSA’s Role

Every year you work and pay Social Security taxes, those earnings are reported to the SSA by your employer (or by yourself if you are self-employed). These earnings are credited to your “earnings record.” It’s vital to ensure this record is accurate. You can access your Social Security statement, which is available online through the SSA’s website (ssa.gov), to review your earnings history. This statement provides an estimate of your future benefits based on your current earnings and retirement plans. Checking this statement regularly, especially as you approach retirement age, is a prudent financial practice. It allows you to identify any discrepancies or omissions and take steps to correct them well in advance. The SSA has a process for correcting errors, but it’s best to address them proactively rather than waiting until you’re ready to claim benefits.

Inflation Adjustments: Keeping Pace with the Times

Social Security earnings are adjusted for inflation over time. This means that your earnings from earlier years are “indexed” to reflect their value in today’s dollars. This indexing process is essential for ensuring that your entire earnings history is treated fairly when calculating your average earnings. Without inflation adjustments, your earlier, lower earnings would unfairly depress your average, leading to a lower benefit. The SSA uses a specific formula and a national average wage index to perform these adjustments. This ensures that the comparison of your earnings across different years is meaningful and reflects the general wage levels at the time you earned them.

The Core Calculation: Average Indexed Monthly Earnings (AIME)

Once your lifetime earnings are indexed for inflation, the SSA then calculates your Average Indexed Monthly Earnings (AIME). This figure represents your average monthly earnings over your working life, after accounting for inflation.

Identifying Your “Average” Years

To calculate your AIME, the SSA considers your earnings in the 35 years in which you earned the most. If you worked for fewer than 35 years, years with zero earnings will be included, which will lower your average. This is a strong incentive to work as long as possible, ideally for at least 35 years, to maximize your AIME. Even if some of those 35 years had lower earnings, they will be indexed to current wage levels, making them more significant in the overall calculation. The SSA looks at your entire earnings history and selects the 35 highest earnings years, applying the appropriate inflation adjustments to each year’s earnings.

The Monthly Average

After identifying the 35 highest indexed earnings years, the SSA sums up the indexed earnings for those years and then divides the total by 420 (which is 35 years multiplied by 12 months per year). This yields your Average Indexed Monthly Earnings (AIME). The AIME is the crucial number that forms the basis for your Primary Insurance Amount (PIA).

Translating AIME to Benefit: The Primary Insurance Amount (PIA)

Your AIME is then plugged into a formula to determine your Primary Insurance Amount (PIA). The PIA is the amount you would receive if you claim Social Security benefits at your Full Retirement Age (FRA). This formula is progressive, reflecting the Social Security system’s commitment to providing a more substantial income replacement for lower-wage workers.

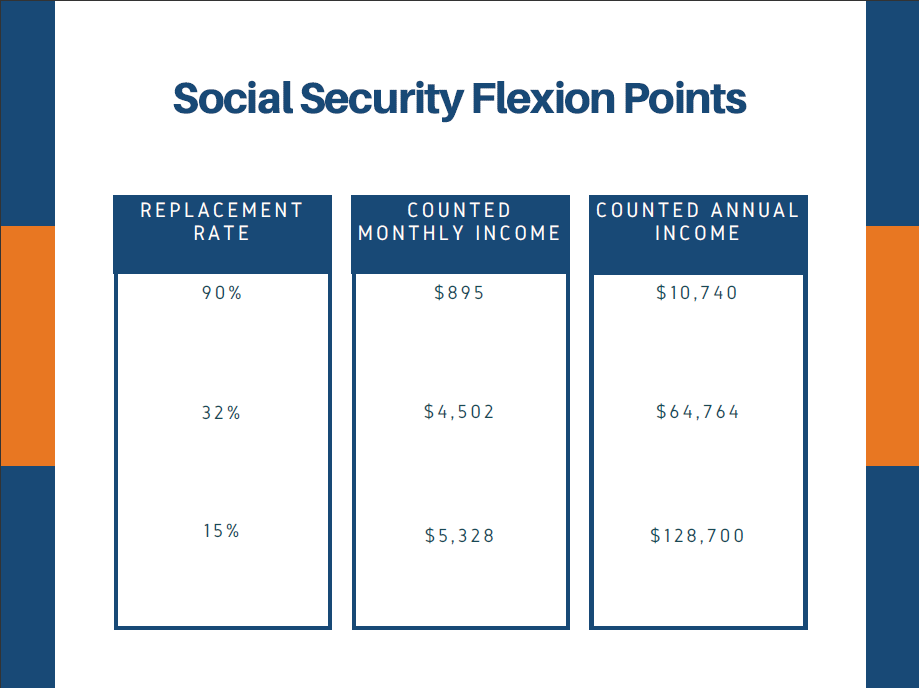

The Benefit Formula: A Stepped Approach

The PIA is calculated using a formula that applies different percentages to different “bend points” of your AIME. These bend points change annually. Generally, the formula works as follows:

- 90% of the first portion of your AIME: The SSA takes 90% of your AIME up to the first bend point. This high percentage for lower earnings ensures a more robust safety net for those who earned less throughout their careers.

- 32% of the middle portion of your AIME: The SSA then applies 32% to the portion of your AIME between the first and second bend points.

- 15% of the remaining portion of your AIME: Finally, 15% is applied to the portion of your AIME above the second bend point.

This stepped approach is what makes Social Security a progressive system. The higher your AIME, the larger the dollar amount falls into the lower percentage brackets. For instance, if your AIME is $1,000, the 90% applies to all of it. If your AIME is $5,000, the 90% applies to the first portion, the 32% to the next, and the 15% to the remainder. The exact dollar amounts for these bend points are adjusted each year based on changes in the national average wage index. This ensures the formula remains relevant and fair over time.

Maximum and Minimum Benefits

There are also maximum and minimum benefit amounts set by the SSA. The maximum possible benefit is for individuals who have consistently earned the maximum taxable income throughout their working lives and claim benefits at age 70. The minimum benefit is for individuals who have worked for many years but earned very little. These caps and floors ensure a degree of equity and predictability within the system.

Adjustments to Your Benefit: Beyond the PIA

Your PIA is your benefit at Full Retirement Age, but several factors can cause your actual benefit amount to be higher or lower.

Early or Delayed Retirement: The Age Factor

One of the most significant adjustments is the age at which you claim benefits.

- Claiming Early: You can claim Social Security benefits as early as age 62. However, for each month you claim before your Full Retirement Age (FRA), your monthly benefit will be permanently reduced. This reduction is calculated on an actuarial basis, meaning it reflects the increased number of payments you are expected to receive over your lifetime. The reduction is substantial, and the longer you claim before your FRA, the lower your monthly payment will be for the rest of your life.

- Claiming Delayed: Conversely, if you delay claiming benefits beyond your FRA, your monthly benefit will increase. For each month you delay past your FRA, up to age 70, your benefit will grow by a certain percentage. This is known as “delayed retirement credits.” These credits are a powerful tool for individuals who can afford to wait to claim, as they significantly boost your lifetime earnings from Social Security. The SSA stops awarding delayed retirement credits after age 70, so there’s no financial advantage to waiting longer than that to claim.

Cost-of-Living Adjustments (COLAs): Protecting Purchasing Power

Social Security benefits are subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help your benefit keep pace with inflation, ensuring that your purchasing power doesn’t erode over time. COLAs are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation rises, your Social Security benefit will likely increase to reflect that rise. This is a critical feature of the Social Security system, providing a measure of financial security and stability for beneficiaries in their retirement years.

Other Adjustments: Windfall Elimination Provision and Government Pension Offset

There are a couple of other less common adjustments that can affect certain individuals:

- Windfall Elimination Provision (WEP): If you receive a pension from work where you did not pay Social Security taxes (e.g., some government jobs), the WEP may reduce your Social Security benefit. This provision aims to prevent individuals from receiving a disproportionately large Social Security benefit based on a short period of work in Social Security-covered employment, combined with a pension from non-covered work.

- Government Pension Offset (GPO): If you receive a pension from federal, state, or local government employment where you did not pay Social Security taxes, and you are also eligible for a Social Security benefit as a spouse or survivor, the GPO may reduce your spousal or survivor benefit. This offset generally reduces your Social Security benefit by two-thirds of the amount of your government pension.

Understanding how your Social Security benefit is calculated is essential for effective retirement planning. By considering your earnings history, the timing of your retirement, and potential adjustments, you can gain a clearer picture of your future financial landscape and make informed decisions to secure your retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.