Navigating the complexities of Social Security benefits can feel like deciphering an intricate financial puzzle, particularly when it comes to understanding how those crucial monthly payments are determined. The Social Security Administration (SSA) employs a standardized, albeit multifaceted, formula to calculate benefits, ensuring a degree of fairness and predictability for millions of Americans. This process, rooted in an individual’s earnings history, is designed to provide a foundational level of income security throughout retirement, disability, and for survivors. Understanding the core components of this calculation is essential for effective retirement planning and for making informed decisions about your future financial well-being.

The Foundation: Your Earnings Record and Average Indexed Monthly Earnings (AIME)

At the heart of Social Security benefit calculation lies your lifetime earnings history. The SSA meticulously tracks your income subject to Social Security taxes throughout your working life. This data forms the basis for determining your eligibility and the amount of your benefit. The process begins by identifying your highest-earning years and then adjusting those earnings for inflation to reflect their value in today’s dollars.

Identifying Your “Credited” Earnings

Social Security credits are earned based on your annual earnings. For 2024, you earn one credit for every $1,730 in earnings, up to a maximum of four credits per year. This means that an individual needs to earn $6,920 in 2024 to reach the maximum of four credits. The total number of credits you accumulate over your working life is crucial for establishing your eligibility for benefits. To qualify for retirement benefits, for instance, most workers need 40 credits, which typically equates to about 10 years of work. For disability or survivor benefits, the credit requirement can vary based on your age at the time of disability or death. The SSA keeps a detailed record of your earnings history, which you can access and review through your “my Social Security” account on the SSA’s website. Regularly checking this record is a prudent step to ensure accuracy and to gain a clearer picture of your potential future benefits.

Adjusting for Inflation: Indexing Your Earnings

Simply summing up your past earnings wouldn’t be a fair way to calculate benefits today, as the value of a dollar has changed significantly over time due to inflation. To address this, the SSA “indexes” your earnings. This means that your earnings from earlier years are adjusted to reflect their approximate value in the most recent year before you become eligible for benefits. For example, if you earned $10,000 in 1980, that amount would be adjusted upwards to reflect what that $10,000 would be worth in today’s economy. This indexing process ensures that your past contributions are valued in a comparable economic context to current earnings. The indexing is applied up to age 60. Earnings after age 60 are counted at their actual dollar amount.

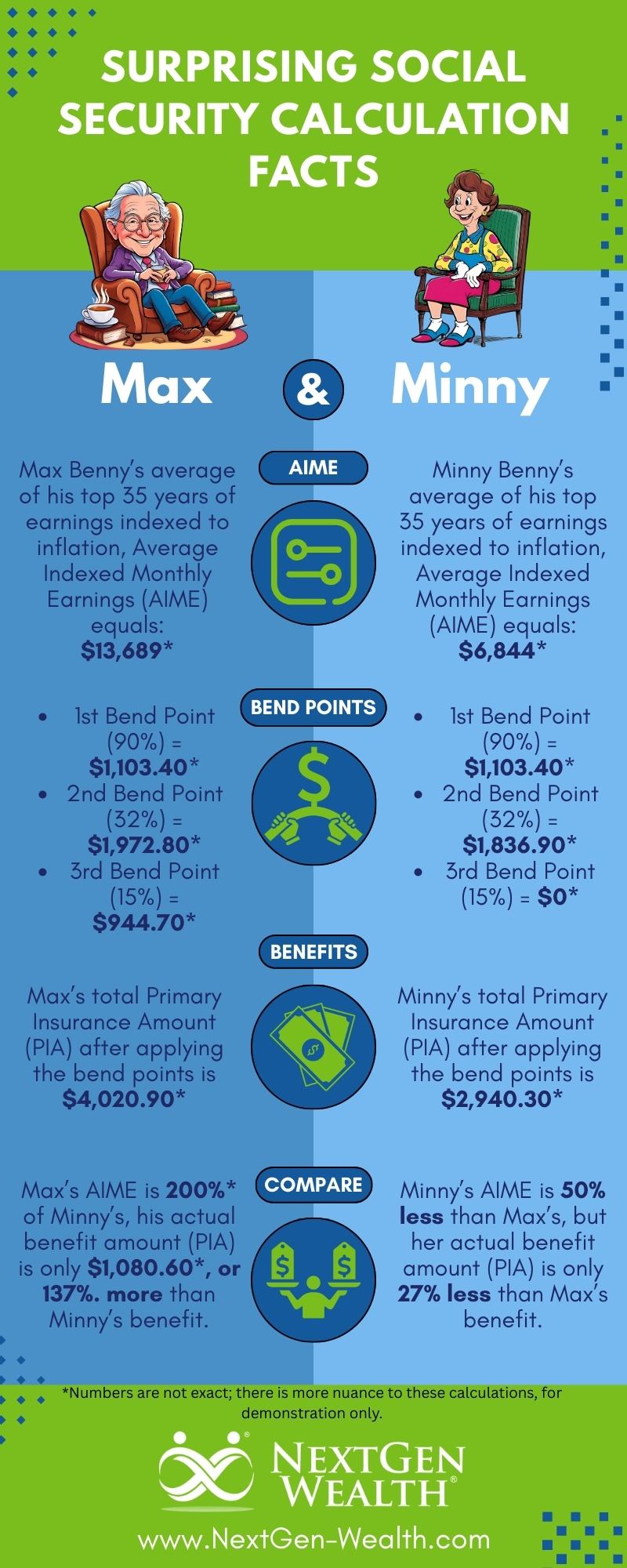

Calculating Your Average Indexed Monthly Earnings (AIME)

Once your earnings have been indexed, the SSA identifies the 35 years in which you earned the most. These highest earning years, after being indexed for inflation, are then summed up and divided by 35 to calculate your Average Indexed Monthly Earnings (AIME). This AIME is a crucial figure, representing your average monthly income over your 35 highest-earning years, adjusted for inflation. It’s important to note that if you have fewer than 35 years of earnings, the years with no earnings will be counted as zero, which will lower your AIME. Conversely, if you have more than 35 years of earnings, the SSA will use the 35 years with the highest indexed earnings. This averaging mechanism is designed to reflect a substantial portion of your working career and to provide a more accurate representation of your earning capacity.

From AIME to Primary Insurance Amount (PIA): The Benefit Formula

Your AIME is the raw material, but it doesn’t directly translate into your monthly benefit payment. The SSA uses a progressive formula to convert your AIME into your Primary Insurance Amount (PIA). The PIA represents the benefit amount you would receive if you start collecting benefits at your full retirement age. This formula is intentionally progressive, meaning it replaces a higher percentage of income for lower-wage earners than for higher-wage earners. This is a core principle of Social Security, aiming to provide a more substantial safety net for those who have earned less throughout their careers.

Understanding the “Bend Points”

The PIA calculation involves applying specific “bend points” to your AIME. These bend points are set by law and are adjusted annually for inflation. For individuals who will reach age 62 in the current year (2024), the formula is as follows:

- 90% of the first $1,116 of your AIME

- 32% of your AIME between $1,116 and $6,721

- 15% of your AIME above $6,721

Let’s break down what this means with an example. Suppose your AIME is $3,000.

The calculation would be:

(0.90 * $1,116) + (0.32 * ($3,000 – $1,116)) = $1,004.40 + (0.32 * $1,884) = $1,004.40 + $602.88 = $1,607.28.

So, your PIA would be approximately $1,607.28.

This formula demonstrates the progressive nature of the Social Security system. The highest percentage of income replacement applies to the lowest portion of your AIME. As your AIME increases, the percentage of income replaced by Social Security decreases. This ensures that individuals with lower lifetime earnings receive a proportionally larger share of their pre-retirement income from Social Security, while higher earners receive a smaller, but still significant, percentage. The exact bend points change each year, so the PIA for an individual who reaches age 62 in a different year will be calculated using that year’s specific bend points.

The Impact of Full Retirement Age

Your PIA is calculated based on retiring at your “full retirement age.” This is the age at which you are entitled to receive 100% of your PIA. For individuals born between 1943 and 1954, full retirement age is 66. For those born in 1960 or later, full retirement age is 67. If you choose to start receiving benefits before your full retirement age (as early as age 62), your monthly benefit will be permanently reduced. This reduction is calculated based on the number of months you claim early. Conversely, if you delay collecting benefits beyond your full retirement age (up to age 70), you will earn delayed retirement credits, which increase your monthly benefit amount. These credits are applied at a rate of 8% per year for each year you delay past your full retirement age.

Adjustments and Special Circumstances Affecting Your Benefit

While the AIME and PIA are the core components, several other factors can influence your final monthly Social Security benefit. These include cost-of-living adjustments (COLAs), early or delayed retirement, and spousal or survivor benefits.

Cost-of-Living Adjustments (COLAs)

To protect the purchasing power of Social Security benefits from inflation, the SSA provides annual Cost-of-Living Adjustments (COLAs). These adjustments are typically announced in October and take effect in January of the following year. The COLA is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which measures the average change over the year in the prices paid by urban wage earners and clerical workers for a representative basket of consumer goods and services. If inflation rises, your Social Security benefit will also increase to help you keep pace with the rising cost of living. This automatic adjustment is a critical feature of the Social Security program, ensuring that benefits retain their real value over time.

Early and Delayed Retirement Provisions

As mentioned earlier, the age at which you begin receiving benefits significantly impacts your monthly payment. Claiming benefits early, between ages 62 and your full retirement age, results in a permanently reduced benefit. The reduction is substantial; for example, if you claim at age 62 and your full retirement age is 67, your benefit will be reduced by approximately 30%. On the other hand, delaying benefits beyond your full retirement age, up to age 70, can significantly increase your monthly payments. Each year you delay, you accrue delayed retirement credits, effectively boosting your future monthly income. The decision of when to claim benefits is a personal one, often influenced by your health, financial situation, and life expectancy, but understanding these adjustment factors is crucial for making the optimal choice.

Spousal and Survivor Benefits

Social Security benefits are not solely for the worker who earned them. Spousal benefits allow a spouse to receive benefits based on their partner’s earnings record. If you are married, you may be eligible for up to 50% of your spouse’s PIA if you claim benefits at your full retirement age. Survivor benefits are paid to eligible family members after a worker has died. These can include a widow or widower, children, or dependent parents. The amount of survivor benefits typically ranges from 71.25% to 100% of the deceased worker’s PIA, depending on the survivor’s age and relationship to the deceased. These provisions highlight the broader social safety net function of Social Security, providing support to families in times of need.

Maximizing Your Social Security Benefits

Understanding how Social Security benefits are calculated is the first step toward maximizing them. Several strategic decisions can positively influence the amount of your monthly payments, allowing you to enjoy a more secure retirement.

Working Longer and Delaying Benefits

The most straightforward way to increase your Social Security benefit is to continue working and delay claiming benefits beyond your full retirement age. As discussed, each year you delay, you earn delayed retirement credits, which can add a substantial amount to your monthly payments. For those with a longer life expectancy or who can afford to wait, this strategy can lead to tens of thousands of dollars more in lifetime benefits. Even working a few extra years can significantly boost your average indexed monthly earnings, as those higher-earning years replace lower-earning or zero-earning years in your 35-year calculation.

Ensuring Accuracy in Your Earnings Record

It is paramount to verify the accuracy of your Social Security earnings record. Errors can occur, and discrepancies can lead to a lower benefit calculation. As mentioned earlier, you can access your earnings history through the “my Social Security” account on the SSA’s website. Review this record annually for any inaccuracies, such as unreported self-employment income or incorrect wage data. If you find an error, you can contact the SSA to have it corrected. Catching and rectifying errors early is much easier than trying to do so years later when the original records may be harder to access.

Understanding the Impact of Taxes on Benefits

While not a direct calculation of benefits, it’s important to be aware that a portion of your Social Security benefits may be subject to federal income tax. The amount of tax depends on your combined income, which includes your adjusted gross income, any non-taxable interest, and one-half of your Social Security benefits. For those with higher incomes, up to 85% of their Social Security benefits can be taxable. State income taxes on Social Security benefits also vary by state. Understanding these potential tax implications can help you plan your overall retirement income strategy more effectively and ensure you are prepared for any tax liabilities.

In conclusion, Social Security benefit calculation is a systematic process designed to provide a foundation of financial security. By understanding the interplay of your earnings history, average indexed monthly earnings, and the progressive benefit formula, you can gain valuable insights into your potential future payments. Strategic decisions regarding retirement timing, ensuring accuracy in your earnings record, and being aware of tax implications can all play a significant role in maximizing the benefits you receive, contributing to a more financially secure future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.