Inflation, the persistent rise in the general price level of goods and services in an economy over a period of time, is a fundamental economic concept that impacts everyone. Understanding how it’s calculated is crucial for making informed financial decisions, whether you’re a consumer, an investor, a business owner, or a policymaker. While the abstract idea of rising prices might seem straightforward, the actual calculation of inflation involves specific methodologies and data collection processes. This article will delve into the core principles and practical methods used to quantify this vital economic indicator, focusing on the realm of personal finance and its implications.

Understanding the Fundamentals of Inflation Calculation

At its heart, calculating inflation involves measuring the change in prices of a basket of goods and services over time. This basket is not arbitrary; it’s carefully curated to represent the typical consumption patterns of households. The most common way to quantify this change is through the use of price indexes, with the Consumer Price Index (CPI) being the most widely recognized and utilized for personal finance.

The Concept of a “Basket of Goods”

Imagine a typical household’s monthly shopping list. It would include items like groceries (bread, milk, eggs), utilities (electricity, gas), transportation (gasoline, public transport fares), housing (rent, mortgage payments), healthcare (doctor visits, prescription drugs), and entertainment (movie tickets, streaming subscriptions). The “basket of goods and services” used to calculate inflation aims to mirror this representative spending.

Government statistical agencies, such as the Bureau of Labor Statistics (BLS) in the United States, conduct extensive surveys to determine what consumers actually buy and in what quantities. These surveys, often called Consumer Expenditure Surveys, help establish the relative importance of different items in the basket. For instance, if households spend a larger proportion of their income on housing than on entertainment, housing will carry a greater weight in the inflation calculation.

The Role of Price Indexes

A price index is a statistical measure that tracks the average change in prices of a specified set of goods and services. It’s essentially a snapshot of prices at a particular point in time, compared to a baseline period. The baseline period is assigned a value of 100, and subsequent periods are measured relative to this base.

For example, if the CPI for a base year is 100, and in the following year it rises to 105, this indicates that prices, on average, have increased by 5%. This 5% represents the inflation rate for that period.

Weighted Averages: Reflecting Consumer Spending

The “basket of goods” approach relies heavily on a concept called a weighted average. Not all items in the basket have an equal impact on the overall inflation rate. As mentioned earlier, items that consumers spend more on have a higher weight. This weighting ensures that price changes in more significant spending categories have a more pronounced effect on the calculated inflation rate.

For example, a 10% increase in the price of gasoline might have a greater impact on the overall CPI than a 10% increase in the price of a single luxury item that very few people purchase. The weights are periodically updated to reflect changes in consumer spending habits. This dynamic adjustment is critical for the index to remain a relevant measure of inflation.

Calculating the Inflation Rate: The Consumer Price Index (CPI) in Detail

The Consumer Price Index (CPI) is the primary tool for measuring inflation from a consumer’s perspective. It’s calculated by tracking the prices of a fixed basket of goods and services over time and comparing the current cost of this basket to its cost in a base period.

Gathering Price Data

The process begins with meticulous data collection. BLS price collectors visit thousands of retail stores, service establishments, rental units, and doctors’ offices across the country every month. They record the prices of thousands of specific items within the defined CPI basket. This data collection is done systematically to ensure accuracy and consistency.

The items collected are not just broad categories but specific products with defined characteristics. For instance, instead of just tracking “bread,” collectors might record the price of a specific brand and size of white bread at a particular supermarket. This level of detail helps to isolate actual price changes from changes in product quality or features.

Constructing the CPI Basket

The CPI basket is composed of goods and services categorized into eight major groups:

- Food and beverages: Includes food at home, food away from home, and alcoholic beverages.

- Housing: Covers rent of primary residence, owners’ equivalent rent, and utility costs.

- Apparel: Includes clothing and footwear.

- Transportation: Encompasses new and used motor vehicles, gasoline, and public transportation.

- Medical care: Includes prescription drugs, medical services, and medical supplies.

- Recreation: Covers sporting goods, electronics, and entertainment services.

- Education and communication: Includes tuition, textbooks, and telephone services.

- Other goods and services: A miscellaneous category including tobacco products, personal care items, and financial services.

The weights for each of these groups, and for specific items within them, are determined by the Consumer Expenditure Survey. These weights are updated periodically, typically every two years, to ensure the CPI reflects current spending patterns.

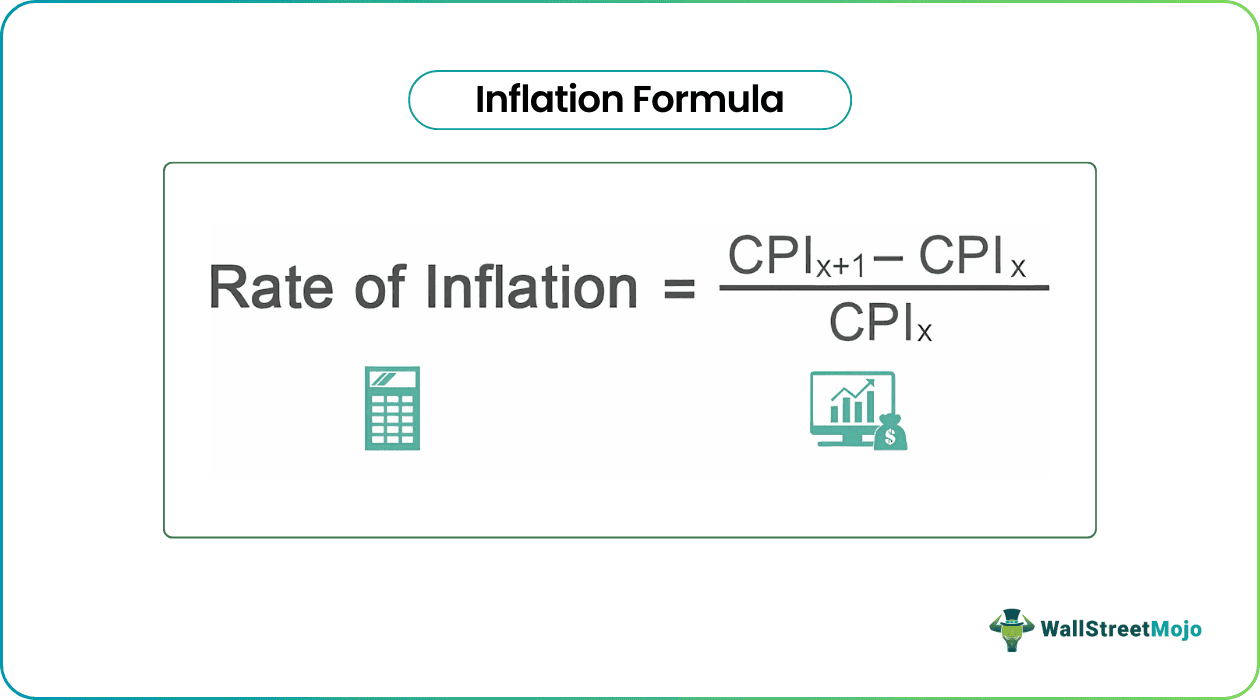

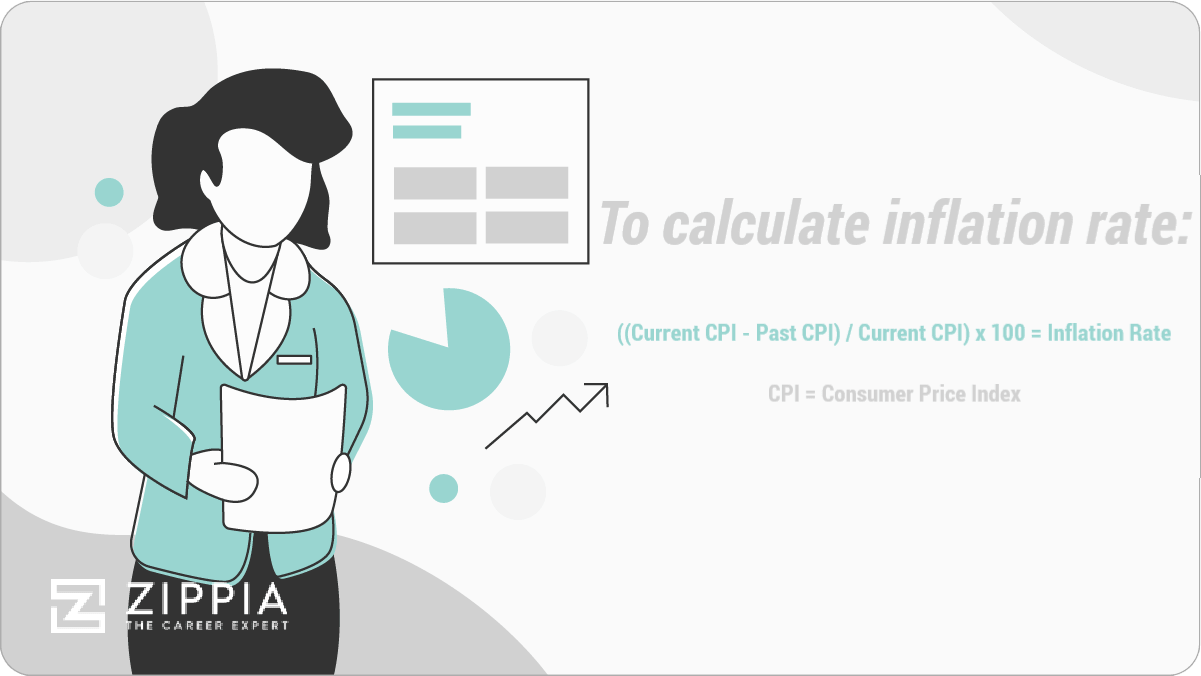

The Inflation Rate Formula

The inflation rate is calculated as the percentage change in the CPI from one period to another. The most common periods used are month-over-month and year-over-year.

The formula for calculating the inflation rate between two periods is:

Inflation Rate = [ (CPI in Current Period – CPI in Previous Period) / CPI in Previous Period ] * 100

For example, let’s say the CPI in January was 275.3 and in February it was 277.1.

- Month-over-month inflation:

[(277.1 – 275.3) / 275.3] * 100 = (1.8 / 275.3) * 100 ≈ 0.65%

This means that, on average, prices rose by approximately 0.65% from January to February.

If we want to calculate the year-over-year inflation rate, we would compare the CPI of a given month to the CPI of the same month in the previous year. For instance, if the CPI in March 2023 was 298.1 and in March 2024 it was 305.7:

- Year-over-year inflation:

[(305.7 – 298.1) / 298.1] * 100 = (7.6 / 298.1) * 100 ≈ 2.55%

This indicates an annual inflation rate of approximately 2.55%.

Beyond the CPI: Other Measures and Considerations

While the CPI is the most commonly cited measure of inflation for personal finance, other price indexes exist and are important for different economic analyses. Understanding these nuances provides a more comprehensive picture of price level changes.

The Producer Price Index (PPI)

The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. Unlike the CPI, which tracks prices from the consumer’s perspective, the PPI tracks prices from the seller’s perspective. It measures price changes for goods and services at various stages of production, from raw materials to finished goods.

The PPI is often considered a leading indicator of inflation because changes in producer prices can eventually be passed on to consumers. If raw material costs increase significantly, manufacturers may eventually raise their prices for finished goods, which will then be reflected in the CPI. The PPI data is broken down by industry and stage of processing, providing valuable insights into price pressures throughout the supply chain.

The Personal Consumption Expenditures (PCE) Price Index

The Personal Consumption Expenditures (PCE) price index, released by the Bureau of Economic Analysis (BEA), is another important inflation measure. Many economists and the Federal Reserve consider the PCE price index to be a more comprehensive measure of inflation than the CPI for several reasons.

Firstly, the PCE index uses a different formula for calculating price changes that tends to be more flexible in accounting for substitution effects. When prices rise for one good, consumers may switch to cheaper alternatives. The PCE index can capture this substitution more readily than the CPI, which uses fixed weights for longer periods.

Secondly, the PCE index includes a broader range of goods and services, including those provided by the government or as employer-provided benefits, which are not fully captured by the CPI. For instance, employer-provided health insurance is reflected in the PCE index, while its impact on household budgets is less directly measured by the CPI. The Federal Reserve uses the PCE price index as its primary inflation target.

Adjusting for Inflation: Real vs. Nominal Values

One of the most critical applications of inflation calculation in personal finance is the ability to distinguish between nominal and real values. Nominal values are expressed in current prices, while real values are adjusted for inflation to reflect purchasing power.

For example, if your salary increases by 3% in a year, but the inflation rate was 4%, your nominal income has gone up, but your real income (your purchasing power) has actually decreased. This distinction is vital for understanding the true growth of your wealth and income over time. To calculate real income, you would divide your nominal income by the price level (often represented by the CPI) and multiply by 100.

Real Income = (Nominal Income / CPI) * 100

Similarly, the real return on an investment accounts for the erosion of purchasing power due to inflation. A nominal return of 5% on an investment might seem good, but if inflation is 3%, your real return is only 2%.

The Impact of Inflation on Personal Finance

Understanding how inflation is calculated is not just an academic exercise; it has profound and direct implications for managing your personal finances, planning for the future, and protecting your wealth.

Budgeting and Purchasing Power

The most immediate impact of inflation is on your purchasing power. When prices rise, the same amount of money buys fewer goods and services. This means your budget needs to stretch further to cover essential expenses. A persistent rise in inflation can lead to a decrease in your standard of living if your income doesn’t keep pace. Regularly reviewing your budget and making adjustments to accommodate rising costs is essential. For instance, if the cost of groceries has significantly increased, you might need to re-evaluate your spending in other discretionary areas.

Savings and Investments

Inflation is a silent enemy of savers and investors. Money held in cash or low-interest savings accounts loses value over time as inflation erodes its purchasing power. To maintain and grow your wealth, your investments need to generate returns that outpace inflation.

This is why understanding real returns is critical. A savings account offering a 1% nominal interest rate when inflation is 3% is effectively losing you 2% of your purchasing power each year. Similarly, when considering investments like bonds or stocks, it’s crucial to look beyond the nominal yield or price appreciation and consider the real return after accounting for inflation.

Retirement Planning

For long-term goals like retirement, inflation is a significant factor that must be factored into planning. The amount of money you will need in retirement will be substantially higher than today’s equivalent due to the cumulative effect of inflation over decades.

When calculating how much you need to save for retirement, it’s essential to project future expenses in “future dollars” by assuming a realistic inflation rate. Failing to account for inflation in retirement planning can lead to a severe shortfall in your retirement funds, forcing you to live on less than you anticipated. This underscores the importance of investing in assets that have historically provided returns above inflation over the long term.

Debt Management

The impact of inflation on debt can be mixed. For borrowers with fixed-rate debt, such as mortgages or car loans, inflation can actually be beneficial. As inflation rises, the real value of the debt you owe decreases over time. This means that the money you repay in the future is worth less in terms of purchasing power than the money you borrowed. However, this benefit is offset by the fact that your ability to repay that debt might be strained if your income doesn’t keep pace with inflation. For those with variable-rate debt, rising inflation often means rising interest rates, making debt more expensive.

In conclusion, understanding how inflation is calculated, primarily through price indexes like the CPI, is fundamental to navigating the economic landscape and making sound financial decisions. By recognizing the impact of inflation on purchasing power, savings, investments, and long-term goals, individuals can better protect their financial well-being and work towards achieving their financial objectives in an ever-changing economic environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.