In the realm of personal finance, few concepts carry as much weight or potential for wealth creation as compound interest. Often referred to by Albert Einstein as the “eighth wonder of the world,” compound interest is the engine that drives long-term investment growth and retirement security. Understanding how to figure out compound interest is more than just a mathematical exercise; it is a fundamental pillar of financial literacy that allows individuals to move from passive saving to strategic wealth building.

At its core, compound interest is the interest calculated on the initial principal, which also includes all the accumulated interest from previous periods. Unlike simple interest, which only grows based on the original amount deposited, compound interest creates a “snowball effect,” where your money begins to work for you, generating its own earnings. This guide explores the mechanics, the mathematics, and the strategic application of compound interest to help you navigate your financial journey with precision.

Understanding the Fundamentals: Simple vs. Compound Interest

Before diving into the complex calculations, it is essential to distinguish between the two primary ways interest is accrued. This distinction is often what separates a stagnant savings account from a high-performing investment portfolio.

The Mechanics of Simple Interest

Simple interest is straightforward. It is calculated solely on the principal amount—the original sum of money invested or borrowed. For example, if you invest $10,000 at a 5% simple interest rate for three years, you would earn $500 each year. At the end of the term, you would have $11,500. The amount earned remains constant because the interest does not get reinvested to earn more interest. While simple interest is common in short-term personal loans or car titles, it is rarely the vehicle used for long-term wealth accumulation.

The Dynamics of Compound Interest

Compound interest operates on the principle of reinvestment. Using the same $10,000 at a 5% interest rate, the first year would yield $500, bringing the total to $10,500. In the second year, the 5% interest is calculated on the new total of $10,500, yielding $525. By the third year, you are earning interest on $11,025. Over short periods, the difference seems negligible, but over decades, the divergence between simple and compound interest becomes exponential.

The Importance of the Compounding Period

The frequency with which interest is compounded—daily, monthly, quarterly, or annually—has a significant impact on the final total. The more frequently interest is added to the principal, the faster the balance grows. For a savvy investor, understanding the compounding frequency is just as important as the interest rate itself, as it determines the Effective Annual Yield (EAY).

The Mathematical Blueprint: The Compound Interest Formula

To truly master your finances, you must understand the formula that governs your wealth. While modern software can do the heavy lifting, knowing the “how” behind the numbers allows you to run mental simulations and better evaluate financial products.

Breaking Down the Standard Formula

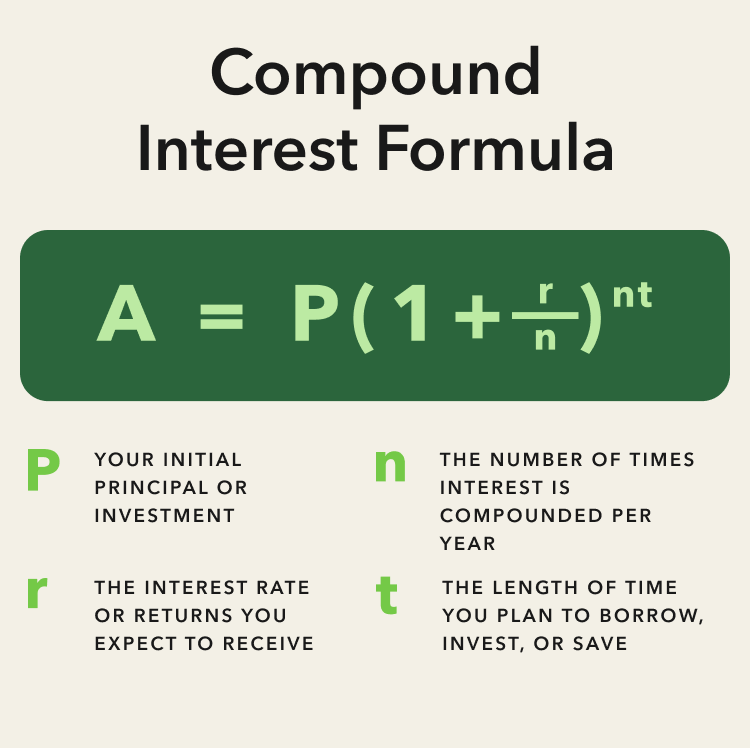

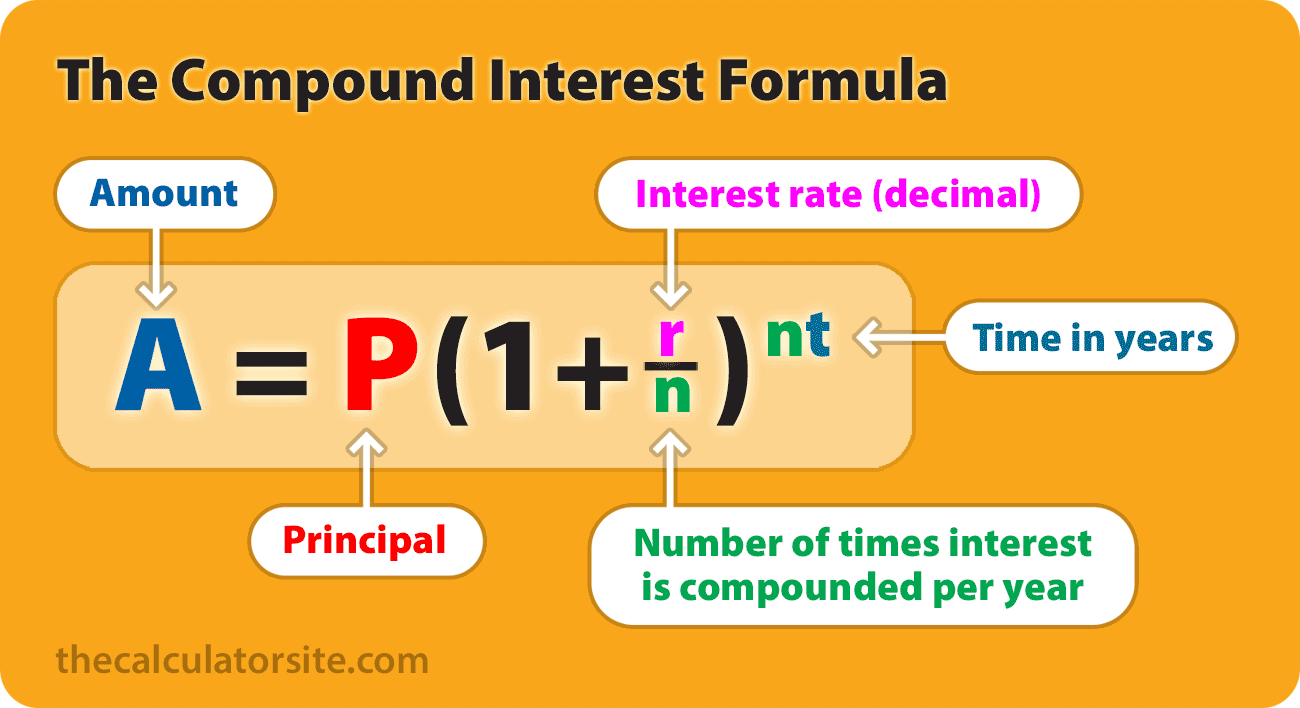

The standard formula for compound interest is:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest.

- P = the principal investment amount (the initial deposit).

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per unit t.

- t = the time the money is invested or borrowed for.

A Step-by-Step Calculation Walkthrough

Suppose you deposit $5,000 into a high-yield savings account with an annual interest rate of 4% (0.04), compounded monthly (n=12), for a period of 10 years (t=10).

- Divide the rate by the frequency: 0.04 / 12 = 0.00333.

- Add one to this result: 1 + 0.00333 = 1.00333.

- Calculate the total periods: 12 * 10 = 120.

- Raise the result to the power of the periods: (1.00333)^120 ≈ 1.4908.

- Multiply by the principal: 5,000 * 1.4908 = $7,454.16.

Through this process, you can see exactly how your money scales over a decade without any additional contributions.

The Role of Continuous Compounding

In some advanced financial instruments, interest is compounded continuously. This represents the absolute limit of compounding frequency. The formula changes to A = Pe^(rt), where e is Euler’s number (approximately 2.71828). While less common for average savings accounts, it is a vital concept in institutional finance and options pricing.

Strategic Tools for Calculation and Projection

In the digital age, figuring out compound interest doesn’t require a slide rule. There are several professional-grade tools and methods that investors use to project their financial future.

Utilizing Spreadsheet Software

Excel and Google Sheets are the gold standard for personal finance management. The most common function used for compound interest is the FV (Future Value) function. The syntax is =FV(rate, nper, pmt, [pv], [type]).

- Rate: The interest rate per period.

- Nper: The total number of payment periods.

- Pmt: The payment made each period (if you are adding monthly).

- Pv: The present value or principal.

Spreadsheets allow you to create “what-if” scenarios, such as how your retirement fund changes if you increase your monthly contribution by just $100.

Financial Calculators and Online Tools

For quick checks, online compound interest calculators are invaluable. These tools often provide visual aids, such as graphs and charts, which illustrate the “bending of the curve”—the moment where interest earned per year begins to exceed the principal invested. These visualizations are powerful psychological motivators for consistent saving.

The Rule of 72: A Mental Shortcut

For investors who need to make quick decisions, the Rule of 72 is a reliable mental shortcut. To find out how long it will take for your money to double at a given interest rate, divide 72 by the annual rate of return. For example, at a 6% return, your money will double in approximately 12 years (72 / 6 = 12). This allows for rapid assessment of investment opportunities without needing a calculator.

Maximizing the “Snowball Effect” in Your Portfolio

Understanding the math is the first step; applying it to build a robust financial future is the second. There are specific levers you can pull to maximize the efficiency of compound interest.

The Advantage of Early Entry

The most critical variable in the compound interest formula is t (time). Because the growth is exponential, the final years of an investment see the most dramatic gains. This is why financial advisors emphasize starting early. An individual who invests $200 a month starting at age 25 will often end up with significantly more wealth than someone who starts investing $500 a month at age 45, simply because the 25-year-old gave the “snowball” more time to roll.

The Impact of Consistency and Contributions

While the basic formula assumes a lump sum, most real-world wealth building involves “periodic additions.” Regularly adding to your principal—known as Dollar Cost Averaging—compounds the compounding effect. By consistently buying into the market or adding to a savings account, you ensure that the “P” (principal) in your formula is constantly growing, leading to an even steeper growth curve.

Minimizing “Wealth Leakage”

Taxation and fees are the enemies of compound interest. When your earnings are taxed every year (as in a standard brokerage account), you have less money left to compound. This is why tax-advantaged accounts like IRAs and 401(k)s are so effective; they allow the full amount of your earnings to remain in the account, compounding in its entirety until retirement. Similarly, keeping investment fees low ensures that more of your return stays in your pocket.

Real-World Applications: From Debt to Retirement

Compound interest is a double-edged sword. While it is a miracle for savers, it can be a disaster for debtors. Applying these calculations to different areas of your financial life is crucial for holistic wealth management.

Managing High-Interest Debt

Credit cards are a prime example of compound interest working against the consumer. Most credit cards compound interest daily. This means if you carry a balance, you are paying interest on the interest accrued just 24 hours prior. By understanding the math, consumers can see why paying only the “minimum balance” leads to a debt trap that can take decades to escape.

Retirement Planning and the Rule of 4%

For retirement, compound interest dictates how much you can safely withdraw. Once you have used the compound interest formula to project your nest egg, you can apply the “4% Rule,” which suggests you can withdraw 4% of your total portfolio in the first year of retirement (adjusted for inflation thereafter) with a high probability of the money lasting 30 years. This transition from “accumulation” to “distribution” is the ultimate goal of mastering interest calculations.

Inflation: The Counter-Force

When figuring out your future wealth, you must account for inflation. While your bank account may show a 5% growth, if inflation is at 3%, your “real” rate of return is only 2%. Professional investors always calculate “real compound interest” to ensure their purchasing power is actually increasing over time, rather than just the nominal dollar amount.

By mastering the calculation and application of compound interest, you transition from a spectator in your financial life to an architect of your future. Whether you are paying down debt or building a multi-million dollar portfolio, the principles remain the same: start early, understand the variables, and let the math do the heavy lifting.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.