Determining exactly how much of your paycheck should be diverted into savings is one of the most critical decisions in personal finance. While many people approach saving as an afterthought—putting aside whatever happens to be left at the end of the month—financial success is rarely achieved through leftovers. It requires a proactive, calculated strategy. Using a “how much to save per month calculator” is the first step in transforming a vague desire for wealth into a concrete mathematical roadmap.

In this guide, we will explore the mechanics of monthly savings, the strategic frameworks used by financial experts, and the specific variables that influence how your money grows over time. Whether you are saving for a house, building an emergency fund, or planning for a multi-decade retirement, understanding the “why” and “how” behind the numbers is essential for long-term security.

Understanding the Mechanics of a Monthly Savings Calculator

A savings calculator is more than just a digital tool; it is a bridge between your current reality and your future aspirations. To use one effectively, you must understand the inputs that drive the results. Most calculators require four primary data points: your current balance, your goal amount, your time horizon, and your expected rate of return.

Input Variables: Goals, Timeframes, and Interest

The precision of your savings plan depends entirely on the accuracy of your inputs. Your starting balance represents your baseline. If you are starting from zero, the burden on your monthly contributions will be higher. Your savings goal should be specific. Rather than saying “I want to be rich,” a calculator requires a figure like “$50,000 for a down payment” or “$2 million for retirement.”

The timeframe is perhaps the most influential variable. Time acts as a multiplier. Saving for a goal ten years away is fundamentally different from saving for one three years away, as the former allows for the power of compounding to do the heavy lifting. Finally, the expected rate of return (or interest rate) dictates how much of your final balance will come from your pocket versus how much will come from market growth or bank interest.

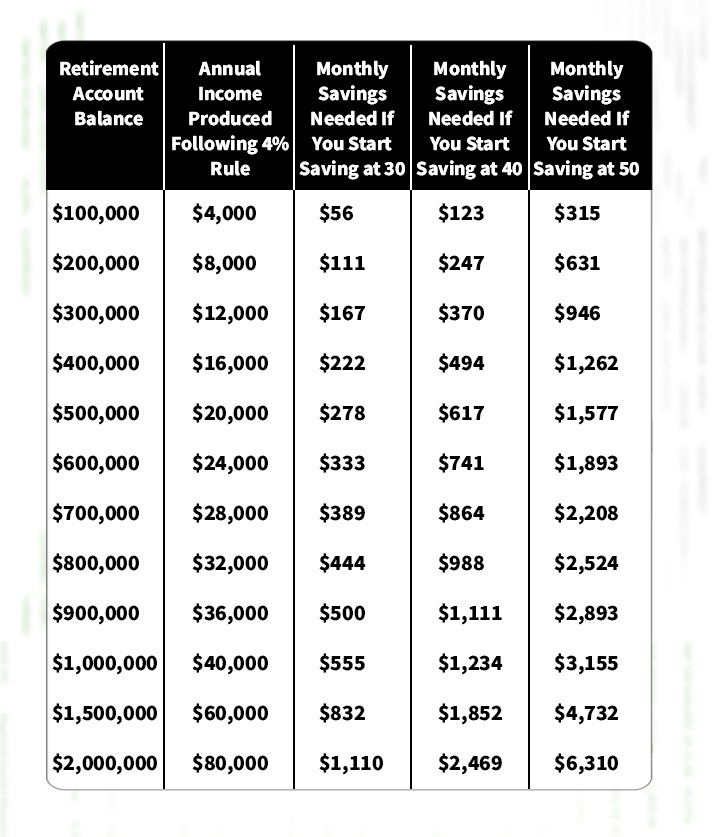

The Role of Compound Interest in Long-Term Projections

Compound interest is often cited as the “eighth wonder of the world” because it allows your interest to earn interest. When you use a savings calculator, you will notice that the longer your money stays invested, the less you actually need to contribute out of pocket to reach your goal.

For example, if you wish to save $100,000 over 20 years at a 7% annual return, a calculator will show that you need to save significantly less per month than if you tried to reach that same goal in 10 years. This is because, in the 20-year scenario, time allows the growth to snowball. Understanding this mechanic encourages early saving habits, as every dollar saved in your 20s is mathematically more powerful than a dollar saved in your 40s.

Core Strategies to Determine Your Monthly Savings Target

While a calculator tells you what is mathematically necessary, your budget tells you what is realistically possible. Balancing these two requires a structural approach to your income. There are several frameworks that financial professionals recommend to help individuals find their “sweet spot” for monthly savings.

The 50/30/20 Rule: A Balanced Approach

The 50/30/20 rule is a popular and straightforward budgeting framework that suggests allocating 50% of your after-tax income to “needs” (rent, groceries, utilities), 30% to “wants” (dining out, hobbies, travel), and 20% to savings and debt repayment.

Using this as a baseline, if you earn $5,000 a month after taxes, your calculator should ideally be set to a $1,000 monthly contribution. This rule is effective because it ensures that you are paying your “future self” before you spend on discretionary lifestyle choices. However, for those with aggressive goals—such as early retirement—this 20% figure often serves as a floor rather than a ceiling.

Backwards Engineering from Major Life Goals

Another effective strategy is to work backward from a specific deadline. If you know you want to buy a home in five years and need a $60,000 down payment, your “how much to save per month calculator” becomes your primary directive.

In this scenario, the math is uncompromising. If the calculator says you need to save $900 a month to reach that $60,000 goal, and your current budget only allows for $500, you are faced with a strategic choice: extend the timeline, increase your income through a side hustle, or reduce your “wants” spending. This “goals-based” saving method provides much higher clarity than saving a random percentage of your income.

Maximizing Your Savings Efficiency through Smart Allocation

Knowing how much to save is only half the battle; knowing where to put that money is what determines the interest rate you plug into your calculator. Not all savings vehicles are created equal, and your choice should depend on your goal’s timeline.

High-Yield Savings Accounts vs. Market Investing

For short-term goals (1–3 years), liquidity and safety are paramount. In this case, your calculator should use a conservative interest rate reflecting current High-Yield Savings Account (HYSA) or Money Market Account rates. These accounts protect your principal while offering a modest return that often keeps pace with inflation.

For long-term goals (5+ years), such as retirement or a child’s education fund, the “savings” should actually be “investing.” By utilizing a brokerage account or a tax-advantaged account like a 401(k) or IRA, you can input a higher rate of return (historically 7–10% for the S&P 500) into your calculator. This significantly reduces the monthly amount you need to contribute, though it comes with the trade-off of market volatility.

The Importance of an Emergency Fund Buffer

Before you start calculating for a new car or a luxury vacation, your calculator should be used to establish an emergency fund. Most experts recommend saving 3 to 6 months of essential living expenses. This fund acts as a financial shock absorber, ensuring that if you lose your job or face a medical emergency, you don’t have to liquidate your long-term investments or go into debt. When running your monthly savings numbers, the emergency fund should always be the priority “Step 1” before any other goals are factored in.

Overcoming Common Financial Hurdles to Hit Your Target

Life is rarely a straight line, and even the most well-calculated savings plan will face obstacles. Understanding how to navigate debt and economic shifts is vital to maintaining your savings momentum.

Managing Debt while Saving

One of the most debated topics in personal finance is whether to save or pay off debt. If you have high-interest debt, such as credit card balances at 20% APR, it mathematically outweighs any interest you could earn in a savings account. In this case, your “monthly savings” should technically be directed toward debt elimination.

However, for low-interest debt like a mortgage or some student loans, it often makes more sense to continue saving and investing while making the minimum payments. A savings calculator can help you compare the opportunity cost of these two paths, showing you the long-term wealth difference between aggressive debt repayment and consistent investing.

Adjusting for Inflation and Lifestyle Creep

A common mistake when using a savings calculator is forgetting that $1,000 today will not buy the same amount of goods in 20 years. Inflation erodes purchasing power. Therefore, when calculating long-term goals, it is wise to use a “real” rate of return (the nominal interest rate minus the inflation rate) to ensure your future nest egg is as large as you need it to be in “today’s dollars.”

Furthermore, as your career progresses and your income increases, you may fall victim to “lifestyle creep”—the tendency to increase your spending as your earnings rise. To stay on track with your calculated goals, it is beneficial to practice “reverse lifestyle creep” by automatically increasing your monthly savings contribution every time you receive a raise.

Conclusion: Taking the First Step Toward Financial Freedom

The journey to financial security begins with a single calculation. While the prospect of saving large sums of money can feel overwhelming, breaking a massive goal down into a monthly contribution makes it manageable and actionable. A “how much to save per month calculator” is a tool for empowerment; it removes the guesswork and replaces it with a clear, objective target.

By identifying your goals, choosing an appropriate strategy like the 50/30/20 rule, and understanding where to allocate your funds for maximum growth, you can take control of your financial destiny. Remember that the most important factor in any savings plan is not the starting amount, but the consistency of the contribution. Start today, adjust as your life changes, and let the math work in your favor.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.