In the world of finance, numbers are the language of progress. Whether you are tracking the growth of a retirement account, evaluating the success of a side hustle, or analyzing the quarterly revenue of a Fortune 500 company, one metric stands above almost all others in its utility: the percent increase.

Understanding how to find a percent increase is more than just a mathematical exercise; it is a fundamental skill for financial literacy. It allows an investor to strip away the “noise” of raw dollar amounts to see the underlying rate of growth. A $10,000 gain is impressive if you started with $20,000, but it is marginal if you started with $1,000,000. By mastering the calculation of percent increase, you gain the ability to compare different financial instruments, assess risk, and set realistic goals for your economic future.

The Fundamental Formula for Financial Fluency

Before diving into complex market analysis, one must master the basic arithmetic that governs all growth metrics. The percent increase represents how much a value has grown relative to its starting point, expressed as a fraction of 100.

The Basic Calculation: New vs. Old

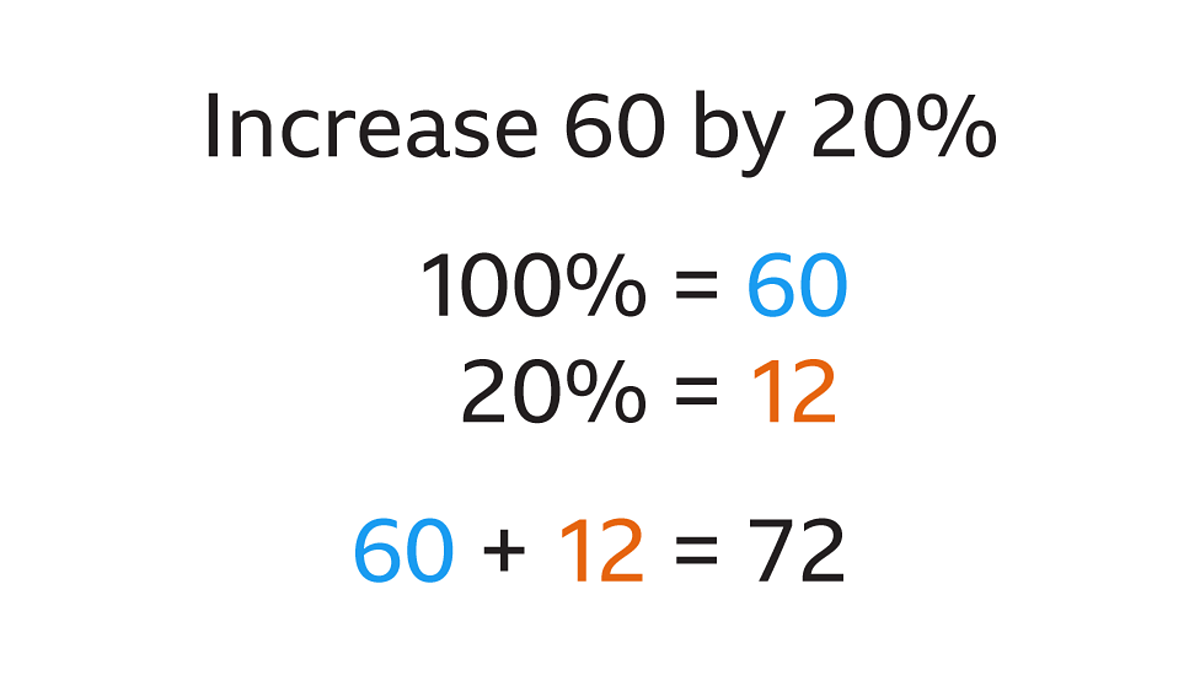

To find the percent increase, you follow a simple three-step process. First, subtract the original value (the “old” number) from the new value. This gives you the absolute increase. Second, divide that absolute increase by the original value. Finally, multiply the resulting decimal by 100 to convert it into a percentage.

The formula looks like this:

((New Value – Original Value) / Original Value) × 100 = Percent Increase

For example, if you invested $5,000 in a brokerage account and it grew to $6,500 over the course of a year, your calculation would be:

- $6,500 – $5,000 = $1,500 (The absolute gain)

- $1,500 / $5,000 = 0.3

- 0.3 × 100 = 30%

This 30% figure tells you exactly how hard your money worked for you, regardless of the initial sum.

Why Decimals and Percentages Matter in Wealth Building

In personal finance, we often deal with decimals before they become percentages. Understanding that a 0.05 increase is a 5% gain is critical when reading bank statements or loan documents. When you are looking at credit card interest rates or high-yield savings account APYs, these small numbers dictate the velocity of your wealth.

If your savings account offers a 4% annual increase, and inflation is running at 3%, your “real” percent increase is only 1%. Being able to flip between raw numbers and percentages allows you to see the true value of your purchasing power over time.

Measuring Investment Performance and Portfolio Growth

For the modern investor, the percent increase is the primary yardstick for success. It levels the playing field, allowing you to compare a high-priced stock like Berkshire Hathaway with a low-priced penny stock or an Index Fund.

Calculating Capital Gains and ROI

Return on Investment (ROI) is perhaps the most common application of the percent increase formula in the financial world. When you sell an asset—be it real estate, stocks, or cryptocurrency—for more than you paid for it, you have realized a capital gain.

However, looking at the raw profit doesn’t tell the whole story. If Investor A makes $50,000 on a house sale and Investor B makes $50,000 on a stock sale, who performed better? If Investor A bought the house for $500,000 (a 10% increase) and Investor B bought the stocks for $100,000 (a 50% increase), Investor B used their capital five times more efficiently. Calculating the percent increase allows you to identify which assets are truly driving your net worth upward.

Understanding Compounded Annual Growth Rate (CAGR)

While a simple percent increase measures growth between two points in time, serious investors often look at the Compounded Annual Growth Rate (CAGR). This is a more sophisticated version of percent increase that accounts for the effects of compounding over multiple years.

Compounding is often called the “eighth wonder of the world” in finance. If your portfolio sees a 10% increase every year, you aren’t just gaining 10% on your original investment; you are gaining 10% on the new, larger total every year. By understanding how to calculate these annual increases, you can project how long it will take to double your money (the “Rule of 72”) and plan your retirement timeline with greater precision.

Business Metrics: Tracking Revenue and Profitability

For business owners and corporate analysts, calculating percent increase is a daily necessity. It is the primary tool used to report growth to stakeholders and to measure the health of a company’s operations.

Year-over-Year (YoY) Analysis

In business finance, seasonal fluctuations can make monthly data misleading. A retail business might see a 200% increase in sales in December compared to November, but that doesn’t necessarily mean the business is growing; it just means it is the holiday season.

To solve this, professionals use Year-over-Year (YoY) percent increase. This involves comparing the current month’s revenue to the same month in the previous year. If December 2023 revenue was $100,000 and December 2024 revenue is $120,000, the business has seen a 20% YoY increase. This is a much more accurate reflection of the company’s trajectory and market share expansion.

Gauging Margin Expansion

Profitability isn’t just about increasing revenue; it’s about managing costs. Business finance experts use percent increase to track “margin expansion.” If a company’s revenue increases by 10% but its expenses increase by 15%, the company is actually becoming less efficient despite making more money.

By calculating the percent increase in “Gross Margin” or “Net Income,” executives can determine if their growth is sustainable. A healthy business seeks a percent increase in profit that meets or exceeds the percent increase in revenue, indicating that the company is scaling efficiently.

The Impact of Inflation and Purchasing Power

In personal finance, not all increases are positive. One of the most critical uses of the percent increase formula is monitoring the rising cost of living, commonly known as inflation.

Real vs. Nominal Returns

When you hear that the stock market returned 10% last year, that is a “nominal” increase. To understand your “real” increase, you must subtract the percent increase of the Consumer Price Index (CPI), which measures inflation.

If your investments grew by 8% (percent increase in portfolio value) but the cost of milk, gas, and rent grew by 9% (percent increase in CPI), your purchasing power actually decreased by 1%. This is a sobering reality for many savers. Understanding how to find the percent increase of your expenses is just as vital as finding the increase in your income. If your annual salary raise is 3%, but the percent increase in your local cost of living is 5%, you have effectively received a pay cut.

Adjusting Your Budget for Rising Costs

A robust financial plan requires constant adjustment. By calculating the percent increase in your recurring bills—such as insurance premiums, utility costs, and groceries—you can identify “budget creep.” If your grocery bill has seen a 15% increase over six months, it may be time to audit your spending or find new suppliers. Using percentages allows you to see which categories of your budget are accelerating the fastest, helping you decide where to cut back to maintain your savings rate.

Strategic Decision Making Using Percent Increase

Ultimately, the ability to calculate percent increase transforms you from a passive observer of your finances into an active strategist. It provides the clarity needed to make difficult choices between competing financial opportunities.

Comparing Opportunity Costs

Every dollar you invest in one place is a dollar you cannot invest elsewhere. This is known as opportunity cost. Suppose you are choosing between paying down a high-interest debt at 7% or investing in a mutual fund that you expect will have a 5% annual increase.

By comparing these two percentages, the choice becomes mathematically clear: paying off the debt provides a “guaranteed” 7% return on your money by eliminating an expense, which is superior to the projected 5% gain from the investment. Percent increase (and decrease) provides the common denominator needed to compare apples to oranges in the financial world.

Setting Financial Benchmarks

Finally, percent increase is the key to effective benchmarking. Most investors compare their personal performance against a benchmark like the S&P 500. If the S&P 500 had a 12% increase this year and your personal portfolio only had a 6% increase, you are underperforming the market.

This data is an invitation to investigate why. Are you paying too much in management fees? Are you over-diversified in low-growth assets? Without the ability to calculate and compare percent increases, you would be flying blind, unable to determine if your financial strategy is actually working or if you are simply benefiting from a rising tide that is lifting all boats.

In conclusion, the percent increase is the heartbeat of financial analysis. From the simple task of calculating a pay raise to the complex world of corporate YoY revenue tracking and real inflation-adjusted returns, this one formula provides the insight necessary to build and sustain wealth. By mastering this calculation, you empower yourself to make data-driven decisions that will define your financial legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.