In the modern financial landscape, the ability to accept credit card payments is no longer a luxury—it is a fundamental requirement for business viability. Whether you are a small business owner, a freelancer, or a growing corporate entity, the mechanisms by which you collect revenue directly impact your cash flow, accounting accuracy, and overall financial health. For a business, moving away from cash-only operations toward a digital-first payment strategy opens the door to a global customer base and streamlines the reconciliation process.

However, navigating the world of merchant services, interchange fees, and financial compliance can be daunting. This guide explores the essential components of credit card processing from a business finance perspective, helping you choose the right tools to optimize your revenue collection.

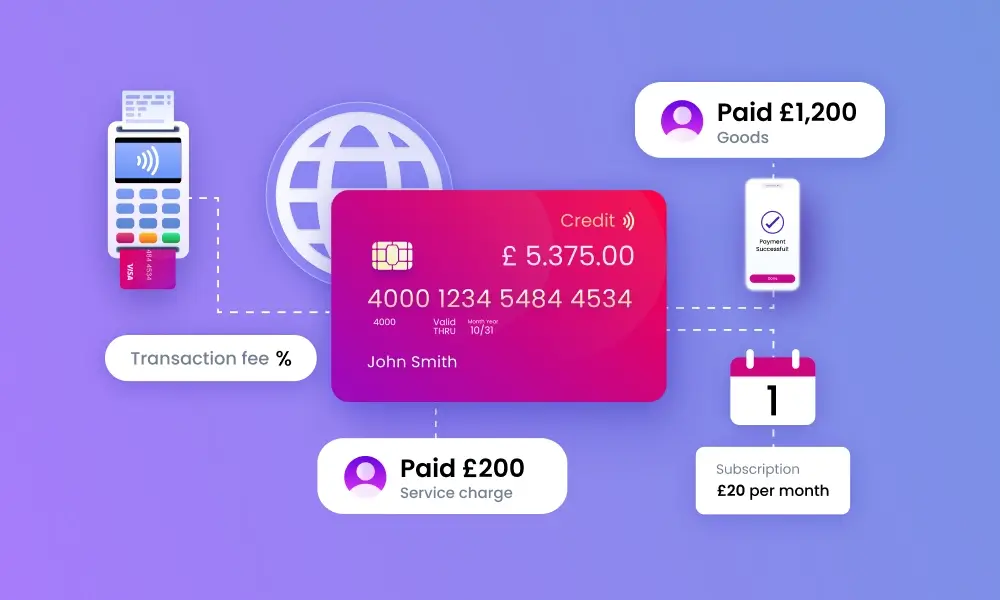

Understanding the Merchant Ecosystem and Financial Infrastructure

Before a business can swipe its first card or process its first online transaction, it must understand the underlying financial infrastructure. Receiving a credit card payment is not a direct transfer from the customer’s bank to yours; it involves a complex relay between several financial institutions.

Merchant Accounts vs. Payment Aggregators

The first decision any business must make is how they wish to hold their funds. A Merchant Account is a dedicated business bank account that allows you to accept credit and debit card payments. These accounts are traditional and offer high levels of stability and customized pricing, but they often require a rigorous application process.

On the other hand, Payment Aggregators (such as Square, PayPal, or Stripe) allow businesses to process payments under a single “master” merchant account. This is the fastest route to receiving payments, as it requires minimal setup. For startups and small-scale entrepreneurs, aggregators provide a low barrier to entry, though they may offer less control over fund holding and higher flat-rate fees compared to dedicated merchant accounts.

The Role of Payment Gateways in Modern Finance

If your business operates online, the payment gateway is your digital storefront’s cash register. It is the software layer that encrypts sensitive credit card information and communicates with the processor to authorize the transaction. From a financial management standpoint, the gateway is critical because it handles the initial validation of funds. Choosing a gateway that integrates seamlessly with your financial software ensures that your sales data flows directly into your ledgers, reducing manual entry errors and providing real-time visibility into your earnings.

Evaluating the Cost of Processing: Fees and Financial Management

In business finance, the “cost of goods sold” is a standard metric, but many owners overlook the “cost of receiving money.” Every credit card transaction carries a fee, and understanding the breakdown of these costs is vital for maintaining healthy profit margins.

Interchange Fees and Assessment Charges

The bulk of your processing costs comes from Interchange Fees. These are non-negotiable fees set by card networks (like Visa and Mastercard) and paid to the card-issuing bank. These fees vary based on the type of card used (rewards cards and corporate cards usually have higher fees) and the level of risk associated with the transaction.

In addition to interchange fees, you will encounter Assessment Charges, which are paid directly to the card networks for the use of their infrastructure. As a business owner, you cannot change these rates, but understanding them allows you to price your products and services more effectively to absorb these necessary financial overheads.

Flat-Rate vs. Tiered Pricing Models

Processors usually offer one of three pricing structures:

- Flat-Rate Pricing: You pay a fixed percentage for every transaction (e.g., 2.9% + $0.30). This is predictable and excellent for small businesses with lower volumes.

- Interchange-Plus Pricing: This is the most transparent model for larger businesses. You pay the exact interchange fee plus a small fixed markup to the processor. This allows you to see exactly where every penny of your transaction fee is going.

- Tiered Pricing: Transactions are categorized as “qualified,” “mid-qualified,” or “non-qualified.” While it may look cheaper on paper, this model is often the most expensive because many transactions are downgraded to higher-priced tiers, making financial forecasting difficult.

Selecting the Right Tools for Your Business Model

The method you use to receive payments should align with your specific business model. Financial tools are not one-size-fits-all, and the wrong choice can lead to unnecessary expenses or technical bottlenecks.

Solutions for E-commerce and Online Sales

For digital businesses, the focus is on reducing “cart abandonment” while maintaining high security. Online payment processors offer “hosted payment pages” where the customer is redirected to a secure site to pay, or “integrated APIs” that allow the customer to stay on your website throughout the transaction. From a finance perspective, integrated solutions often provide better data analytics, allowing you to track customer spending habits and optimize your marketing spend based on actual revenue data.

Point of Sale (POS) Systems for Physical Retail

Brick-and-mortar businesses require hardware. Modern POS systems have evolved from simple cash registers into comprehensive financial hubs. These systems do more than just swipe cards; they manage inventory, track employee hours, and generate daily financial reports. Investing in a high-quality POS system allows a business to synchronize its physical sales with its digital records, ensuring that the balance sheet is always up to date.

Mobile Payments and Invoicing Tools

For service-based businesses, such as consultants or contractors, the ability to receive payments on the go is paramount. Mobile card readers that plug into a smartphone or tablet have revolutionized field-service finance. Furthermore, professional invoicing tools allow you to send a digital bill with a “Pay Now” button embedded. This reduces the “Days Sales Outstanding” (DSO)—a key financial metric—by making it easier for clients to settle their accounts immediately upon receipt of the invoice.

Risk Management and Financial Security

Receiving credit card payments introduces financial risks that must be managed. Security is not just a technical requirement; it is a financial safeguard against fraud and loss.

PCI Compliance and Data Integrity

The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that all companies that process, store, or transmit credit card information maintain a secure environment. Failure to maintain PCI compliance can result in heavy fines from banks and the loss of the ability to process cards entirely. Financially, it is much cheaper to invest in a PCI-compliant processor than to deal with the fallout of a data breach, which can include legal fees, customer reimbursements, and long-term brand damage.

Mitigating Chargebacks and Fraudulent Activity

A “chargeback” occurs when a customer disputes a transaction with their bank, leading to a reversal of the payment. For a business, a chargeback is a double hit: you lose the revenue from the sale, and you are usually hit with a chargeback fee ranging from $15 to $100.

To protect your business finance, you must implement fraud detection tools like Address Verification Systems (AVS) and Card Verification Value (CVV) checks. Maintaining clear communication with customers and having a transparent refund policy are the best financial defenses against legitimate disputes, ensuring that your earned revenue stays in your account.

Optimizing Cash Flow through Payment Integration

The final step in mastering credit card payments is ensuring that the money moves efficiently from the processing terminal to your business bank account.

Settlement Periods and Funding Cycles

When a customer pays by credit card, the money is not immediately available. It typically goes through a “settlement” process that takes 24 to 72 hours. Understanding your processor’s funding cycle is essential for managing daily operations, paying vendors, and meeting payroll. Some modern financial tools offer “Instant Deposit” for an extra fee, which can be a vital lifeline for businesses facing temporary liquidity challenges.

Integrating Payments with Accounting Software

The peak of financial efficiency is achieved when your payment processor is integrated with your accounting software (such as QuickBooks, Xero, or FreshBooks). In a manual system, a bookkeeper must export transaction logs and manually reconcile them against bank deposits—a process prone to human error. With integration, every credit card payment received is automatically logged, categorized, and reconciled. This real-time accounting provides business owners with an accurate snapshot of their financial position at any given moment, enabling data-driven decisions that foster long-term growth and stability.

By strategically choosing your merchant infrastructure, understanding the nuances of fees, and prioritizing security and integration, you transform the act of “receiving payment” from a simple transaction into a powerful engine for business financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.