In the modern financial landscape, few tickers command as much attention, awe, and scrutiny as NVDA. As the primary beneficiary of the generative AI revolution, Nvidia Corporation has seen its market capitalization soar into the trillions, leaving investors and analysts grappling with a fundamental question: How much is Nvidia stock selling for relative to its earnings, and is that premium justified? While the casual observer might misinterpret the financial jargon—perhaps even confusing “earnings” with “earrings”—the reality of Nvidia’s valuation is a complex study in growth projections, market dominance, and the mechanics of the Price-to-Earnings (P/E) ratio.

To understand Nvidia’s current market position, one must look beyond the raw stock price and delve into the relationship between its market value and its actual profitability. This “Money” focused analysis explores the metrics that define Nvidia’s valuation, the factors driving its premium, and the risks inherent in such a high-octane financial profile.

Understanding the P/E Ratio: Why Nvidia Trades at a Massive Premium

The most common metric used to determine if a stock is “expensive” or “cheap” is the Price-to-Earnings (P/E) ratio. This figure represents the dollar amount an investor can expect to invest in a company in order to receive one dollar of that company’s earnings. When investors ask how much Nvidia is selling “over” its earnings, they are essentially asking about this multiple.

The Forward P/E vs. Trailing P/E Distinction

When analyzing Nvidia, it is crucial to distinguish between the Trailing P/E and the Forward P/E. The trailing P/E looks at the last 12 months of actual earnings. Because Nvidia’s growth has been so explosive, its trailing P/E often looks astronomical—sometimes exceeding 70x or 100x. However, the market is a forward-looking mechanism.

The Forward P/E, which uses estimated earnings for the next 12 months, often tells a different story. Because Nvidia’s earnings have been doubling or tripling year-over-year, its forward P/E frequently drops into a more “reasonable” range, often sitting between 30x and 45x. For a company growing at Nvidia’s pace, a forward P/E in the 30s can actually be viewed as undervalued by growth-oriented investors, despite being significantly higher than the S&P 500 average.

Historical Context of Nvidia’s Valuation

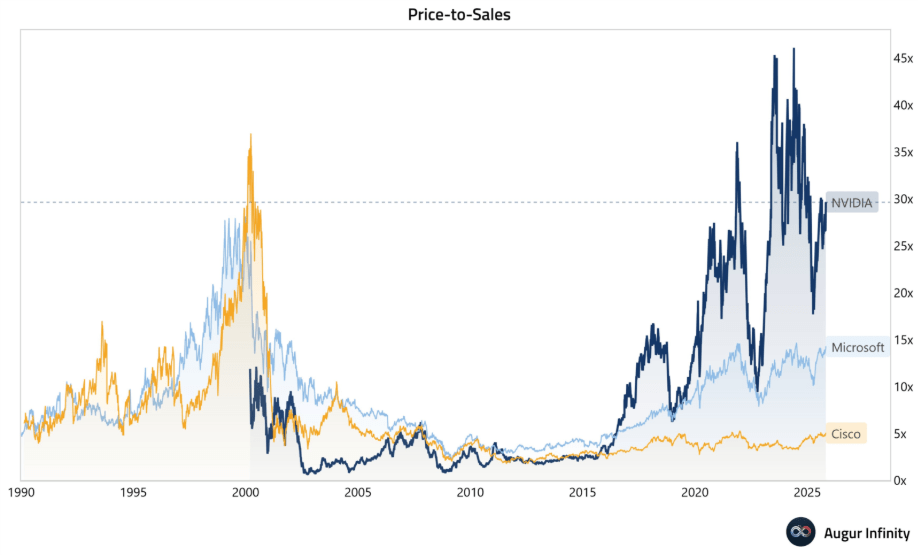

Nvidia has not always been a trillion-dollar titan. Historically, the company traded as a cyclical semiconductor stock, heavily dependent on the gaming industry and, later, crypto-mining. During those eras, its valuation fluctuated wildly based on GPU inventory levels. Today, the shift from “gaming” to “data center” as the primary revenue driver has fundamentally re-rated the stock. Investors are no longer paying for a hardware manufacturer; they are paying for the infrastructure provider of the fourth industrial revolution. This structural shift explains why the stock consistently sells at a premium that would have seemed unthinkable a decade ago.

The AI Multiplier: How Generative AI Justifies Higher Earnings Multiples

The reason Nvidia sells at such a high multiple over its current earnings is the anticipated explosion in future cash flows. In financial terms, this is often referred to as “multiple expansion” driven by a total addressable market (TAM) that appears almost limitless.

Data Center Revenue as the Growth Engine

The “Money” story of Nvidia is centered on its Data Center segment. Unlike the consumer market, where a gamer might buy one GPU every three to five years, cloud service providers (CSPs) like Microsoft, Google, and Amazon are purchasing tens of thousands of H100 and B200 Blackwell chips simultaneously.

This massive institutional demand provides Nvidia with incredible pricing power. When a company has gross margins exceeding 70%, every dollar of revenue contributes significantly to the bottom line. This high-margin profile allows the stock to sustain a higher P/E ratio because the quality of its earnings—the actual cash remaining after expenses—is superior to most other hardware firms.

Software and Ecosystem Lock-in (CUDA)

Investors are not just paying for silicon; they are paying for the “moat” created by CUDA (Compute Unified Device Architecture). CUDA is Nvidia’s proprietary software platform that allows developers to use GPUs for general-purpose processing. Because the entire AI development ecosystem is built on CUDA, switching to a competitor’s chip (like AMD or Intel) involves massive software migration costs. In the eyes of a financial analyst, this “stickiness” reduces the risk of future earnings volatility, justifying a higher price-to-earnings premium.

Comparative Analysis: Nvidia vs. the Mag 7 and Semiconductor Peers

To determine if Nvidia is truly overvalued, we must compare its “price over earnings” against its peers in the “Magnificent Seven” and the broader semiconductor industry. Valuation is never absolute; it is always relative.

Benchmarking Against AMD and Intel

In the semiconductor space, Nvidia’s valuation often looks high compared to Intel, but Intel is currently struggling with a turnaround and lower growth. A more apt comparison is AMD. Interestingly, there have been periods where AMD’s P/E ratio was actually higher than Nvidia’s, despite Nvidia having higher margins and a larger market share. This suggests that while Nvidia’s stock price is high, it is backed by more robust “earned” income than its closest competitors. Nvidia earns more, so even though its price is higher, the ratio remains competitive.

Nvidia in the Context of the “Magnificent Seven”

When compared to the rest of the Magnificent Seven (Apple, Microsoft, Alphabet, Amazon, Meta, Tesla), Nvidia often displays the highest growth rate. While Apple might trade at a P/E of 28x with single-digit revenue growth, Nvidia trading at 35x or 40x forward earnings with triple-digit growth represents a much better “Growth at a Reasonable Price” (GARP) play for many institutional fund managers. This relative value is why the stock continues to attract capital even at record highs.

Risks and Sustainability: Can the Earnings Keep Pace with the Stock Price?

No investment is without risk, and the primary danger for Nvidia investors is “multiple compression.” This occurs when the market decides that a company’s high-growth phase is ending, leading to a lower P/E ratio even if earnings remain stable.

The Cyclical Nature of the Semiconductor Industry

Historically, the chip industry is boom-and-bust. There is a risk that the current AI spending spree is a “front-loading” event, where companies buy all the chips they need now, leading to a massive drop in orders two years down the line. If Nvidia’s earnings growth slows from 100% to 10%, a P/E of 40x will no longer be sustainable. The stock price would likely see a significant correction to align with its new, slower growth reality.

Geopolitical Pressures and Regulatory Risks

A significant portion of Nvidia’s earnings comes from international markets, including China. U.S. export restrictions on high-end AI chips have already forced Nvidia to create “throttled” versions of its hardware for the Chinese market. Should these regulations tighten further, or should geopolitical tensions in Taiwan (where Nvidia’s chips are manufactured by TSMC) escalate, the projected earnings used to justify the current stock price could vanish overnight. Investors paying a premium today are taking on this concentrated geopolitical risk.

Investment Strategy: Navigating Nvidia’s “Expensive” Price Tag

For the individual investor, the question isn’t just “how much is it selling for,” but “is it a good buy today?” This requires looking at metrics that combine price, earnings, and growth.

The PEG Ratio: Factoring in Growth

The PEG ratio (Price/Earnings to Growth) is perhaps the most vital tool for evaluating Nvidia. A PEG ratio of 1.0 is generally considered “fair value.” Despite its high stock price, Nvidia’s PEG ratio has often dipped below 1.0 during its fastest growth spurts. This presents a financial paradox: a stock can be at an all-time high price and have a high P/E ratio, yet still be “cheap” relative to its growth rate. For many, this is the green light that justifies holding the stock despite the headline-grabbing price.

Long-term Horizon vs. Short-term Volatility

Because Nvidia sells so far “over” its current earnings based on future expectations, it is subject to extreme volatility. A single earnings report that “only” meets expectations instead of “smashing” them can lead to a 10% drop in share price. However, for investors with a five-to-ten-year horizon, these fluctuations are often noise. The central thesis remains: if AI is the future of the global economy, the company providing the “shovels” for the “gold mine” will continue to command a premium.

In conclusion, Nvidia stock sells at a significant premium over its trailing earnings, but when adjusted for its unprecedented growth and market dominance, that premium appears more calculated than speculative. While the “price” is high, the “earnings” engine behind it is currently one of the most powerful in corporate history. As with any high-growth investment, the key for the “Money”-minded investor is to balance the excitement of the AI revolution with the cold, hard reality of valuation multiples and risk management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.