In the complex landscape of personal and business finance, various instruments exist to facilitate the flow of capital between parties. While most people are familiar with credit cards and standard bank mortgages, there is a fundamental legal document that underpins many of these transactions: the promissory note. Often shortened to a “promissory” in casual financial dialogue, this document serves as a powerful bridge between a simple verbal agreement and a formal, complex loan contract. Understanding what a promissory note is, how it functions, and why it remains a cornerstone of the financial world is essential for anyone looking to manage debt, raise capital, or lend money effectively.

Understanding the Fundamentals of a Promissory Note

At its core, a promissory note is a written, unconditional promise made by one party (the issuer or maker) to pay a specific sum of money to another party (the payee) either on demand or at a specified future date. It is a legal instrument that outlines the terms of a debt, providing clarity and security for both the borrower and the lender.

Definition and Key Components

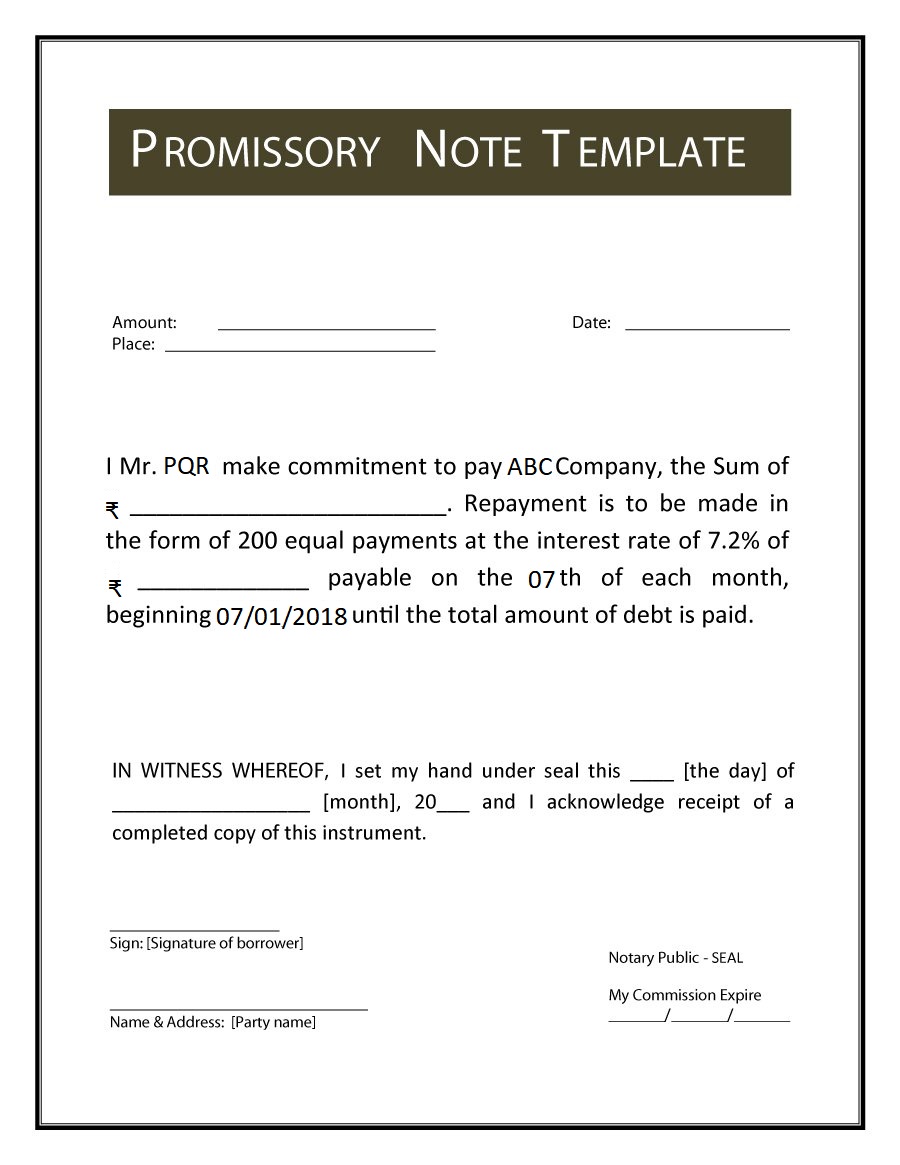

A promissory note is more than just a piece of paper stating that money is owed. To be legally binding and effective in a financial context, it typically must include several specific elements. These include the names of the parties involved, the total amount of money borrowed (the principal), the interest rate being charged, the repayment schedule (including the maturity date), and the signatures of the involved parties. Because it is a contract, it carries the weight of the law, allowing a lender to seek legal recourse if the borrower fails to uphold their end of the agreement.

How It Differs from a Simple IOU

While many people use the terms “IOU” and “promissory note” interchangeably, they are distinct in the eyes of financial law. An IOU (an abbreviation for “I owe you”) is merely an acknowledgment of a debt. It proves that a debt exists but often lacks the specific details regarding repayment dates, interest, or the consequences of default. In contrast, a promissory note is an enforceable promise to pay that includes the “how” and “when” of the transaction. In many jurisdictions, a promissory note can also be a “negotiable instrument,” meaning it can be sold or transferred to another party, whereas a simple IOU generally cannot.

The Legal Status of Promissory Notes

In the United States, promissory notes are often governed by the Uniform Commercial Code (UCC), specifically Article 3, which deals with negotiable instruments. This legal framework ensures that notes are handled consistently across state lines. Because these documents are legally binding, they provide a level of protection that verbal “handshake” deals lack. If a borrower defaults on a promissory note, the lender can use the document as primary evidence in a court of law to secure a judgment for the unpaid balance.

Common Types of Promissory Notes in Finance

The flexibility of the promissory note allows it to be used in various financial scenarios, from small personal loans to multi-million dollar corporate debt offerings. Depending on the nature of the transaction, the note may take several different forms.

Personal and Informal Promissory Notes

Personal promissory notes are frequently used for loans between family members or friends. In these scenarios, the borrower may not have access to traditional banking services, or the lender may wish to provide more favorable terms than a bank would. Even in informal settings, using a promissory note is a “money-smart” move. It prevents misunderstandings by clearly documenting whether the money is a gift or a loan, what the interest rate is, and when the lender expects to be paid back.

Commercial and Business Notes

In the business world, promissory notes are a standard tool for short-term financing. Companies often use them to manage cash flow or to purchase inventory. For instance, a business might issue a note to a supplier to defer payment for goods received. These commercial notes are typically more formal than personal ones and may include “covenants”—specific conditions that the business must meet to remain in good standing, such as maintaining a certain level of liquidity.

Real Estate and Mortgage Notes

When you buy a home, you typically sign two major documents: a mortgage (or deed of trust) and a promissory note. While the mortgage creates a lien on the property as collateral, the promissory note is the actual document where you promise to repay the loan. These notes are often “secured,” meaning that if the borrower defaults, the lender has the right to seize the property to recoup their losses. Because real estate notes involve large sums and long timeframes, they are highly detailed regarding amortization schedules and escrow requirements.

Investment and Convertible Notes

In the world of startups and venture capital, “convertible promissory notes” are incredibly popular. These are a hybrid of debt and equity. A startup might borrow money from an investor via a promissory note with the agreement that, at a later date (usually during a formal funding round), the debt will “convert” into shares of ownership in the company. This allows early-stage companies to get the funding they need without having to immediately determine the exact valuation of the business.

The Essential Elements of a Valid Note

For a promissory note to be an effective financial tool, it must be drafted with precision. Missing details can lead to disputes or make the note unenforceable in a court of law.

Principal Amount and Interest Rates

The principal is the original amount of money borrowed. The interest rate is the cost of borrowing that money, expressed as a percentage. In professional finance, it is crucial to specify whether the interest is “simple interest” (calculated only on the principal) or “compound interest” (calculated on the principal plus accumulated interest). Furthermore, the note should specify if the rate is fixed or variable.

Repayment Terms and Maturity Dates

The “how” and “now” of repayment are vital. A note can be structured in several ways:

- Installment Payments: The borrower pays a set amount monthly or quarterly.

- Interest-Only Payments: The borrower pays only the interest for a duration, with a “balloon payment” of the full principal due at the end.

- On-Demand: The lender can ask for the full amount at any time, provided they give reasonable notice.

- Lump Sum: The entire principal and interest are paid in one go on a specific maturity date.

Security and Collateral

Promissory notes can be either secured or unsecured. An unsecured note is backed only by the “full faith and credit” of the borrower; if they go bankrupt, the lender may get nothing. A secured note is backed by an asset, such as a car, equipment, or real estate. In the event of a default, the lender can take possession of that asset. In the world of high-finance and personal investing, secured notes are always preferred as they significantly lower the risk for the lender.

Risks and Benefits for Borrowers and Lenders

Like any financial instrument, the promissory note carries a specific profile of risks and rewards. Both parties must weigh these carefully before signing.

Why Lenders Use Them: Security and Income

For a lender, a promissory note is a way to generate passive income through interest. In a low-interest-rate environment, private lending via promissory notes can often yield higher returns than traditional savings accounts or government bonds. Additionally, the note provides a clear legal path to collection, which is far superior to an undocumented loan.

Why Borrowers Use Them: Flexibility and Access

Borrowers often turn to promissory notes because they offer flexibility that institutional banks cannot match. A borrower can negotiate unique repayment terms, such as a grace period or a lower interest rate, directly with the lender. For small business owners or individuals with less-than-perfect credit, a promissory note might be the only way to access the capital needed for a project or an emergency.

Potential Pitfalls: Default and Collection

The primary risk for any lender is “default”—the borrower’s failure to pay. Collecting on a defaulted note can be time-consuming and expensive, potentially requiring a lawyer or a collection agency. For the borrower, the risk lies in the legal consequences of default, which can include a damaged credit score, the loss of collateral, and legal judgments that can lead to wage garnishment.

The Role of Promissory Notes in Modern Business Finance

Despite the rise of digital banking and fintech, the promissory note remains as relevant as ever. It has evolved to meet the needs of the 21st-century economy, playing a pivotal role in how businesses scale and how investors seek yield.

Bridging the Gap in Startup Funding

As mentioned earlier, the convertible note is a staple of Silicon Valley. It allows founders to bridge the “funding gap” between their initial “friends and family” round and a major Series A. This financial tool simplifies the process, allowing founders to focus on growth rather than complex legal valuations during the most fragile stages of a company’s life.

Secondary Markets and Selling Debt

One of the most interesting aspects of promissory notes in the “Money” niche is their liquidity. Because they are often negotiable instruments, a lender who needs immediate cash doesn’t have to wait for the borrower to pay them back. They can sell the note to a third party (often at a discount). This creates a secondary market where investors buy and sell debt, much like they buy and sell stocks or bonds. This “selling of paper” is a common practice in the mortgage and auto-loan industries.

Digital Evolution: E-Notes

The financial world is increasingly moving toward “e-notes”—electronic promissory notes. These are digitally signed and stored in secure registries. While the format has changed from parchment to pixels, the underlying financial logic remains the same: a clear, enforceable promise that facilitates trust and commerce.

In conclusion, the promissory note is an indispensable tool in the world of money. Whether it is used to formalize a loan to a sibling, secure a mortgage for a first home, or provide seed capital for the next great tech giant, its ability to clearly define debt and repayment is unmatched. By understanding the components, types, and risks associated with these documents, individuals and business owners can navigate the world of finance with greater confidence and legal security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.