In the complex ecosystem of global economics, few numbers carry as much weight for the average consumer and business owner as the prime interest rate. Often referred to simply as “the prime,” this figure serves as the foundational benchmark for a vast array of lending products across the United States and beyond. Whether you are looking to purchase a home, carry a balance on a credit card, or secure a small business loan, the prime interest rate dictates the cost of your capital.

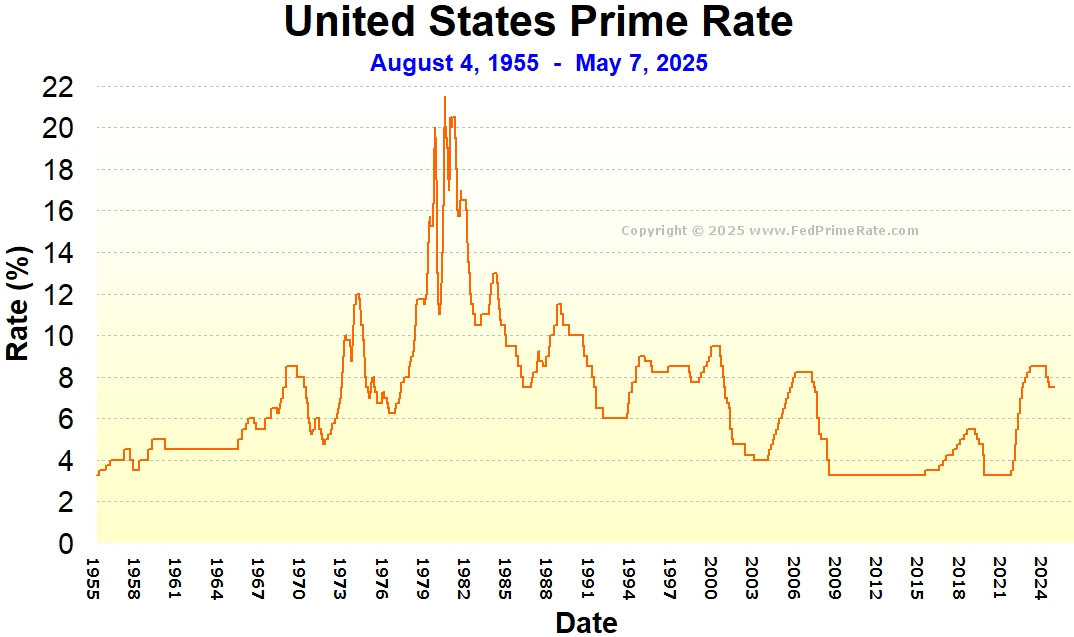

As of early 2024, the prime interest rate stands at 8.50%. This figure has remained steady following a period of aggressive hikes by the Federal Reserve aimed at curbing record-high inflation. To understand what this number means for your wallet, one must look beneath the surface at how the rate is determined, how it flows through the banking system, and what strategies you can employ to navigate a high-rate environment.

Understanding the Mechanics of the Prime Interest Rate

The prime interest rate is not set by a government agency, yet it is inextricably linked to federal policy. It is defined as the interest rate that commercial banks charge their most creditworthy corporate customers—those with the lowest risk of default. While each bank can technically set its own prime rate, the industry follows a consensus typically published by the Wall Street Journal, which polls the largest banks in the country.

The Definition and Origin of the Prime Rate

Historically, the prime rate was a private negotiation tool between banks and major industrial firms. Over the decades, it evolved into a standardized index. Today, the prime rate is almost universally calculated as the Federal Funds Target Rate plus 3.00%. For example, if the Federal Reserve sets the target range for the federal funds rate at 5.25% to 5.50%, the prime rate will be 8.50% (5.50% + 3.00%). This 3% spread allows banks to cover administrative costs and generate a profit margin while providing a reliable benchmark for variable-interest products.

The Relationship Between the Federal Reserve and Commercial Banks

The Federal Open Market Committee (FOMC) meets eight times a year to determine the federal funds rate—the rate at which banks lend to one another overnight. When the FOMC raises this rate to “cool” an overheating economy, commercial banks immediately raise the prime rate to maintain their margins. Conversely, when the economy slows and the Fed cuts rates to stimulate spending, the prime rate drops. This mechanism is the primary lever of monetary policy, influencing how much money circulates in the economy.

How the Prime Rate Influences Your Personal Debt

For the individual consumer, the prime rate is the “silent partner” in almost every financial contract. Most people do not borrow at the prime rate—instead, they borrow at “prime plus” a certain percentage based on their credit score.

Credit Cards and Variable APRs

The most immediate impact of a change in the prime rate is felt in credit card statements. The vast majority of credit cards have variable Annual Percentage Rates (APRs) tied directly to the prime rate. If you have a credit card with an APR of “Prime + 15%,” and the prime rate is 8.50%, your interest rate is 23.50%. When the prime rate moves, your credit card issuer typically adjusts your rate within one to two billing cycles. In a high-prime-rate environment, carrying a balance becomes exponentially more expensive, making debt reduction a top priority for household financial health.

Home Equity Lines of Credit (HELOCs)

Unlike most primary mortgages, which are fixed-rate loans tied to the 10-year Treasury yield, Home Equity Lines of Credit (HELOCs) are almost always tied to the prime rate. Because HELOCs are revolving lines of credit, the monthly interest payment can fluctuate significantly. For homeowners who used HELOCs for renovations or debt consolidation when the prime rate was 3.25% in 2020, the jump to 8.50% has more than doubled their interest expenses, often adding hundreds of dollars to monthly obligations.

Auto Loans and Personal Financing

While some auto loans offer fixed rates, many personal loans and private student loans use the prime rate as their index. Even for fixed-rate products, lenders look at the current prime rate to set the “floor” for new loans. When the prime rate is high, the cost of financing a new vehicle or taking out a personal loan for a wedding or medical expense rises, often forcing consumers to delay large purchases or opt for less expensive alternatives.

The Role of the Prime Rate in Business and Corporate Finance

The prime rate is often called the “heartbeat of business finance.” For small to medium-sized enterprises (SMEs), the cost of borrowing is the difference between expansion and stagnation.

Fueling Small Business Growth

Small Business Administration (SBA) loans are frequently tied to the prime rate. Many SBA 7(a) loans, the most common type of small business loan, have a maximum interest rate allowed that is expressed as “Prime + a markup” (usually 2.25% to 2.75%). When the prime rate sits at 8.50%, a small business might be paying upwards of 11% for capital. This increases the “hurdle rate”—the minimum return a project must generate to be profitable—making it harder for entrepreneurs to justify hiring new staff or purchasing new equipment.

Short-term Working Capital and Benchmarks

Larger corporations use the prime rate as a benchmark for short-term working capital lines of credit. These lines are essential for managing seasonal inventory shifts or bridging the gap between accounts receivable and accounts payable. If the prime rate remains elevated for an extended period, the cost of “doing business” rises across the board. These costs are often passed down to consumers in the form of higher prices for goods and services, contributing to the very inflation the Federal Reserve is trying to fight.

Economic Indicators and the Future of Interest Rates

The question of “what is the prime rate today” is often followed by “where is it going tomorrow?” To forecast the prime rate, one must look at the same indicators the Federal Reserve monitors.

Inflation and the Fed’s Balancing Act

The primary driver of interest rate policy is the Consumer Price Index (CPI). The Federal Reserve has a dual mandate: to promote maximum employment and maintain stable prices (targeting 2% inflation). When inflation rose to 9% in 2022, the Fed was forced to raise rates aggressively, pushing the prime rate from historical lows to its current decade-high level. As inflation begins to cool toward the 2% target, the pressure to maintain high rates diminishes. However, if the labor market remains too strong, the Fed may keep rates “higher for longer” to ensure inflation does not rebound.

Forecasting the Next Move

Market analysts and economists use the “FedWatch” tool to track the probability of future rate moves. If the Fed decides to cut the federal funds rate by 25 basis points (0.25%), the prime rate will almost certainly drop to 8.25% immediately following the announcement. Investors watch these signals closely, as a falling prime rate usually signals a “risk-on” environment where stocks and real estate become more attractive due to lower borrowing costs.

Strategies for Managing Your Finances in a High-Rate Environment

While an 8.50% prime rate presents challenges, it also offers opportunities for those who are proactive with their financial planning.

Debt Consolidation and Refinancing

In a high-rate environment, the “debt avalanche” method becomes even more effective. This involves paying off the debt with the highest interest rate first (usually credit cards tied to the prime rate). Consumers may also look into “0% APR” balance transfer cards. Although these cards are harder to qualify for when rates are high, they can provide a 12-to-21-month window to pay off principal without the burden of the 8.50% prime-based interest.

Maximizing Savings Yields

There is a silver lining to a high prime rate: savers finally win. High-yield savings accounts (HYSAs) and Certificates of Deposit (CDs) typically offer higher returns when the prime rate is elevated. Banks must compete for deposits to fund their lending activities, leading to interest rates on savings accounts that can exceed 4% or 5%. For the first time in over a decade, keeping cash in a liquid, FDIC-insured account can provide a meaningful return that keeps pace with or exceeds inflation.

Reevaluating Investment Portfolios

For investors, a high prime rate changes the “discount rate” used to value future earnings. Growth stocks, which rely on future profits, often struggle when rates are high because the cost of borrowing to fund that growth is expensive. Conversely, value stocks and sectors like insurance or banking may perform better. Financial literacy in this area involves understanding that the prime rate is not just a cost, but a signal for how to allocate assets for the long term.

In conclusion, the prime interest rate today is more than just a static number; it is a reflection of the current economic climate and a predictor of future financial trends. By understanding how it affects everything from your credit card bill to the national economy, you can make informed decisions that protect your capital and grow your wealth, regardless of which way the Federal Reserve moves next.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.