Interest rates are often described as the “price of money.” In the modern economic landscape, few metrics carry as much weight or influence over the daily lives of individuals and the strategic decisions of corporations. When the question “what is the current interest rate?” is asked, the answer is rarely a single number. Instead, it is a complex web of benchmarks, yields, and annual percentage rates (APRs) that dictate the cost of borrowing and the reward for saving.

In recent years, we have transitioned from an era of historic lows to a period of significant tightening by central banks globally. This shift has fundamentally altered the math behind personal finance, real estate, and investment strategies. Understanding the current interest rate environment is no longer just for economists; it is a vital skill for anyone looking to build and protect their wealth.

Understanding the Landscape of Current Interest Rates

To understand current rates, one must first look at the source: the central bank. In the United States, the Federal Reserve (the Fed) sets the Federal Funds Rate, which acts as the North Star for all other interest rates in the economy.

The Role of Central Banks and the Federal Funds Rate

The Federal Funds Rate is the interest rate at which commercial banks lend to each other overnight. While the average consumer never pays this rate directly, it influences everything from the prime rate to the yield on a 10-year Treasury note. When the Fed raises rates, it is typically an effort to cool down an overheating economy and curb inflation. By making it more expensive to borrow, the central bank reduces the amount of circulating currency, theoretically slowing the rise of prices for goods and services.

Why Rates Fluctuate: The Battle Against Inflation

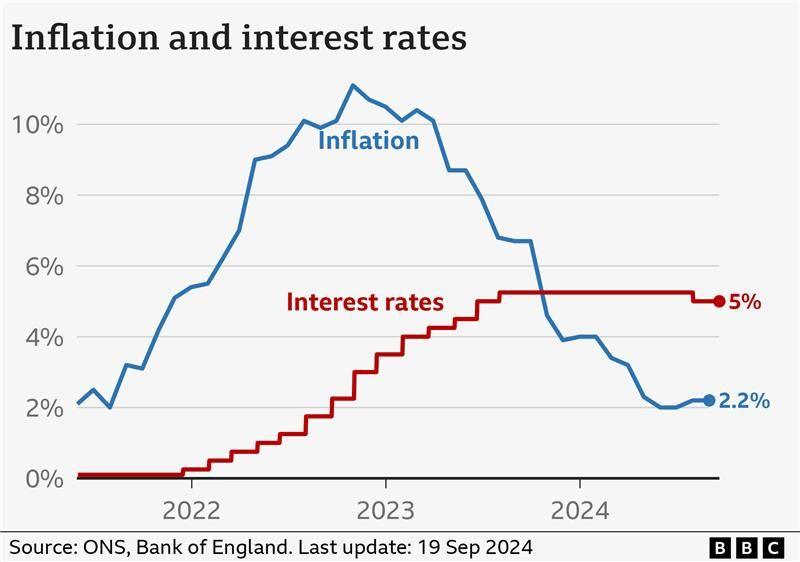

The primary driver of the recent upward trend in interest rates has been inflation. Following the global pandemic, a combination of supply chain disruptions, increased consumer demand, and fiscal stimulus led to a surge in the Consumer Price Index (CPI). Central banks responded by aggressively hiking rates to bring inflation back toward their traditional 2% target. Consequently, we have moved out of the “easy money” era into a “restrictive” environment, where the cost of capital is significantly higher than it was just a few years ago.

The Yield Curve and Economic Signaling

Investors also keep a close eye on the “yield curve,” which plots the interest rates of bonds with equal credit quality but differing maturity dates. In a healthy economy, long-term rates are higher than short-term rates. However, when short-term rates exceed long-term rates—a phenomenon known as an “inverted yield curve”—it often serves as a warning sign of a potential recession. Understanding these nuances helps investors anticipate where the market is headed before the headlines catch up.

The Impact on Personal Finance and Borrowing

The most immediate place where current interest rates hit home is the monthly budget. Whether you are buying a home, financing a car, or carrying a balance on a credit card, the current rate environment dictates your purchasing power.

Mortgages and the Housing Market

The 30-year fixed-rate mortgage is the benchmark for the American dream, and its movement has been dramatic. When interest rates rise from 3% to 7%, the monthly payment on the same loan amount can increase by hundreds or even thousands of dollars. This has led to a “lock-in effect,” where homeowners with low-interest mortgages are reluctant to sell, leading to decreased inventory and sustained high home prices. For buyers, the current rates require a more rigorous analysis of debt-to-income ratios and a greater emphasis on larger down payments to offset interest costs.

Credit Cards and Variable Interest Debt

Most credit cards carry variable interest rates tied to the prime rate. As the Fed increases its benchmark, credit card APRs follow suit almost immediately. With many cards now reaching APRs of 20% to 25% or higher, the cost of carrying a balance has become a significant financial drain. In this environment, the priority for any personal finance strategy must be the aggressive repayment of high-interest consumer debt, as the “guaranteed return” on paying off a 20% interest card far outweighs any realistic investment return in the stock market.

Auto Loans and Large Purchases

The days of 0% financing for vehicles are largely behind us. Current interest rates for auto loans have climbed, affecting both the new and used car markets. Consumers are now forced to consider longer loan terms to keep monthly payments manageable, though this often results in paying significantly more for the vehicle over the life of the loan. For those looking to make large purchases, the current environment suggests that “cash is king,” or at the very least, that shopping around for the best credit union rates is a mandatory step in the process.

Strategic Investing in a High-Rate Environment

While high interest rates are a burden for borrowers, they represent a golden opportunity for savers and certain types of investors. The investment playbook that worked during the 2010s—where “there is no alternative” (TINA) to stocks—has been rewritten.

The Resurgence of Fixed Income and Bonds

For the first time in over a decade, “risk-free” or low-risk investments are offering meaningful yields. US Treasury bonds, corporate bonds, and municipal bonds have become attractive components of a diversified portfolio. As rates rise, the yield on new bonds increases, providing a steady income stream that can compete with the volatility of the equity markets. For conservative investors or those nearing retirement, the current rate environment allows for a more traditional 60/40 (stocks/bonds) portfolio to function effectively once again.

The Stock Market’s Reaction to Rate Hikes

Generally speaking, rising interest rates are a headwind for stocks. Higher rates mean higher borrowing costs for companies, which can eat into profit margins. Furthermore, when calculating the “present value” of future earnings—a common way to value stocks—a higher interest rate (the discount rate) leads to a lower valuation today. This is particularly true for high-growth tech stocks that may not be profitable yet. However, certain sectors, such as banking and insurance, often benefit from higher rates as their net interest margins expand.

High-Yield Savings Accounts (HYSAs) and CDs

One of the few silver linings of the current interest rate hike is the return of the High-Yield Savings Account. For years, savings accounts paid a negligible 0.01%. Today, many online banks and credit unions offer 4% to 5% or more. Similarly, Certificates of Deposit (CDs) and “CD Ladders” have become popular tools for locking in high rates for the short-to-medium term. For an emergency fund or a down payment fund, these liquid, FDIC-insured options are currently providing excellent inflation-adjusted returns.

Business Finance and the Entrepreneurial Outlook

For business owners and corporate executives, the current interest rate environment represents a shift from a “growth-at-all-costs” mindset to one of “profitability and efficiency.”

The Cost of Capital and Expansion Plans

When money is cheap, businesses are more likely to take on debt to fund research and development, hiring, and physical expansion. At current rates, the “hurdle rate”—the minimum return a project must generate to be worth the investment—is much higher. Businesses are now being more selective with their capital expenditures, focusing on projects with clear, short-term ROI rather than speculative long-term bets.

Managing Cash Flow and Debt Service

Companies with significant variable-rate debt are feeling the squeeze on their cash flow. Managing the “debt service coverage ratio” has become a top priority for CFOs. Many businesses are looking to refinance existing debt into fixed-rate instruments or are utilizing interest rate swaps to hedge against future volatility. On the flip side, companies with large cash reserves are now generating significant interest income, adding a new layer of strength to their balance sheets.

Venture Capital and the Startup Ecosystem

The “startup” world has been hit particularly hard by the rise in rates. Venture capital (VC) firms, which rely on the promise of massive future returns, find it harder to justify risky investments when they can get a safe 5% return elsewhere. This has led to a “valuation reset” in the private markets, forcing startups to pivot toward sustainable business models and “burn rate” reduction earlier in their lifecycle.

Future Projections and Financial Planning

Interest rates are not static; they are a tool used to balance the economy. As we look forward, the question shifts from “what is the current interest rate?” to “where are rates going?”

When Will Rates Pivot?

Markets are constantly trying to predict the “pivot”—the moment when central banks stop raising rates and begin to lower them. This typically happens when inflation is under control or when the economy shows signs of a significant slowdown. While the timing is always uncertain, financial planning should account for a “higher-for-longer” scenario. Assuming that rates will quickly return to the zero-bound levels of the past decade may be a risky strategy.

Building a Resilient Portfolio for Any Environment

The key to navigating interest rate volatility is diversification and flexibility. A resilient financial plan includes:

- A mix of durations: Balancing short-term liquid assets (like HYSAs) with longer-term investments (like stocks and long-term bonds).

- Debt management: Prioritizing the elimination of variable-rate debt while holding onto low-interest, fixed-rate debt (like a 3% mortgage) for as long as possible.

- Regular rebalancing: Ensuring that as the value of different asset classes changes due to rate moves, your portfolio remains aligned with your risk tolerance.

In conclusion, while the current interest rate environment presents challenges—particularly for those looking to borrow—it also offers a renewed set of tools for the savvy saver and investor. By understanding the mechanisms behind these rates and adjusting your financial strategy accordingly, you can turn a period of economic transition into an opportunity for long-term wealth creation. Professional financial management in this era requires a keen eye on the central bank, a disciplined approach to debt, and the agility to move capital where it is most efficiently rewarded.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.