In the realm of finance, percentages are more than just mathematical symbols; they are the fundamental language of value, growth, and risk. Whether you are tracking the performance of a stock portfolio, determining the viability of a business venture, or simply trying to optimize your monthly budget, understanding how to calculate and interpret percentages is an essential skill. Financial literacy hinges on the ability to translate raw numbers into meaningful proportions. This guide explores the diverse applications of percentage calculations within the “Money” niche, providing you with the tools to navigate personal finance, investing, and corporate accounting with precision.

The Foundation: Understanding Percentages in Personal Finance

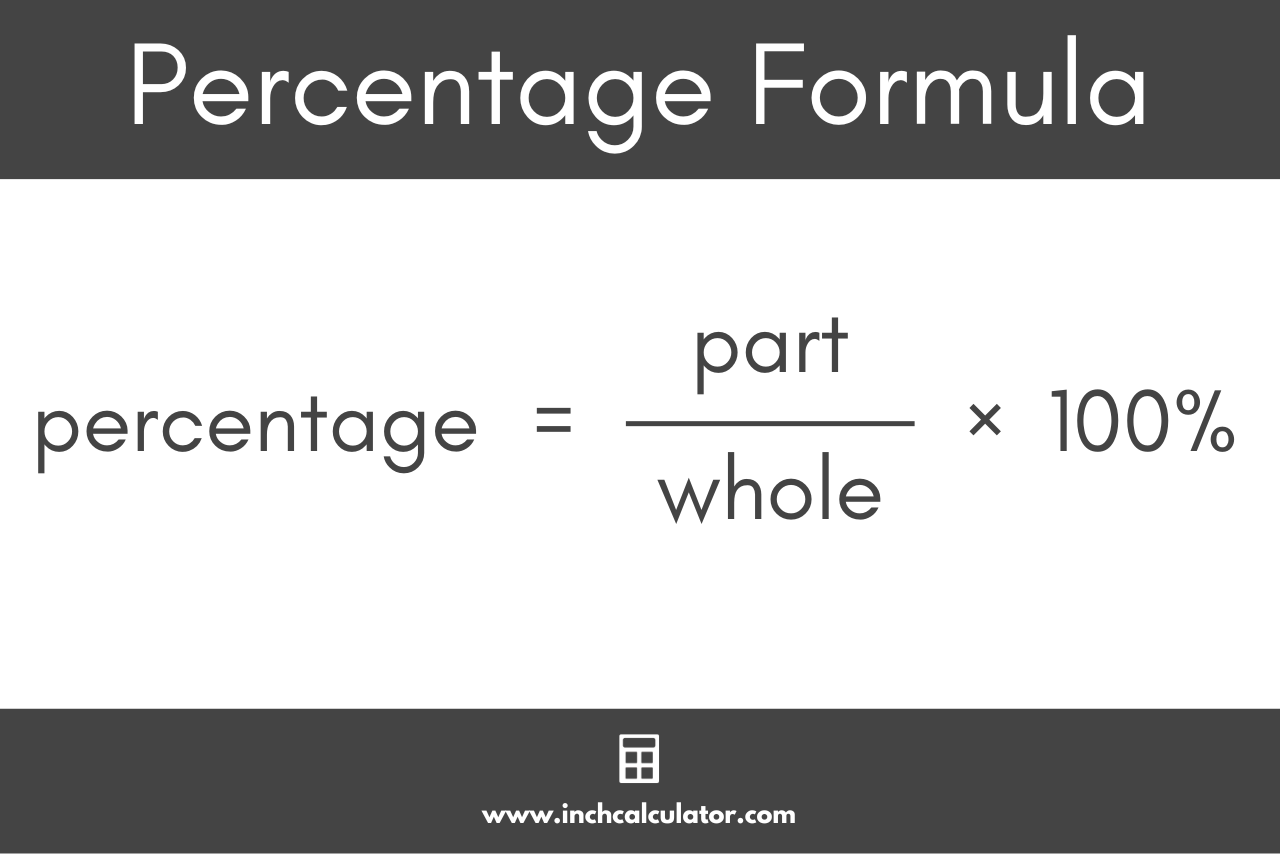

At its core, a percentage represents a fraction of 100. In personal finance, this allows for a standardized comparison between different sets of data, regardless of the currency or volume involved. Mastery of the basic percentage formula is the first step toward effective money management.

The Basic Formula Every Professional Should Know

The most fundamental calculation in finance is determining what portion one number represents of another. The formula is straightforward:

** (Part / Whole) × 100 = Percentage **

For example, if you earn $5,000 a month and your rent is $1,500, you are spending 30% of your income on housing ($1,500 / $5,000 = 0.3; 0.3 × 100 = 30%). In a professional context, this calculation is used to assess “expense ratios.” By converting your expenses into percentages, you can compare your spending habits against financial benchmarks, such as the 50/30/20 rule, which suggests allocating 50% of income to needs, 30% to wants, and 20% to savings.

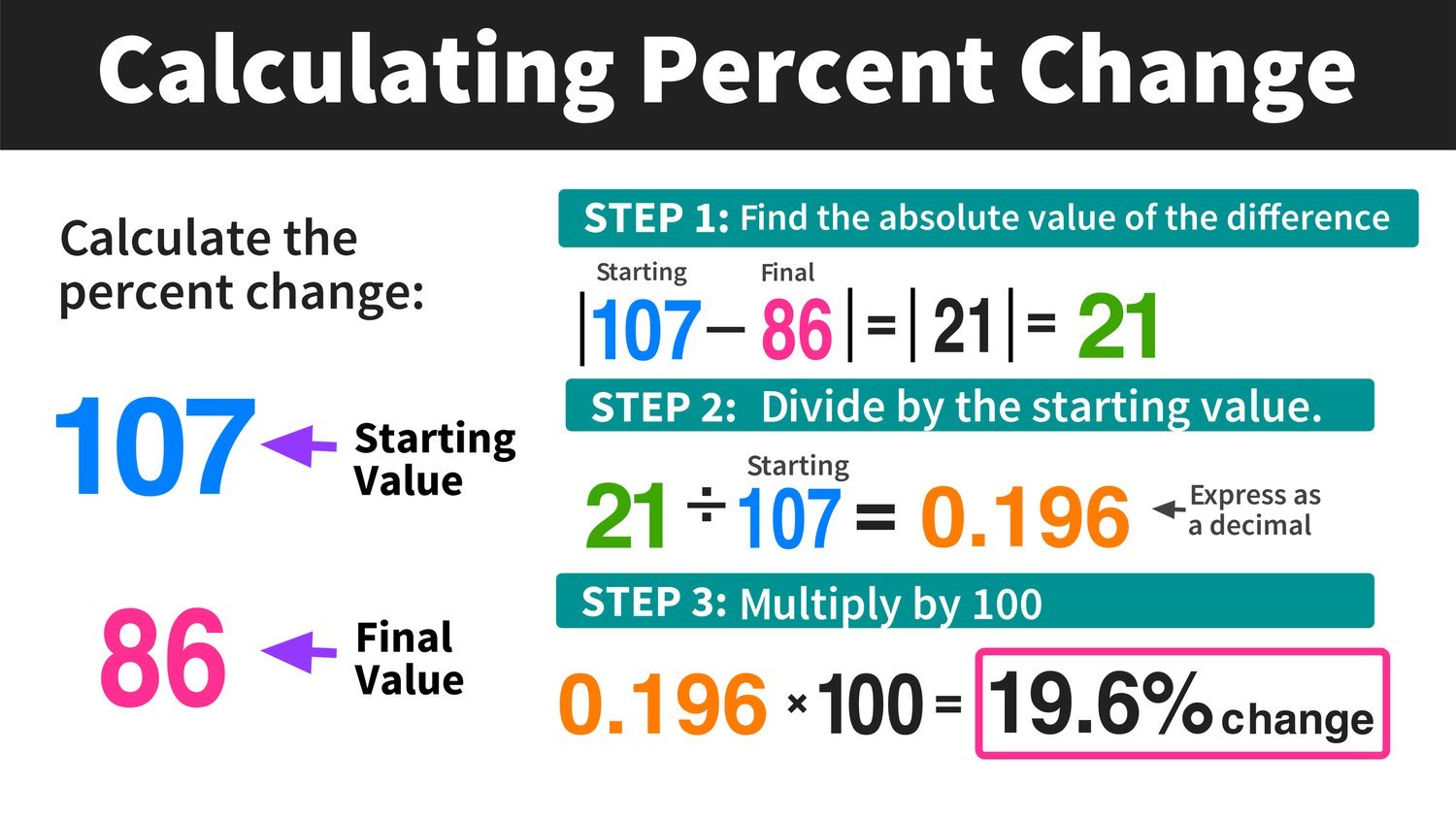

Calculating Percentage Increase and Decrease in Your Budget

Understanding growth or reduction is vital when tracking inflation or salary raises. To find the percentage change, use the following formula:

** [(New Value – Old Value) / Old Value] × 100 **

If your monthly grocery bill rose from $400 last year to $460 this year, the calculation would be: ($460 – $400) / $400 = 0.15. Multiplying by 100 reveals a 15% increase. For a professional looking to negotiate a salary, knowing that your cost of living has increased by a specific percentage provides a data-driven foundation for your request. Conversely, calculating percentage decreases helps identify the effectiveness of cost-cutting measures within a household or business budget.

Investing and ROI: Measuring the Growth of Your Portfolio

For investors, percentages are the primary metric for success. Nominal gains (the dollar amount) are often misleading without the context provided by percentage-based returns. Whether you are trading equities, real estate, or digital assets, the ability to calculate your yield determines your long-term strategy.

How to Calculate Return on Investment (ROI)

ROI is the ultimate barometer for any financial endeavor. It measures the efficiency of an investment or compares the efficiencies of several different investments. The formula is:

** [(Current Value of Investment – Cost of Investment) / Cost of Investment] × 100 **

Suppose you purchased shares in a tech company for $10,000, and two years later, the value of those shares is $13,500. Your ROI is 35%. However, a professional investor looks deeper. If you paid $500 in brokerage fees during that time, your “Cost of Investment” is actually $10,500. Recalculating with the fees included ($13,500 – $10,500) / $10,500 results in an ROI of approximately 28.5%. This nuanced approach to percentage calculation ensures that you are accounting for the “leakage” that often erodes net profits.

Compound Interest: The Power of Percentages Over Time

While simple interest is calculated only on the principal amount, compound interest is calculated on the principal plus the accumulated interest of previous periods. Understanding this percentage-based growth is crucial for retirement planning. The formula for compound interest is:

** A = P(1 + r/n)^(nt) **

Where:

- A = the future value of the investment

- P = the principal balance

- r = the annual interest rate (decimal)

- n = the number of times interest is compounded per year

- t = the number of years the money is invested

For a wealth builder, seeing how a 7% annual return compounds over 30 years versus a 4% return can be life-changing. A 3% difference in the “percentage” might seem small annually, but due to the nature of exponential growth, it can result in a difference of hundreds of thousands of dollars by the time of retirement.

Business Finance and Profitability Metrics

In the corporate world, percentage calculations are used to determine the health of a company. Revenue alone does not tell the full story; it is the margins—the percentages—that reveal if a business is truly sustainable.

Profit Margins: Gross vs. Net Percentage

A company’s “Gross Profit Margin” reflects the percentage of revenue that exceeds the cost of goods sold (COGS). It is calculated as:

** [(Total Revenue – COGS) / Total Revenue] × 100 **

If a business sells a product for $100 and it costs $60 to manufacture, the gross margin is 40%. However, the “Net Profit Margin” is even more critical, as it accounts for all expenses, including taxes, interest, and operating costs. A high gross margin but a low net margin suggests that while the product is profitable to make, the company’s overhead (rent, marketing, salaries) is too high. Professional financial analysts use these percentages to identify where a business is losing efficiency.

Markup vs. Margin: Avoiding Common Financial Errors

One of the most frequent errors in business finance is confusing markup with margin. Markup is the percentage added to the cost to reach the selling price, whereas margin is the percentage of the selling price that is profit.

- Markup: (Profit / Cost) × 100

- Margin: (Profit / Revenue) × 100

If an item costs $80 and you want a 25% markup, you sell it for $100. However, the profit margin on that $100 sale is only 20% ($20 profit / $100 revenue). If a business owner mistakes a 25% markup for a 25% margin, they may inadvertently price their products too low to cover their operational expenses, leading to a cash flow crisis.

Debt and Tax Management: The Cost of Capital

Percentages also represent the “cost” of money. When you borrow, you pay a percentage; when you earn, the government takes a percentage. Managing these figures is essential for maintaining a positive net worth.

Understanding Annual Percentage Rates (APR)

When taking out a mortgage, car loan, or credit card, the APR is the most important number. Unlike a simple interest rate, the APR includes the interest rate plus any other fees or costs involved in procuring the loan.

Calculating the impact of APR allows you to see the “real” cost of debt. For instance, on a $20,000 car loan, the difference between a 4% APR and a 7% APR over five years isn’t just 3%; it translates to thousands of dollars in extra interest payments. Professionals use percentage-based debt-to-income (DTI) ratios to determine their borrowing capacity. Most lenders prefer a DTI of 36% or less, meaning your total monthly debt payments should not exceed 36% of your gross monthly income.

Calculating Your Effective Tax Rate

Taxation is rarely a flat percentage. Most systems are progressive, meaning different portions of your income are taxed at different rates. To understand your true financial standing, you must calculate your “Effective Tax Rate” rather than just looking at your “Marginal Tax Bracket.”

The formula is:

** (Total Tax Paid / Total Taxable Income) × 100 **

If you are in a 24% tax bracket, you aren’t paying 24% on every dollar. Your first several thousand dollars are taxed at 10%, the next portion at 12%, and so on. By calculating the effective percentage, you gain a clearer picture of your actual take-home pay, which is the only figure that should be used for budgeting and investment planning.

Conclusion: The Strategic Value of Numerical Precision

Calculating percentages is not merely a mathematical exercise; it is a strategic necessity in the world of money. By mastering these formulas, you move from a passive observer of your finances to an active manager of your wealth. Percentages provide the clarity needed to compare disparate investment opportunities, the discipline required to maintain a healthy budget, and the insight necessary to scale a profitable business.

In every financial decision—from choosing a high-yield savings account to analyzing a corporate balance sheet—the percentage is the key that unlocks the true story behind the numbers. As you apply these calculations to your own financial life, you will find that the ability to think in percentages is one of the most valuable assets in your professional and personal toolkit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.