In an era of fluctuating inflation and rising living costs, the concept of “cash back” has evolved from a niche coupon-clipping hobby into a sophisticated pillar of personal finance management. While the digital landscape is flooded with online shopping rebates, many consumers overlook the significant opportunities to recoup funds during their physical, day-to-day transactions. Understanding where to get cash back near you is not merely about finding an ATM alternative; it is about architecting a financial strategy that treats every dollar spent as an opportunity for a micro-return on investment.

This guide explores the diverse ecosystem of local cash-back opportunities, ranging from traditional retail maneuvers to high-tech financial tools that bridge the gap between physical commerce and digital rewards.

1. Traditional Retail and Grocery Solutions

The most immediate answer to “where to get cash back near me” often lies within the brick-and-mortar retailers you visit weekly. These establishments provide two distinct forms of cash back: the ability to withdraw currency at the point of sale and the ability to earn rewards on purchases.

Supermarkets and Big-Box Stores

Major grocery chains like Kroger, Publix, and Safeway, along with big-box giants like Walmart and Target, remain the most reliable locations for “debit card cash back.” This practice allows a customer to add an amount to their total purchase and receive that amount in physical currency. From a financial perspective, this is a superior alternative to out-of-network ATMs, which often charge predatory fees. By securing $20 to $100 during a grocery run, you effectively eliminate the “convenience tax” associated with standalone cash machines.

Pharmacy and Drugstore Chains

National chains such as CVS and Walgreens offer similar point-of-sale cash-back options. However, the true value in these locations lies in their integrated loyalty programs. When you search for cash back at these locations, you should look beyond the physical bills and toward the “store currency” (like Walgreens Cash). When managed correctly, these rewards act as a liquid asset that offsets future liabilities (spending), effectively keeping more cash in your primary checking account.

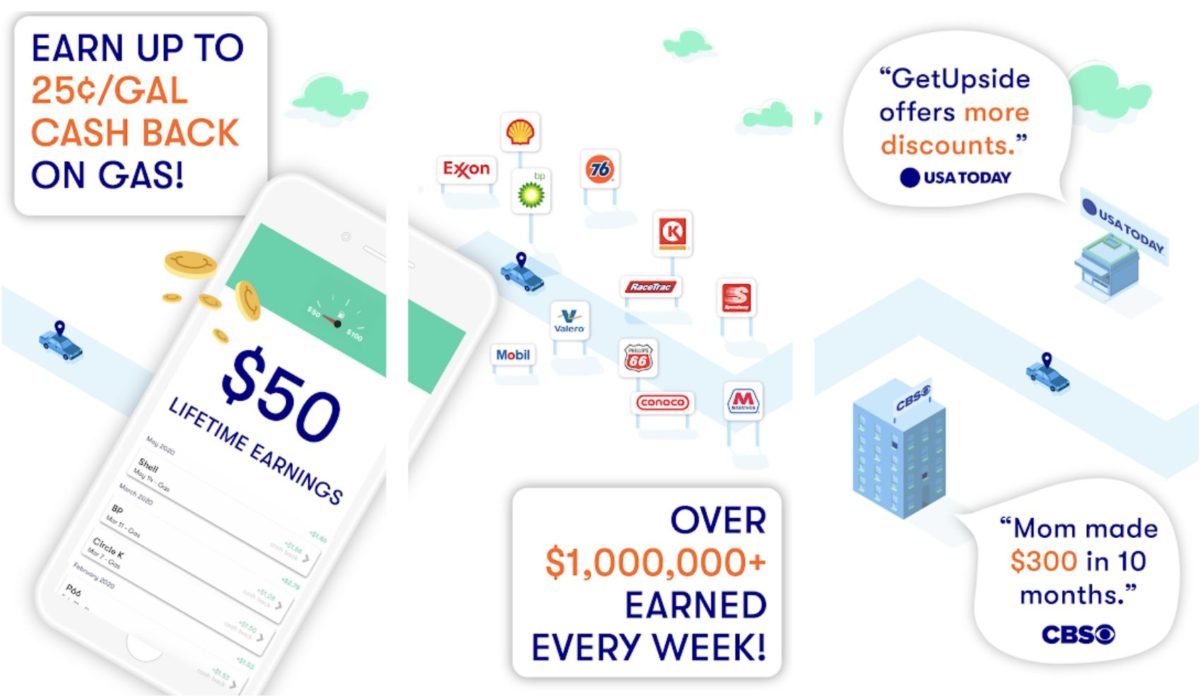

The Gas Station Hack

Gas stations are often overlooked as cash-back hubs. While many offer a lower price for cash payments, a growing number of fuel stations are partnering with financial apps to offer “per-gallon” cash back. Brands like BP, Shell, and ExxonMobil have proprietary apps that link to your payment method, providing an immediate rebate on every gallon. In a high-price fuel environment, this represents a significant percentage of “cash back” that stays in your pocket rather than going into the tank.

2. Leveraging Modern Financial Technology

The “Money” niche has been revolutionized by fintech apps that allow users to geolocate cash-back opportunities in real-time. These tools turn your smartphone into a financial radar, identifying which nearby businesses are currently offering the highest incentives.

Receipt Scanning and Verification Apps

Apps like Ibotta and Fetch Rewards have changed the “near me” search parameters. Instead of looking for a specific store that gives cash, you look for stores that carry specific products with high rebates. By scanning a receipt after a local shopping trip, you can earn cash back on everything from milk to electronics. The sophistication of these platforms allows for “stacking”—where you receive a store discount, use a cash-back credit card, and then scan the receipt for a third layer of savings.

Linked-Card Proximity Rewards

Modern financial tools like Dosh and Rakuten (formerly Ebates) have introduced “In-Store” cash-back features. By linking a credit or debit card to these platforms, the technology tracks your GPS location and alerts you to nearby participating merchants. When you swipe your card at a local restaurant or clothing boutique, the cash back is automatically credited to your account without the need for scanning receipts or showing coupons. This “passive” cash-back model is ideal for those who want to optimize their finances without adding friction to their daily routine.

Digital Wallets and Neo-Banking

Apple Pay, Google Pay, and neo-banks like Chime or Revolut often feature “boosts” or localized offers. By opening your banking app and looking at the “Explore” or “Rewards” tab, you can find map-based interfaces showing local coffee shops, hardware stores, or diners offering 5% to 10% cash back. These offers are often time-sensitive, making them a dynamic way to choose where to spend your money based on the highest current yield.

3. Strategic Maximization: Combining Methods for High Yield

Finding where to get cash back is the first step; the second is mastering the “stacking” methodology. Professional personal finance management involves layering multiple cash-back streams to reach an effective discount of 10% to 15% on standard retail prices.

The “Stacking” Strategy

To maximize local cash back, a consumer should use a high-yield cash-back credit card (e.g., 2% on all purchases) to pay for an item at a store found through a rebate app (e.g., 5% back on Ibotta). If that store also has a loyalty program, the consumer earns a third layer of points. This triple-threat approach transforms a mundane errand into a high-efficiency financial transaction. For instance, buying household essentials at a local pharmacy could yield credit card points, store rewards, and an app-based rebate simultaneously.

Understanding Merchant Category Codes (MCC)

Sophisticated earners pay attention to how a “near me” business is classified by credit card issuers. A gas station that sells groceries might be classified as “Fuel,” while a large supermarket with a pharmacy might be classified as “Grocery.” By aligning your spending with a credit card that offers 3% to 5% back on specific categories, you can strategically choose which local business to visit based on your card’s current high-earning bracket.

Seasonal and Quarterly Rotations

Many financial institutions rotate their high-yield categories every three months. One quarter might offer 5% back on “Local Small Businesses,” while another focuses on “Gas Stations and Wholesale Clubs.” Staying aware of these rotations allows you to shift your local shopping habits to whichever merchant category is currently providing the highest cash-back liquidity.

4. Hidden Cash Back Opportunities in the Local Economy

Beyond the obvious retail outlets, the local economy is full of “hidden” cash-back opportunities that require a slightly different approach to discover.

Local Dining and Professional Services

Many local restaurants participate in “Dining Rewards” programs linked to major airline or hotel loyalty schemes. By registering your primary spending card with these networks, you can earn cash-equivalent points at neighborhood eateries that don’t overtly advertise cash-back options. Similarly, some local service providers (like mechanics or dentists) offer discounts for “cash” payments—which, while not a traditional rebate, functions as an immediate cash-back incentive by reducing the principal expense.

Utility and Subscription Rebates

While not a physical location you visit, your local utility companies often partner with financial platforms to offer rebates on energy-efficient upgrades. Furthermore, using certain “Money” management apps can identify if you are overpaying for local services and negotiate “cash back” in the form of service credits or refunds for past overcharges.

Credit Union and Community Bank Perks

Small, local financial institutions often offer “Kasasa” accounts or similar reward-based checking products. These accounts often provide massive cash-back percentages (sometimes up to 3-5% on debit purchases) specifically to encourage local spending. Unlike national banks, these community-focused institutions often have “near me” perks that are exclusively available to residents of your specific zip code.

5. Security and Best Practices in the Financial Digital Age

While pursuing cash back is a productive financial habit, it must be balanced with digital security and a clear understanding of the “data-for-dollars” trade-off.

Data Privacy and App Permissions

Most cash-back apps require access to your location data and purchase history. From a personal finance perspective, you are essentially selling your consumer data in exchange for a rebate. It is vital to use reputable apps with transparent privacy policies. Ensure that the “cash back” you receive is worth the level of tracking you are permitting. Using a dedicated email address for these services can help maintain digital hygiene and prevent your primary inbox from being overwhelmed by marketing offers.

Avoiding the “Spending Trap”

A common pitfall in the pursuit of cash back is “induced spending.” The psychological allure of getting $5 back can often trick a consumer into spending $50 on an item they didn’t originally need. To maintain a healthy financial profile, cash-back tools should only be applied to planned, necessary expenditures. The goal is to get cash back on things you were already going to buy, not to use “savings” as a justification for lifestyle creep.

Managing Your Cash-Back Liquidity

Cash back sitting in an app is not the same as cash in your bank account. Many platforms have a minimum withdrawal threshold (e.g., $20). To optimize your “Money” strategy, you should treat these balances as accounts receivable. Once you hit the threshold, transfer the funds to a high-yield savings account or use them to pay down high-interest debt. Allowing cash back to sit idle in a third-party app is essentially giving that company an interest-free loan of your money.

Conclusion

Mastering the search for “where to get cash back near me” is a fundamental skill in modern wealth management. By combining the physical convenience of retail cash-back with the analytical power of fintech apps and strategic credit card usage, you can turn your local geography into a source of passive income. Whether it’s the $20 you save on fees at the grocery store or the 10% rebate you stack at a local diner, these small wins compound over time. In the world of personal finance, the most successful individuals aren’t just those who earn the most, but those who optimize every dollar they spend. By treating your local environment as a landscape of financial opportunity, you ensure that your money always works as hard for you as you did to earn it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.