When investors and financial analysts discuss the pinnacle of corporate success, one name invariably dominates the conversation: Apple Inc. (AAPL). As the first company in history to hit a $1 trillion, $2 trillion, and subsequently a $3 trillion market capitalization, Apple has become the ultimate barometer for the health of the global economy and the tech-heavy Nasdaq. But when we ask “how much is Apple worth,” the answer is a moving target—a complex calculation of share price, outstanding equity, cash reserves, and future earning potential.

To understand Apple’s valuation, one must look beyond the sleek gadgets and retail aesthetics. This is a study of unprecedented capital efficiency, massive share buybacks, and a transition from a hardware manufacturer to a high-margin services powerhouse.

Decoding Apple’s Market Capitalization and Shareholder Value

Market capitalization, or “market cap,” is the most common metric used to determine a company’s worth. It is calculated by multiplying the current share price by the total number of outstanding shares. For Apple, this figure frequently fluctuates between $2.5 trillion and $3.5 trillion, depending on quarterly earnings reports and broader macroeconomic trends such as interest rates and inflation.

What Does Market Cap Actually Mean?

Market capitalization represents the public’s consensus on the value of a company’s equity. It is not necessarily the “price tag” if the company were to be bought tomorrow—an acquisition of this scale would require a significant premium—but it reflects the collective confidence of millions of retail and institutional investors. For Apple, a high market cap is a testament to its “moat,” a term popularized by Warren Buffett to describe a business’s ability to maintain competitive advantages over its rivals to protect its long-term profits and market share.

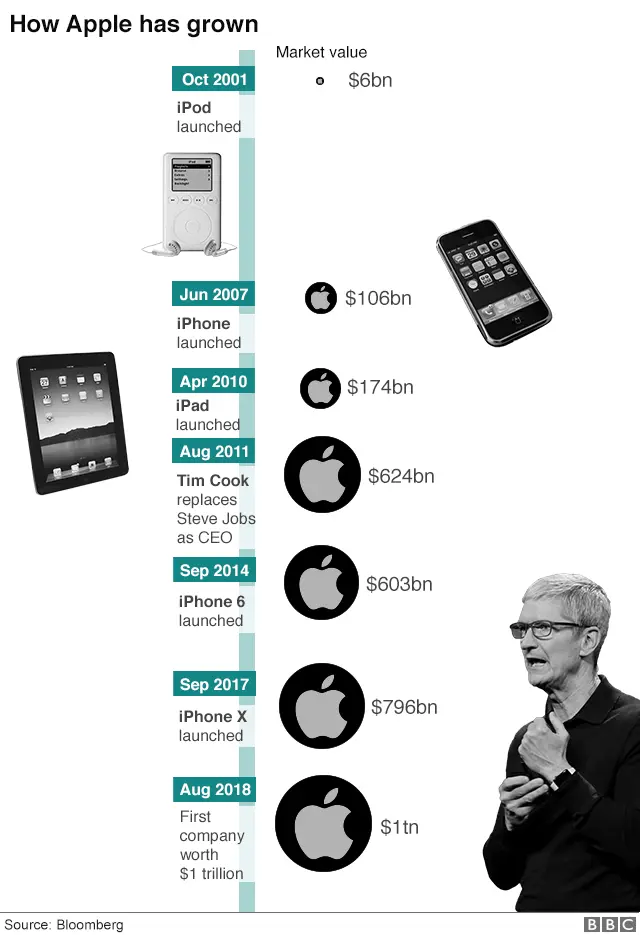

The Journey to the $3 Trillion Milestone

Apple’s ascent to the top of the financial world was not overnight. It took the company 42 years to reach a $1 trillion valuation in 2018. Remarkably, it took only two more years to hit $2 trillion in 2020, and just another 16 months to briefly touch $3 trillion in early 2022. This acceleration was driven by a combination of low interest rates, a global shift toward digital work during the pandemic, and an aggressive share repurchase program that reduced the supply of stock, thereby increasing the value of remaining shares.

Revenue Streams and Profitability: The Engine Behind the Valuation

A company is ultimately worth the present value of its future cash flows. Apple’s valuation is sustained by a massive revenue engine that generated nearly $400 billion in annual sales in recent fiscal years. To understand why the company is valued so highly, we must break down where that money comes from and, more importantly, how much of it is kept as profit.

Hardware Sales: The Foundation of Wealth

The iPhone remains the crown jewel of Apple’s financial portfolio, often accounting for 50% or more of total revenue. However, the “worth” of the company is increasingly tied to the ecosystem rather than just the device. While Mac, iPad, and Wearables (Apple Watch and AirPods) contribute tens of billions in revenue, they serve a secondary purpose: locking users into the Apple environment. From a financial perspective, every iPhone sold represents a recurring revenue opportunity through the “walled garden” effect.

The Services Pivot: High Margins and Recurring Income

The most significant driver of Apple’s valuation expansion over the last five years has been its Services division. This includes the App Store, iCloud, Apple Music, Apple Pay, and Apple TV+.

Why does Wall Street value Services more than hardware? The answer lies in the margins. Hardware typically has a gross margin of 35-40%, whereas Services enjoy margins north of 70%. Furthermore, Services provide “sticky” recurring revenue. Investors are willing to pay a premium (a higher P/E multiple) for a company that has predictable, subscription-based income compared to a company that must convince consumers to buy a new $1,000 phone every two years.

Investment Metrics: Why Wall Street Values Apple So Highly

Professional investors look at specific financial ratios to determine if Apple’s multi-trillion-dollar valuation is justified or if the stock is overpriced. When evaluating Apple’s worth, three factors stand out: the Price-to-Earnings (P/E) ratio, cash flow, and capital return programs.

Price-to-Earnings (P/E) Ratios and Growth Projections

The P/E ratio measures a company’s current share price relative to its per-share earnings. Historically, Apple traded at a “value” multiple of 12x to 15x earnings. However, as the company proved its resilience and grew its Services sector, that multiple expanded to 25x–30x. This expansion means that for every dollar Apple earns, investors are willing to pay $30 to own a piece of it. This premium is a reflection of Apple’s status as a “safe haven” asset—a stock that investors flock to during times of economic uncertainty because of its stable balance sheet.

Cash Reserves and Buyback Strategies

Apple is famous for its “cash pile,” which often exceeds $160 billion in cash and marketable securities. While having too much cash can sometimes be seen as inefficient, Apple uses it strategically through a “capital neutral” policy.

Since 2012, Apple has returned over $600 billion to shareholders through dividends and, more significantly, share buybacks. By repurchasing its own stock, Apple reduces the number of shares in circulation. For the remaining investors, this means their slice of the “Apple pie” becomes larger without them having to spend an extra dime. This financial engineering has been a massive contributor to the growth of Apple’s share price and its overall valuation.

Risks and Future Outlook: Protecting the $3 Trillion Valuation

No valuation is guaranteed, and for a company the size of Apple, the challenges are as large as the balance sheet. To maintain its status as the world’s most valuable company, Apple must navigate regulatory hurdles and find the “next big thing” to drive growth.

Regulatory Pressures and Antitrust Concerns

One of the primary threats to Apple’s worth is global regulation. In the European Union and the United States, regulators are increasingly scrutinizing the App Store’s commission structure and the “closed” nature of the iOS ecosystem. If Apple is forced to allow third-party app stores or reduce its 30% “Apple Tax,” it could significantly impact the high-margin Services revenue that investors value so dearly. Any threat to these margins typically results in a contraction of the P/E multiple, which can wipe hundreds of billions off the market cap in a matter of days.

Emerging Markets and Future Product Cycles

As the smartphone market in the U.S. and China reaches saturation, Apple’s future valuation depends on its success in emerging markets like India. With a growing middle class, India represents a massive untapped demographic for iPhone sales and subsequent services.

Furthermore, investors are looking for Apple’s play in Artificial Intelligence (AI) and Spatial Computing (Vision Pro). While the Vision Pro is currently a niche, high-cost item, its potential to eventually replace the laptop or tablet is what keeps the “growth story” alive. For Apple to reach a $4 trillion or $5 trillion valuation, it must prove that it can lead the next generation of computing just as it led the mobile revolution.

Conclusion: The Real Value of Apple

How much is Apple worth? Financially, it is the sum of its massive hardware profits, its high-margin services, and its unrivaled ability to generate cash. But to an investor, Apple’s worth is defined by its consistency. In a volatile market, Apple offers a rare combination of growth and security.

Whether the market cap sits at $2.8 trillion or $3.2 trillion on any given day, the underlying business remains a masterclass in financial management. By leveraging its brand to maintain high prices, using its cash to reward shareholders, and transitioning toward a service-oriented business model, Apple has redefined what it means to be a successful modern enterprise. For the foreseeable future, Apple will likely remain the gold standard against which all other corporate valuations are measured.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.