Purchasing a vehicle is often the second-largest financial commitment a person makes, surpassed only by the purchase of a home. Yet, a staggering number of consumers walk onto a dealership lot focusing solely on the “monthly payment” without understanding the underlying mechanics of interest, principal, and loan amortization.

When you focus only on the monthly figure, you lose sight of the total cost of ownership. Calculating your car payment with interest manually—or at least understanding the variables involved—empowers you to negotiate from a position of strength, avoid “predatory” long-term loans, and ensure your vehicle fits within a healthy personal finance framework.

The Anatomy of a Car Loan: Understanding the Variables

Before you can calculate a payment, you must understand the four primary components that dictate how much money leaves your bank account every month. Each of these variables is a lever; moving one will inevitably affect the others.

The Principal Amount

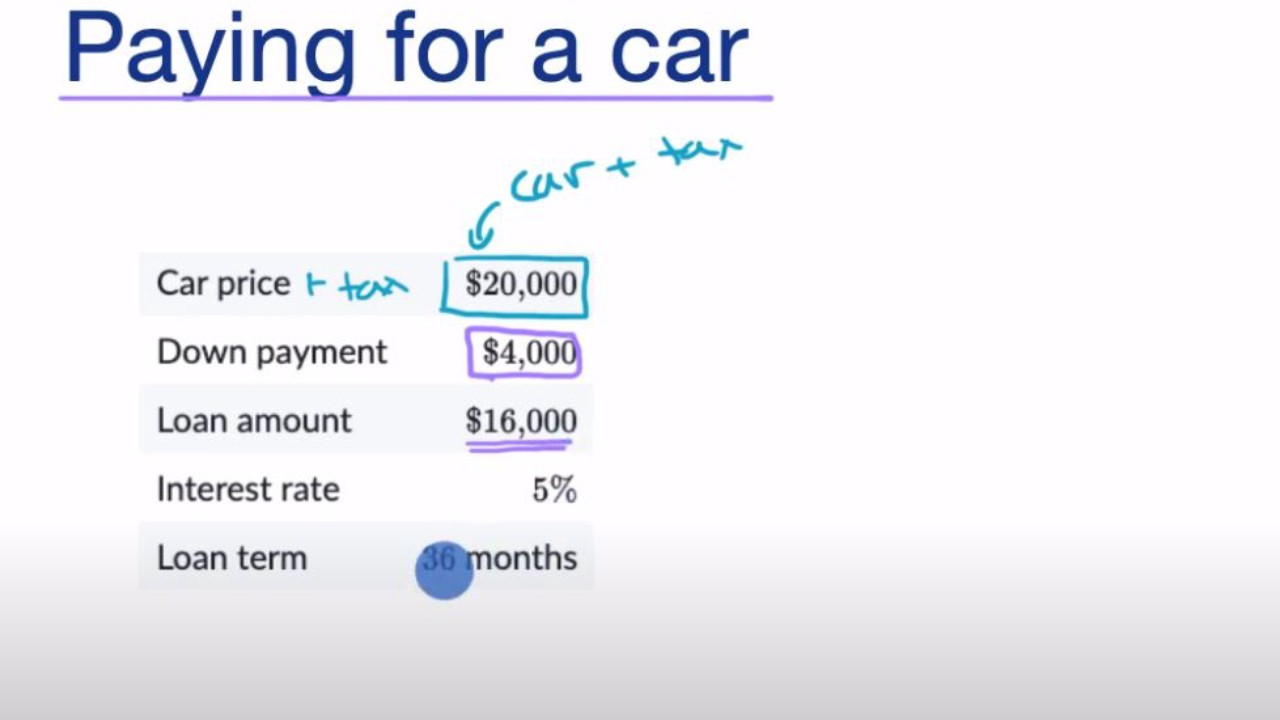

The principal is the actual amount of money you are borrowing from a lender to cover the cost of the vehicle. It is not necessarily the “sticker price” of the car. To find your principal, you take the agreed-upon purchase price, add sales tax, registration fees, and any dealer add-ons (like extended warranties), and then subtract your down payment and the value of any trade-in vehicle.

The Annual Percentage Rate (APR)

Interest is the “rent” you pay to use the lender’s money. In the world of auto finance, this is expressed as the Annual Percentage Rate (APR). Unlike simple interest, car loans are typically calculated using an amortization schedule. Your interest rate is heavily influenced by your credit score, the age of the vehicle (new cars usually have lower rates), and current market conditions set by the Federal Reserve.

The Loan Term

This is the duration you have to pay back the loan, usually expressed in months (e.g., 36, 48, 60, 72, or 84 months). While a longer term lowers your monthly payment, it significantly increases the total interest paid over the life of the loan. In the current financial climate, 60 months is considered the standard, while anything 72 months or higher is often viewed as a financial risk due to the potential for “negative equity.”

Taxes, Titles, and Fees

Many buyers forget that the “out-the-door” price is often 8% to 12% higher than the advertised price due to state sales tax, documentation fees, and title transfers. If you roll these costs into your loan instead of paying them upfront, you are essentially paying interest on taxes—a compounding expense that can add hundreds of dollars to your total cost.

How to Manually Calculate Your Monthly Payment

While digital calculators are convenient, knowing the mathematical formula allows you to understand the “why” behind the numbers. Car loans typically use a fixed-rate amortization formula.

The Standard Amortization Formula

The formula used to determine a monthly payment ($M$) is:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1 ]

Where:

- P = Principal loan amount

- i = Monthly interest rate (Annual rate divided by 12)

- n = Number of months (loan term)

Step 1: Converting APR to Monthly Interest

Lenders quote interest annually, but you pay monthly. If you are quoted a 6% APR, you must convert this to a decimal and divide by 12.

- 0.06 / 12 = 0.005.

In this case, i = 0.005.

Step 2: Running an Example Calculation

Let’s assume you are buying a car with a principal (P) of $30,000 at a 6% APR (i = 0.005) for 60 months (n = 60).

- Calculate (1 + i)^n: (1.005)^60 ≈ 1.34885

- Multiply by i: 0.005 * 1.34885 ≈ 0.006744

- Calculate the denominator [(1 + i)^n – 1]: 1.34885 – 1 = 0.34885

- Divide the results: 0.006744 / 0.34885 ≈ 0.01933

- Multiply by P: 30,000 * 0.01933 = $579.90

In this scenario, your monthly payment is approximately $580. Over 60 months, you will pay a total of $34,794, meaning the “cost” of the loan—the interest—was $4,794.

Factors That Influence Your Interest Rate and Total Cost

Knowing the formula is only half the battle. To secure the best deal, you need to understand the financial levers that banks use to determine your specific APR.

The Power of the Credit Score

Your credit score is the single most influential factor in determining your interest rate. Borrowers in the “Super Prime” category (780+) may see rates as low as 4-5%, while “Subprime” borrowers (below 600) might face rates of 15-20% or higher. On a $30,000 loan, the difference between a 5% rate and a 15% rate is over $9,000 in interest charges alone.

The Down Payment Strategy

A substantial down payment does more than just lower your monthly bill; it reduces the lender’s risk. Financial experts often recommend the 20/4/10 rule:

- Put 20% down.

- Limit the loan term to 4 years (48 months).

- Ensure total vehicle expenses (payment, insurance, fuel) do not exceed 10% of your gross income.

New vs. Used Vehicle Rates

Lenders generally offer lower interest rates on new cars because they have a higher resale value and are easier to repossess and sell if the borrower defaults. However, new cars depreciate faster. Used cars have higher interest rates but a lower overall principal, often making them the more “fiscally responsible” choice despite the higher APR.

Strategic Financial Tips to Lower Your Total Cost

Once you have calculated your potential payment, the goal shifts to optimization. How can you minimize the amount of interest leaving your pocket?

The Trap of the Long-Term Loan

In recent years, 72-month and 84-month loans have become common. While they make expensive SUVs look “affordable” on a monthly basis, they are dangerous. Cars are depreciating assets. If you take an 84-month loan with a small down payment, you will likely be “underwater” (owing more than the car is worth) for the majority of the loan term. This becomes a crisis if the car is totaled in an accident or if you need to sell it unexpectedly.

Pay Toward the Principal Early

Most auto loans are “simple interest” loans, meaning interest is calculated based on the balance on the day the payment is due. By making even small extra payments toward the principal (not just the next month’s payment), you reduce the balance upon which future interest is calculated. This can shave months off your loan and hundreds off your interest total.

Shop Your Rate Before Visiting the Dealer

The “F&I” (Finance and Insurance) office at a dealership is a profit center. Dealers often “mark up” the interest rate they get from a bank and pocket the difference. To combat this, get a pre-approval from a credit union or your local bank before you set foot on the lot. If the dealer wants your business, they will have to beat the rate you already have in hand.

When to Consider Refinancing

If you were forced to take a high-interest loan because your credit was poor at the time of purchase, you aren’t stuck with it forever. If you make on-time payments for 6 to 12 months and your credit score improves, you can refinance the loan with a different lender. Dropping your APR by just 2% or 3% can result in significant monthly savings.

Final Thoughts: The Value of Financial Literacy in Car Buying

Calculating a car payment with interest is more than just an exercise in algebra; it is a vital component of wealth management. When you understand that a $500 payment for 84 months is vastly different from a $500 payment for 48 months, you begin to see through the marketing tactics of the automotive industry.

By mastering the math of amortization, maintaining a strong credit profile, and adhering to conservative budgeting rules like the 20/4/10 guideline, you transform the car-buying process from a stressful negotiation into a calculated financial decision. Remember, the goal isn’t just to drive a car you love—it’s to do so without compromising your long-term financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.