Navigating the world of loans can often feel like deciphering a complex financial code. From interest rates to closing costs, numerous terms vie for your attention, each playing a role in the overall expense of borrowing money. Among these, the Annual Percentage Rate (APR) stands out as one of the most critical, yet frequently misunderstood, metrics. For anyone considering a loan—whether it’s a mortgage, an auto loan, a personal loan, or a credit card—understanding APR is not just important; it’s essential for making informed financial decisions and protecting your long-term fiscal health.

At its core, APR represents the true annual cost of borrowing. It’s designed to provide a comprehensive, standardized measure that allows consumers to compare different loan offers on an “apples-to-apples” basis. However, its nuances extend far beyond a simple percentage, encompassing not only the interest charged but also various fees and additional costs bundled into the loan. This article will demystify APR, explore its components and variations, and equip you with the knowledge to leverage this powerful metric in your personal finance journey.

Demystifying APR: The True Cost of Borrowing

When you borrow money, you’re not just paying back the principal amount; you’re also paying for the privilege of using someone else’s capital. This “cost” comes in various forms, and APR is designed to capture a significant portion of it.

Defining APR (Annual Percentage Rate)

APR stands for Annual Percentage Rate. In simple terms, it is the yearly rate charged for borrowing, or earned by investing, expressed as a single percentage number that represents the actual yearly cost of funds over the term of a loan. This definition is crucial because it immediately tells you that APR is more than just the interest rate quoted by a lender.

While the nominal interest rate tells you how much interest you’ll pay on the principal balance, the APR includes this interest rate plus other charges, such as origination fees, discount points, and other administrative costs directly associated with obtaining the loan. The primary purpose of APR is to standardize the disclosure of credit costs, allowing consumers to compare various loan products more effectively, even if they come from different lenders with different fee structures. It’s a regulatory requirement, particularly in the United States under the Truth in Lending Act (TILA), ensuring transparency in lending practices.

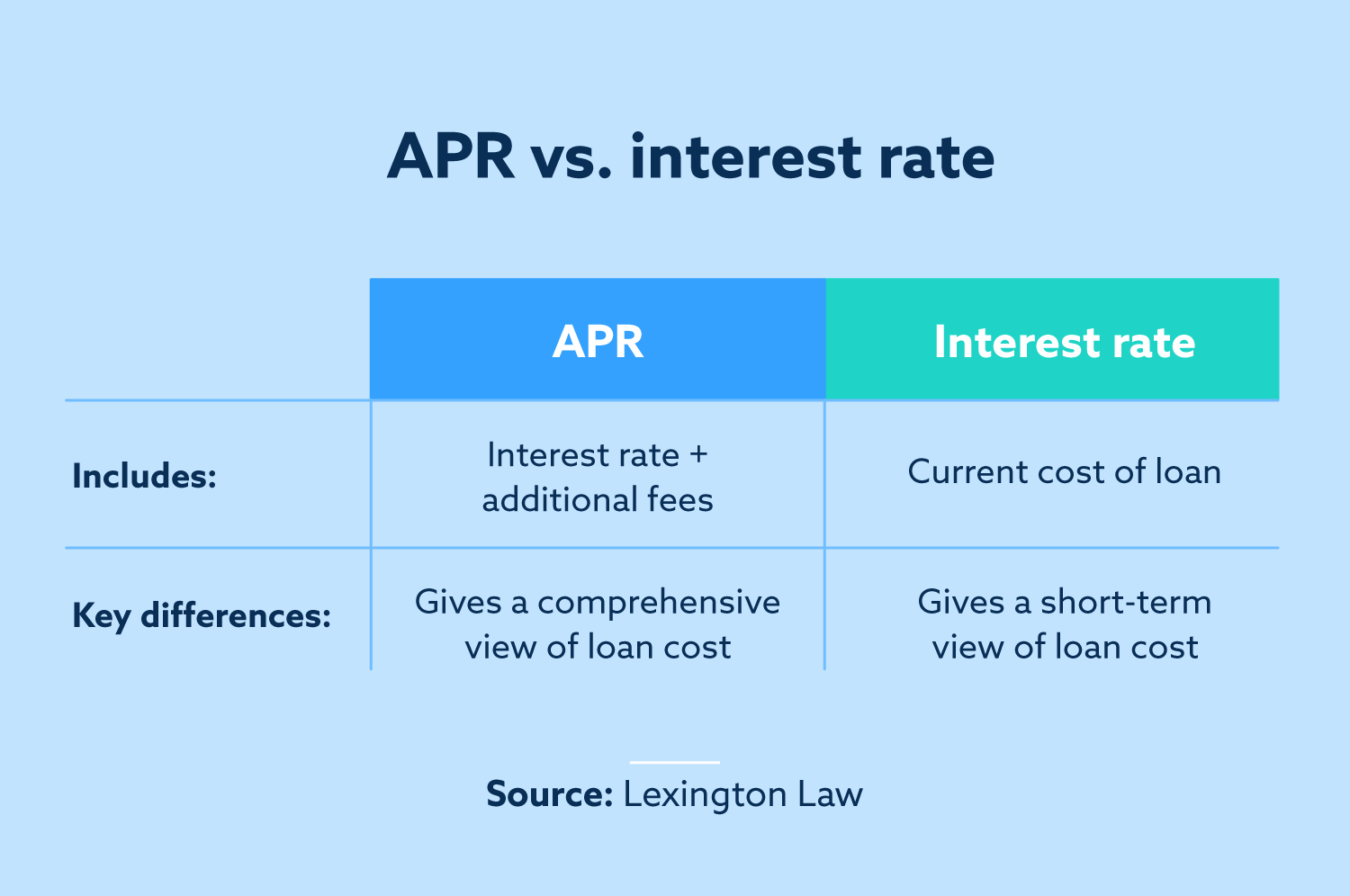

APR vs. Interest Rate: A Crucial Distinction

Perhaps the most common point of confusion for borrowers is distinguishing between the interest rate and the APR. While the terms are often used interchangeably in casual conversation, they represent distinct financial concepts:

- Interest Rate: This is the percentage charged by the lender on the principal amount of the loan. It’s the core cost of borrowing money. If you have a $10,000 loan at a 5% interest rate, you’ll pay $500 in interest for that year (assuming no other factors).

- Annual Percentage Rate (APR): As mentioned, the APR takes the interest rate and adds certain mandatory fees and additional costs associated with the loan. These fees might include loan origination fees, processing fees, underwriting fees, or even private mortgage insurance premiums (for some loans). Because it incorporates these additional costs, the APR will almost always be higher than the nominal interest rate.

Consider two loan offers for the same principal amount and term:

- Loan A: Offers a 4.0% interest rate with a 2% origination fee.

- Loan B: Offers a 4.2% interest rate with no origination fee.

If you only looked at the interest rate, Loan A might seem more attractive. However, once the origination fee is factored into the APR calculation, Loan A’s APR could potentially be higher than Loan B’s, revealing that Loan B is, in fact, the cheaper option overall. This illustrates why relying solely on the interest rate can be misleading and why APR is the more comprehensive metric for comparing loan costs.

Components of APR

To fully grasp APR, it helps to understand what typically gets included in its calculation. The specific components can vary slightly depending on the type of loan (e.g., mortgage vs. personal loan), but generally, they fall into two categories:

- The Interest Rate: This is the base percentage charged on the principal.

- Certain Fees and Charges: These are costs directly related to setting up the loan. Common examples include:

- Loan Origination Fees: A fee charged by the lender for processing the loan application. It’s often expressed as a percentage of the loan amount.

- Discount Points: Fees paid upfront to reduce the interest rate on the loan. Each “point” is typically 1% of the loan amount.

- Broker Fees: If a mortgage broker is used, their fees are often included.

- Underwriting Fees: Charges for evaluating the loan application and borrower’s creditworthiness.

- Private Mortgage Insurance (PMI): For conventional mortgages where the borrower puts down less than 20%, PMI might be rolled into the APR calculation for specific disclosure purposes, though it’s an ongoing premium.

- Prepaid Interest: Sometimes, interest that accrues between the closing date and the first payment due date is factored in.

It’s important to note that not all fees associated with a loan are included in the APR. For example, third-party costs like attorney fees, notary fees, appraisal fees, credit report fees, and title insurance (for mortgages) are typically not included in the APR calculation, even though they are part of your overall closing costs. This distinction further emphasizes the importance of scrutinizing the complete loan estimate.

Types of APR and How They Impact Your Loan

APR isn’t a monolithic concept; it comes in various forms, each with its own implications for borrowers. Understanding these different types is crucial for managing your debt effectively.

Fixed APR vs. Variable APR

One of the most significant distinctions in APR is whether it’s fixed or variable:

- Fixed APR: As the name suggests, a fixed APR remains constant throughout the life of the loan. This provides stability and predictability, as your interest rate and corresponding payment will not change due to market fluctuations. Fixed-rate mortgages and traditional personal loans commonly feature fixed APRs, making budgeting easier and offering peace of mind. The downside is that you won’t benefit if market interest rates drop, as your rate will remain the same.

- Variable APR: A variable APR, also known as a fluctuating or adjustable APR, changes over time based on an underlying benchmark index (e.g., the Prime Rate, SOFR – Secured Overnight Financing Rate). It’s typically expressed as “index + margin.” Common examples include credit cards, Home Equity Lines of Credit (HELOCs), and Adjustable-Rate Mortgages (ARMs). The main advantage is that your payments could decrease if the index falls, but conversely, they could increase if the index rises, introducing uncertainty into your monthly budget. Variable APRs often come with caps (limits on how much the rate can increase or decrease) to protect consumers from extreme fluctuations.

Choosing between fixed and variable APR depends on your risk tolerance, financial stability, and outlook on future interest rate movements.

Purchase APR, Balance Transfer APR, and Cash Advance APR (Credit Cards Specific)

Credit cards are unique in that they often have multiple APRs applicable to different types of transactions:

- Purchase APR: This is the standard rate applied to new purchases made with the credit card if you don’t pay your balance in full by the due date each month. It’s the most commonly advertised APR for a credit card.

- Balance Transfer APR: This is the rate applied to balances transferred from other credit cards or loans to the new card. Lenders often offer promotional, lower APRs (sometimes 0%) for balance transfers for an introductory period, after which the rate reverts to a higher standard rate (which might be the purchase APR or a specific balance transfer rate).

- Cash Advance APR: This is the rate applied to cash advances taken from your credit card. Cash advance APRs are typically the highest of all credit card APRs and usually do not have a grace period, meaning interest starts accruing immediately from the transaction date.

- Introductory/Promotional APR: Many credit cards offer a low or 0% APR for a limited time (e.g., 6, 12, or 18 months) on purchases or balance transfers. This “teaser rate” is designed to attract new customers. Once the introductory period ends, the APR reverts to the standard purchase APR. It’s crucial to understand when these periods end and what the regular APR will be.

- Penalty APR: If you violate the terms of your credit card agreement, such as making late payments, the issuer may impose a penalty APR. This rate is significantly higher than your standard purchase APR and can be applied to all existing and new balances. It serves as a strong deterrent against irresponsible credit behavior.

Being aware of these different credit card APRs is paramount for managing your credit card debt effectively and avoiding unexpected costs.

Calculating and Comparing APR: Empowering Your Borrowing Decisions

Understanding the theoretical aspects of APR is one thing; using it practically to make smart financial decisions is another. The ability to compare loan offers accurately based on their APRs is a powerful tool in your financial arsenal.

How APR is Calculated (Conceptual)

While the exact mathematical formulas for calculating APR can be complex and are often handled by financial institutions using specialized software, the underlying concept is straightforward: the total cost of credit, expressed as an annual percentage.

Essentially, the lender takes all the costs included in the APR (the nominal interest payments over the loan term plus all applicable fees) and spreads them out over the life of the loan. This total cost is then divided by the loan amount and annualized to arrive at the APR. The key takeaway for consumers is that you don’t need to perform the calculation yourself; lenders are legally obligated to disclose the APR to you clearly. This transparency, mandated by regulations like the Truth in Lending Act, empowers you to see the actual cost beyond just the interest rate.

The Power of APR in Loan Comparison

The most significant benefit of APR is its role as the ultimate comparison tool. When you receive multiple loan offers, each might present a different interest rate and a unique set of fees. Without APR, comparing these offers would be like trying to compare apples and oranges.

Let’s revisit our earlier example:

- Loan A: Interest Rate: 4.0%, Origination Fee: 2% ($200 on a $10,000 loan)

- Loan B: Interest Rate: 4.2%, Origination Fee: 0%

If Loan A has an interest rate of 4.0% but an APR of 4.35% (due to fees), and Loan B has an interest rate of 4.2% and an APR of 4.2% (no fees), then Loan B is the cheaper option despite having a higher nominal interest rate. The APR effectively “packages” all the relevant costs into a single, digestible percentage, allowing you to directly see which loan truly costs less over its lifetime.

Always demand to know the APR when shopping for any loan, and use it as your primary metric for comparing offers from different lenders. It simplifies complex financial decisions into a single, comparable figure.

Factors Affecting Your APR

Several factors influence the APR you’re offered, as lenders assess risk to determine the rate they are willing to provide:

- Credit Score: This is arguably the most impactful factor. Borrowers with excellent credit scores (typically 760+) are considered lower risk and will qualify for the lowest available APRs. Those with lower scores will be offered higher APRs to compensate the lender for the increased risk of default.

- Debt-to-Income (DTI) Ratio: Your DTI ratio, which compares your monthly debt payments to your gross monthly income, indicates your capacity to take on new debt. A lower DTI generally signifies less risk and can lead to a more favorable APR.

- Loan Term: The length of the repayment period can influence APR. Shorter-term loans sometimes come with slightly lower APRs because the lender’s risk exposure is for a shorter duration. However, this isn’t always the case, and longer terms often lead to more total interest paid over time, even if the monthly payments are lower.

- Loan Type: Different types of loans carry different risk profiles. Secured loans (like auto loans or mortgages, backed by collateral) generally have lower APRs than unsecured loans (like personal loans or credit cards), where there’s no asset for the lender to seize if you default.

- Market Conditions: The overall economic environment and prevailing interest rates set by central banks (like the Federal Reserve) significantly influence the base rates lenders offer. When central bank rates rise, so do consumer loan APRs.

- Down Payment/Collateral: For secured loans, a larger down payment or more valuable collateral can reduce the lender’s risk, potentially leading to a lower APR.

Understanding these factors allows you to take steps to improve your creditworthiness and negotiate for the best possible APRs.

Beyond APR: Other Considerations for Smart Borrowing

While APR is an invaluable tool, it shouldn’t be your only consideration when taking out a loan. A holistic approach to borrowing involves looking at the bigger financial picture.

Total Loan Cost

While APR helps compare the rate of cost, it’s also crucial to consider the total dollar amount you will pay over the life of the loan. A loan with a slightly lower APR but a very long repayment term might end up costing you more in total interest than a loan with a slightly higher APR but a shorter term. Always ask for the total projected cost of the loan, including all principal and interest payments. This figure gives you a concrete understanding of how much money will leave your pocket.

Loan Term and Monthly Payments

The length of your loan (the “term”) directly impacts your monthly payments and the total interest paid.

- Longer Loan Term: Results in lower monthly payments, which can make a loan more affordable on a month-to-month basis. However, because you’re paying interest for a longer period, the total amount of interest paid over the life of the loan will be significantly higher.

- Shorter Loan Term: Results in higher monthly payments, which might strain your budget. But, you’ll pay off the loan faster and incur substantially less total interest.

The optimal loan term balances affordability with minimizing total interest paid, aligning with your personal budget and financial goals.

Prepayment Penalties and Other Fine Print

Before signing any loan agreement, meticulously read the fine print. Look for:

- Prepayment Penalties: Some loans charge a fee if you pay off the loan early or make extra payments that significantly reduce the principal ahead of schedule. While less common now, especially for consumer loans, they can exist and effectively negate the benefit of early repayment.

- Late Payment Fees: Understand the charges for missed or late payments.

- Other Hidden Fees: Are there any annual fees, maintenance fees, or other charges not included in the APR that could add to your overall cost?

- Escrow Requirements: For mortgages, understand if you’ll need an escrow account for property taxes and insurance.

A comprehensive review of the loan agreement ensures you’re aware of all potential costs and terms, preventing unwelcome surprises down the line.

Strategic Uses of APR in Financial Planning

Understanding and utilizing APR strategically can significantly enhance your financial planning and debt management efforts.

Optimizing Debt Management

APR can be a powerful guide in optimizing your debt repayment strategy:

- Debt Avalanche Method: This popular strategy involves prioritizing debts with the highest APR first, regardless of the balance. By tackling the most expensive debt first, you minimize the total interest paid over time, saving money and accelerating your path to debt freedom.

- Refinancing: If your credit score has improved significantly, market interest rates have dropped, or you’re struggling with a high-interest loan, understanding APR can help you decide if refinancing is a viable option. Refinancing aims to secure a new loan with a lower APR, reducing your monthly payments or the total cost of interest.

Informed Decision-Making

Every major financial decision involving borrowing should begin with an examination of the APR:

- Major Purchases: Whether financing a car, a home, or even a large appliance, comparing the APRs from different lenders for different financing options can save you thousands of dollars.

- Credit Card Usage: Being aware of the different APRs on your credit card helps you avoid costly mistakes, like taking a cash advance or carrying a balance after an introductory period.

Building and Maintaining Good Credit

The link between your credit health and the APRs you qualify for is undeniable. A strong credit score (built through timely payments, low credit utilization, and a long credit history) is your ticket to accessing the lowest possible APRs. By understanding this relationship, you’re incentivized to maintain good credit, which in turn leads to cheaper borrowing costs and better financial flexibility in the future.

Conclusion

The Annual Percentage Rate (APR) is far more than just another financial term; it is the most critical metric for truly understanding the cost of a loan. By encompassing not only the interest rate but also various fees, APR provides a standardized, comprehensive measure that empowers borrowers to compare different loan offers accurately and make financially sound decisions.

From distinguishing between fixed and variable rates to recognizing the different APRs on a credit card, a thorough understanding of this concept puts you in the driver’s seat of your financial future. While APR is paramount, remember to also consider the total loan cost, the loan term, and the fine print, including potential prepayment penalties. Armed with this knowledge, you can approach borrowing with confidence, secure the most favorable terms, and strategically manage your debt to achieve your personal finance goals. In the intricate world of money, knowledge truly is power, and understanding APR is a cornerstone of that power.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.