California, known for its innovation, vibrant economy, and stunning landscapes, also holds the distinction of having one of the most complex and progressive state income tax systems in the United States. For residents and those considering a move to the Golden State, understanding the intricacies of California’s tax brackets is not just a matter of compliance, but a crucial element of sound financial planning. This comprehensive guide will demystify California’s income tax structure, helping you grasp how your earnings are taxed and what factors influence your overall tax burden.

California operates on a progressive income tax system, meaning that as your taxable income increases, so does the percentage of tax you pay on those higher portions of your income. Unlike a flat tax system, where everyone pays the same percentage regardless of income, California’s approach aims to distribute the tax burden more equitably, with higher earners contributing a larger share. This system, while sometimes perceived as burdensome, is fundamental to funding the state’s extensive public services, infrastructure, and social programs. Navigating these brackets effectively requires a clear understanding of your filing status, income sources, and available deductions and credits.

Understanding California’s Progressive Income Tax System

The bedrock of California’s state income taxation is its progressive structure. This system isn’t unique to California; the federal income tax system also employs a progressive model. However, California’s state-level application is notable for its relatively high top marginal rates and the breadth of its income brackets.

The Core Principle of Progressive Taxation

At its heart, a progressive tax system means that different portions of your income are taxed at different rates. Imagine your total taxable income as a series of layers. The lowest layer is taxed at the lowest rate, the next layer at a slightly higher rate, and so on. This continues up to the highest layer of income, which is taxed at the top marginal rate. Crucially, this does not mean your entire income is taxed at the highest bracket you fall into. Only the portion of your income that falls within a particular bracket is taxed at that bracket’s rate. This distinction is vital for understanding your true tax liability.

For example, if the first $10,000 of income is taxed at 1%, and the next $10,000 at 2%, someone earning $15,000 would pay 1% on their first $10,000 and 2% on the remaining $5,000. They would not pay 2% on the full $15,000. This is the essence of marginal tax rates, which we’ll explore in more detail.

Who Pays California State Income Tax?

Generally, anyone who is a resident of California or earns income from California sources, even if they are not a resident, is subject to California state income tax. A “resident” for tax purposes is broadly defined as someone who is in California for other than a temporary or transitory purpose, or someone who is domiciled in California but outside the state for a temporary or transitory purpose. This definition can be complex and depends on various factors, including the amount of time spent in the state, the location of your permanent home, family, and business interests. Non-residents, on the other hand, are typically taxed only on income derived from California sources, such as wages earned for work performed in California, or income from a business located in the state. Understanding your residency status is the first critical step in determining your California tax obligations.

Key Differences from Federal Tax Brackets

While both California and the federal government use progressive tax systems, there are significant differences. California’s state income tax system has its own set of brackets, rates, deductions, and credits, which are entirely separate from the federal system. One of the most prominent differences is the number of brackets and the highest marginal rates. California typically has more income tax brackets than the federal system, and its top marginal rate can be substantially higher than the federal top rate, particularly when considering the additional “millionaire’s tax” (Mental Health Services Tax). Furthermore, some deductions and credits available at the federal level may not apply to your California state return, and vice-versa. Therefore, it’s essential to prepare your state tax return with California-specific rules in mind, rather than simply replicating your federal calculations.

Navigating California’s Tax Brackets: Filing Status Matters

Just like with federal income taxes, your filing status plays a pivotal role in determining which set of tax brackets applies to your income in California. The thresholds for each bracket vary significantly based on whether you are single, married, or head of household, among other statuses. It’s crucial to select the correct filing status, as an error can lead to incorrect tax calculations or potential penalties.

Single Filers

This status applies to individuals who are unmarried, legally separated, or divorced at the end of the tax year, and who do not qualify for another filing status. Single filers typically face the lowest income thresholds for each tax bracket, meaning they reach higher marginal tax rates at lower levels of income compared to married couples filing jointly.

Married Filing Jointly / Registered Domestic Partner (RDP) Filing Jointly

Married couples or registered domestic partners who choose to file a single tax return together use this status. In California, RDPs are treated the same as married couples for state income tax purposes. This status generally offers wider income brackets compared to single filers, meaning that a combined income reaches higher marginal rates at a higher overall income level. This is often referred to as a “marriage bonus” in terms of bracket application, as it typically results in a lower overall tax liability than if each spouse filed as single (assuming equal incomes).

Married Filing Separately / RDP Filing Separately

While married couples or RDPs can file separately, this status often results in a higher overall tax burden for the couple compared to filing jointly. The income thresholds for each bracket are typically half of what they would be for married filing jointly. There are specific circumstances where filing separately might be advantageous, such as when one spouse has significant deductions for medical expenses and their Adjusted Gross Income (AGI) threshold needs to be met individually. However, for most couples, joint filing is more tax-efficient.

Head of Household

This status is available to unmarried individuals who pay more than half the cost of keeping up a home for themselves and a qualifying person (e.g., a dependent child or relative) for more than half the year. Head of household filers typically benefit from wider tax brackets and potentially larger standard deductions than single filers, making it a more advantageous status for those who qualify.

Qualifying Widow(er)

This status applies to a widow or widower who has a dependent child and meets certain criteria for up to two years after the death of their spouse. It typically offers the same tax brackets as married filing jointly, providing a continuation of tax benefits for surviving spouses during a challenging period.

How California Tax Brackets Are Applied: Beyond the Percentage

Understanding the mere percentage rates of each bracket is only half the battle. To truly grasp your tax liability, you need to differentiate between marginal and effective tax rates and comprehend how deductions and credits fit into the picture.

Marginal vs. Effective Tax Rates

This is a critical distinction that often confuses taxpayers.

- Marginal Tax Rate: This is the tax rate applied to your last dollar of taxable income. When people talk about “being in a certain tax bracket,” they are usually referring to their highest marginal tax rate. As explained earlier, a progressive system means not all your income is taxed at this highest rate; only the portion that falls into that highest bracket.

- Effective Tax Rate: This is the total amount of tax you pay divided by your total taxable income. It represents the actual percentage of your income that goes towards taxes. Because of the progressive nature of the brackets, your effective tax rate will always be lower than your highest marginal tax rate (unless you only earn income within the lowest bracket). The effective rate provides a more accurate picture of your overall tax burden.

For financial planning, both rates are important. Your marginal rate helps you understand the tax implications of earning an additional dollar, while your effective rate gives you a broader sense of your total tax burden.

The Impact of Deductions and Credits

Before your income is subjected to the tax bracket rates, it undergoes a crucial transformation through deductions and credits, which significantly reduce your tax liability.

- Deductions: These reduce your taxable income. When you take a deduction, the amount is subtracted from your gross income, lowering the amount of income that is then run through the tax brackets. Deductions are “worth” your marginal tax rate. For example, a $1,000 deduction in a 5% marginal bracket saves you $50 in taxes. California offers its own set of standard and itemized deductions, which may differ from federal deductions. Itemized deductions in California can include state income taxes paid (with limitations), mortgage interest, charitable contributions, and certain medical expenses.

- Credits: These directly reduce your tax liability dollar-for-dollar. A $1,000 credit reduces your final tax bill by $1,000, regardless of your tax bracket. Credits are generally more powerful than deductions of the same amount. California offers various state-specific tax credits, such as the California Earned Income Tax Credit (CalEITC), Dependent Exemption Credits, and credits for specific activities or investments. Maximizing eligible deductions and credits is a cornerstone of effective tax planning.

Understanding Taxable Income in California

Your taxable income for California state purposes is not simply your gross income. It’s calculated by taking your gross income and subtracting eligible adjustments, deductions, and exemptions.

- Gross Income: All income from whatever source derived, unless specifically excluded by law. This includes wages, salaries, tips, interest, dividends, business income, rental income, and capital gains.

- Adjustments to Income: Certain deductions taken “above the line,” meaning they reduce your gross income before you even get to the standard or itemized deduction choice. Examples might include contributions to traditional IRAs, self-employment tax deductions, and health savings account (HSA) contributions (though HSA rules can differ between federal and state).

- Standard Deduction vs. Itemized Deductions: After adjustments, you choose between the California standard deduction (a fixed amount based on your filing status) or itemizing your deductions (listing specific deductible expenses). You typically choose whichever results in a larger reduction to your taxable income.

- Exemptions: California also allows for dependent exemption credits, which directly reduce your tax liability. These are distinct from personal exemptions which have largely been eliminated at the federal level but still exist in some form in California.

The final figure after all these subtractions is your taxable income, which is then applied to the appropriate California tax brackets to determine your initial tax liability.

Additional California Taxes and Considerations Beyond Brackets

While income tax brackets are a primary concern, California’s overall tax landscape includes several other significant taxes and unique considerations that can impact your financial picture. A holistic view is essential for comprehensive financial planning.

Capital Gains and Dividends

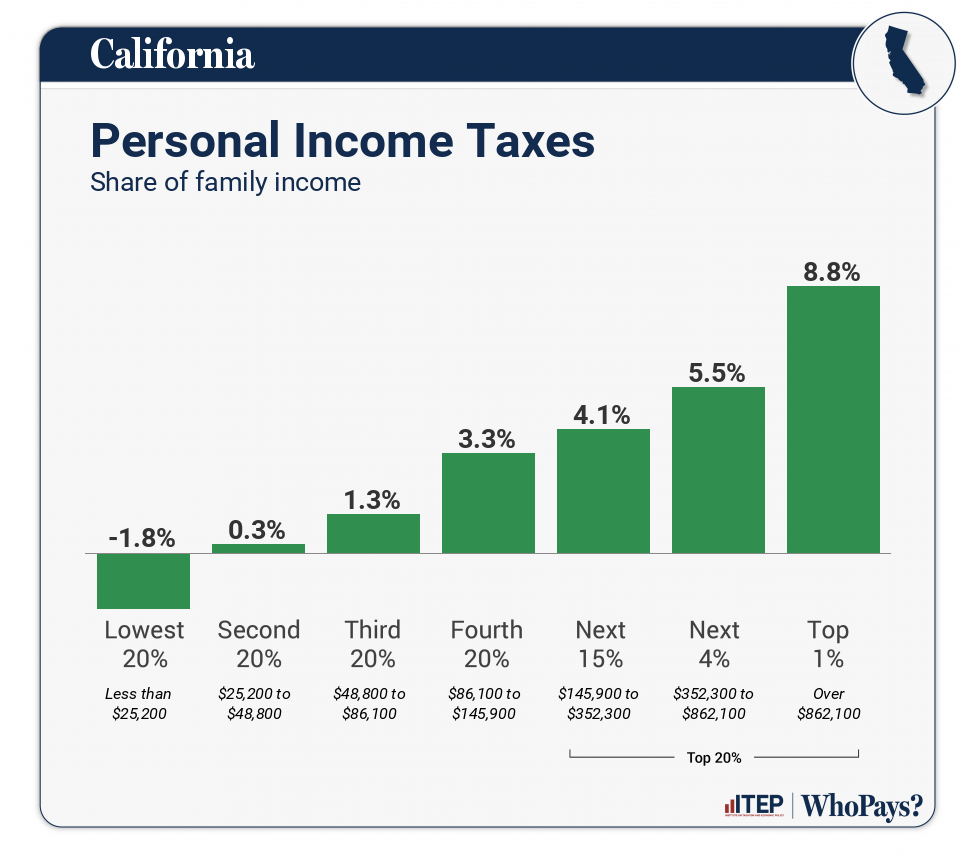

Unlike the federal system, which often taxes long-term capital gains at preferential rates, California generally treats capital gains and qualified dividends as ordinary income. This means they are added to your other income and subjected to the same progressive income tax brackets. This can have a substantial impact on investors, particularly those with significant investment portfolios or those who frequently buy and sell assets. Understanding this can influence investment strategies, such as tax-loss harvesting or holding investments for longer periods to defer realization of gains.

Sales Tax and Property Tax: A Broader Context

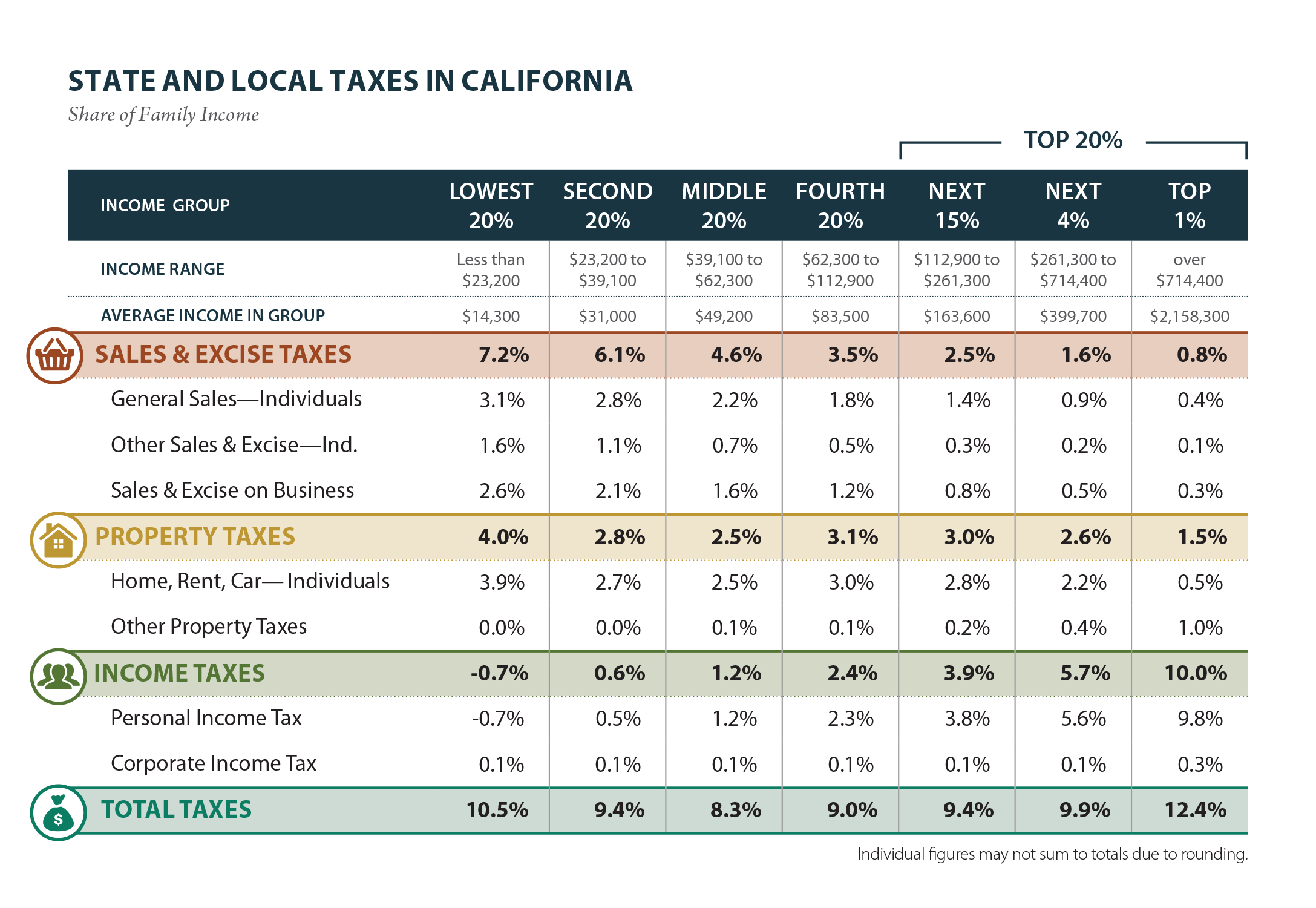

Beyond income tax, California has some of the highest sales tax rates in the nation, with a statewide base rate supplemented by local district taxes that can push the combined rate significantly higher depending on your location. Similarly, property taxes, while subject to Proposition 13 which limits annual increases in assessed value, can still be substantial, especially for new homebuyers or those in highly desirable areas. While not directly tied to income brackets, these consumption and wealth taxes contribute significantly to the overall tax burden for California residents and should be factored into any financial assessment.

The Millionaire’s Tax (Mental Health Services Tax)

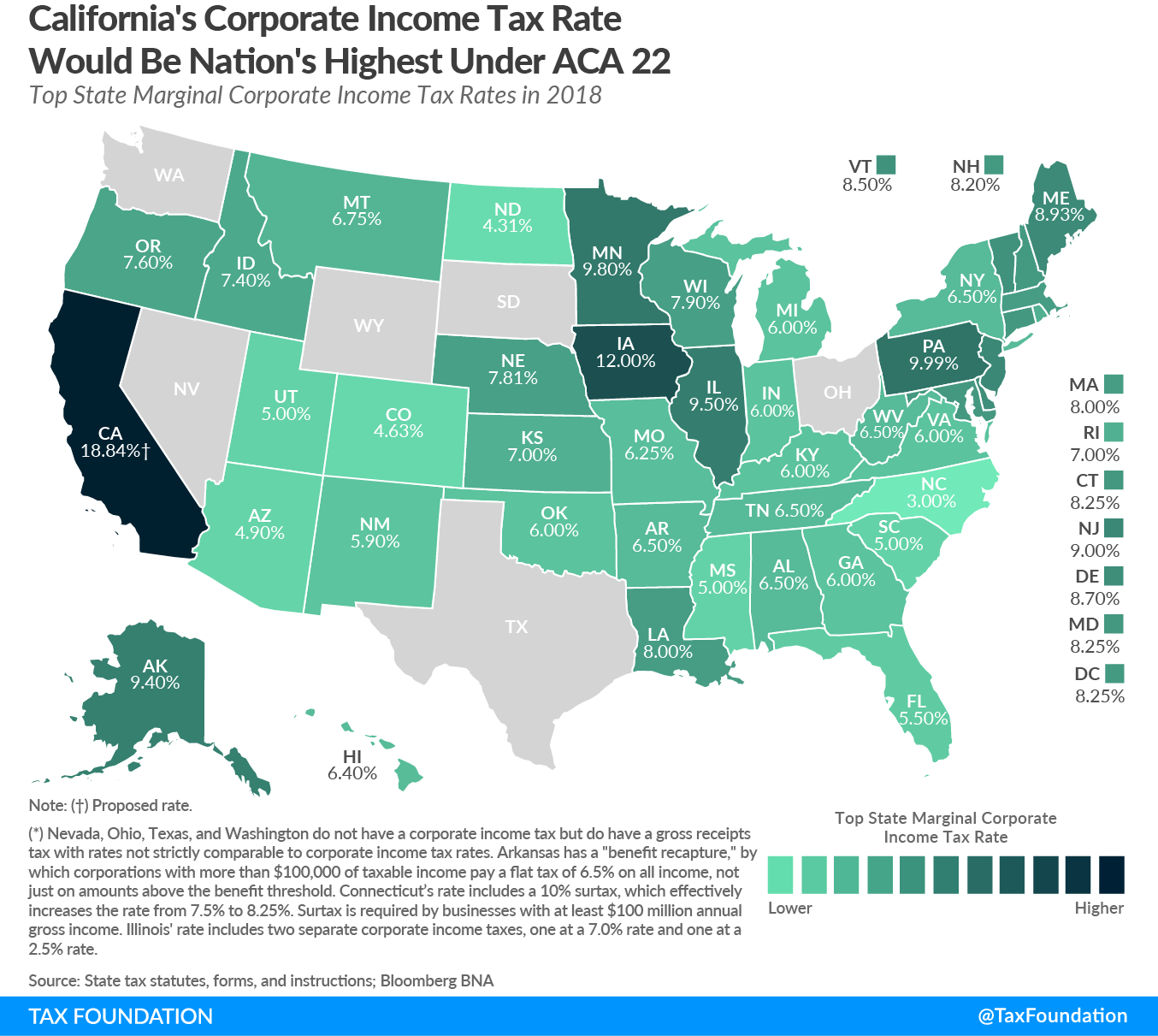

California has an additional 1% tax on taxable income over $1 million. This surcharge, often referred to as the “millionaire’s tax” or the “Mental Health Services Tax” (MHSA), is levied on top of the highest marginal income tax rate. It applies to individuals, not just to the state’s wealthiest, and is specifically earmarked to fund mental health services within the state. For high-income earners, this additional 1% can push their effective marginal state income tax rate to one of the highest in the country, further emphasizing California’s progressive tax structure.

Local Taxes and Fees

While most of the income tax discussion centers on state-level brackets, it’s also worth noting that various local taxes and fees can apply depending on your city or county. These might include parcel taxes, utility user taxes, or specific local levies that fund municipal services. While not directly income tax brackets, they add to the overall cost of living and doing business in specific parts of California. Awareness of these localized charges is important for a complete financial outlook.

Strategies for Managing Your California Tax Burden

Understanding California’s tax brackets is the first step; the next is to proactively manage your tax burden. While you cannot change the tax rates, you can employ various strategies to optimize your financial position within the existing framework.

Leveraging Deductions and Credits

The most immediate and impactful strategy is to diligently track and claim all eligible deductions and credits. This means keeping meticulous records of expenses that might qualify for itemized deductions, such as mortgage interest, property taxes (within federal limits), state income taxes paid, and charitable contributions. Furthermore, research state-specific credits like the California Earned Income Tax Credit (CalEITC), Young Child Tax Credit, or any other credits applicable to your circumstances (e.g., for energy-efficient home improvements, dependent care, or specific industries). Even small deductions and credits can add up to significant savings.

Retirement Planning and Tax-Advantaged Accounts

Utilizing tax-advantaged retirement accounts is a powerful long-term strategy. Contributions to traditional IRAs and 401(k)s are often tax-deductible in the year they are made, reducing your current taxable income and thus your current year’s tax liability within California’s brackets. While withdrawals in retirement will be taxed, you benefit from tax-deferred growth and potentially lower tax brackets in retirement. Health Savings Accounts (HSAs) also offer a triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses) which can be leveraged for both healthcare and retirement savings, though California’s treatment of HSA contributions can sometimes differ slightly from federal.

Professional Guidance: When to Seek an Expert

Given the complexity of California’s tax laws, especially for individuals with varied income sources, high net worth, or complex financial situations (e.g., business owners, investors, those with out-of-state income), seeking professional guidance is highly recommended. A qualified Certified Public Accountant (CPA) or enrolled agent specializing in California tax law can help you:

- Accurately determine your filing status.

- Identify all eligible deductions and credits.

- Navigate nuanced rules regarding residency, capital gains, and business income.

- Develop proactive tax planning strategies to minimize future liabilities.

- Represent you in the event of an audit by the Franchise Tax Board (FTB).

The investment in professional advice can often pay for itself through avoided errors and optimized tax savings.

Staying Informed About Tax Law Changes

Tax laws are not static; they evolve annually, often with significant changes at both federal and state levels. California frequently adjusts its tax brackets for inflation, introduces new credits, or modifies existing rules. Subscribing to financial news, reputable tax publications, or newsletters from tax professionals can help you stay abreast of these changes. Being informed ensures that your tax planning strategies remain current and effective, preventing missed opportunities or unintended non-compliance.

Understanding California’s tax brackets and the broader state tax environment is a cornerstone of responsible personal finance for anyone living, working, or investing in the Golden State. While the system can appear daunting due to its progressivity and complexity, a clear grasp of its mechanisms, coupled with strategic planning and, when necessary, professional guidance, empowers you to navigate your tax obligations effectively and efficiently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.