Navigating the world of taxes can often feel like deciphering a complex code, filled with jargon and intricate rules. Among the most fundamental concepts that every individual and business owner should grasp is that of “tax deductibles.” Far from being a mere accounting technicality, understanding and strategically utilizing tax deductibles is a cornerstone of effective financial planning, enabling taxpayers to legally reduce their taxable income and, consequently, their overall tax liability. In essence, a tax deductible is an expense that can be subtracted from your gross income, lowering the amount of income on which you are taxed. This seemingly simple mechanism holds significant power in optimizing your financial health, allowing you to retain more of your hard-earned money.

This comprehensive guide will demystify tax deductibles, exploring what they are, how they function, and the various categories that apply to individuals and businesses alike. We will delve into the strategic considerations necessary to maximize their benefits and highlight the critical importance of accurate record-keeping and compliance.

Understanding the Core Concept of Tax Deductibles

At its heart, a tax deductible is an allowable expense that can be subtracted from a taxpayer’s gross income before calculating their tax liability. The goal is to ensure that you are only taxed on the income you genuinely had available for personal use or investment after certain necessary or encouraged expenditures.

Defining Tax Deductibles

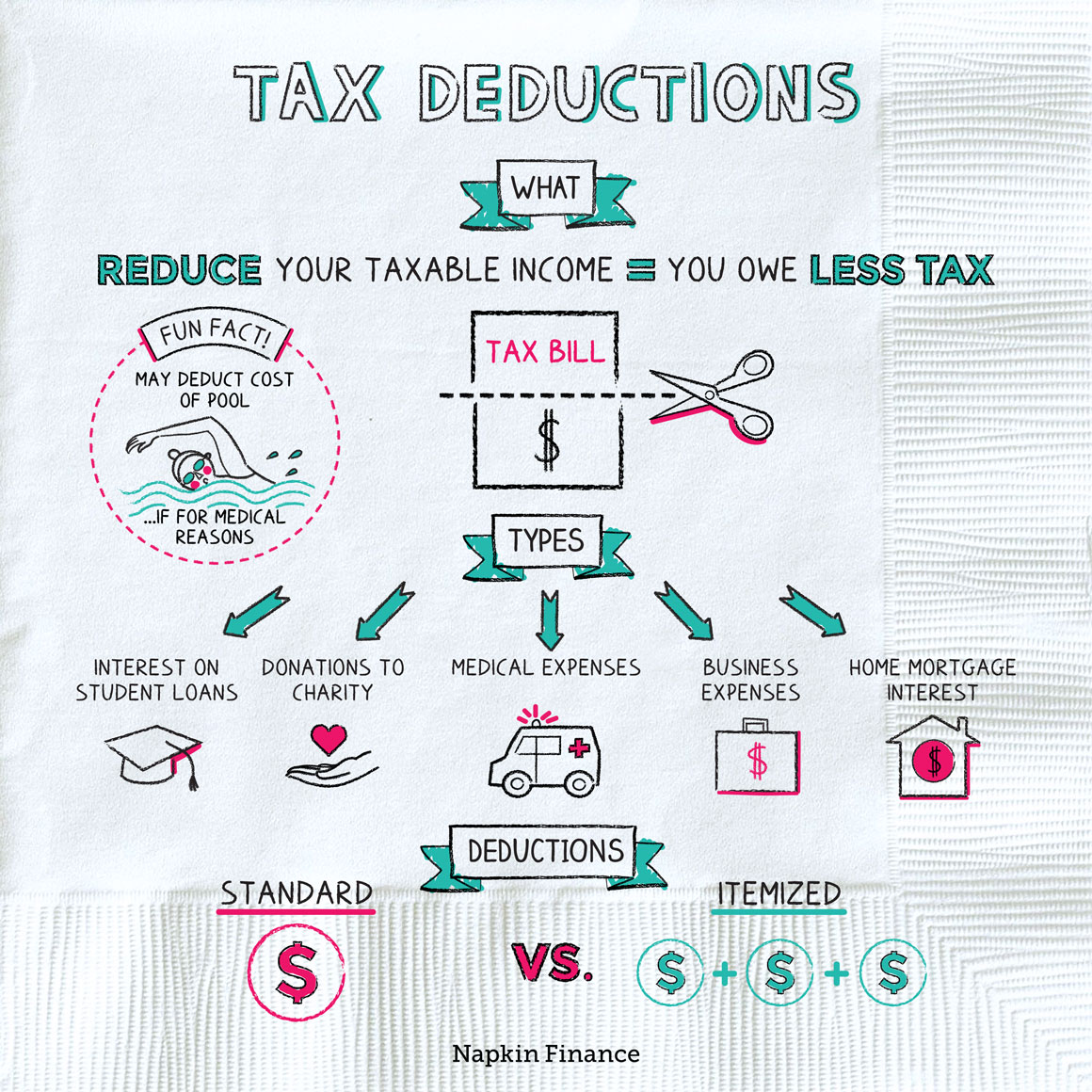

A tax deductible is an expense that the Internal Revenue Service (IRS) or relevant tax authority permits you to subtract from your total income to arrive at your adjusted gross income (AGI) or taxable income. These expenses are typically incurred in the process of earning income, making investments, or are specific costs the government incentivizes through tax breaks. The key is that these are not simply credits that reduce your tax bill dollar-for-dollar; instead, they reduce the base upon which your tax is calculated. For instance, if you earn $70,000 annually and have $10,000 in eligible tax deductions, your taxable income becomes $60,000, and you are taxed only on that lower amount.

How Deductibles Reduce Your Taxable Income

The mechanism is straightforward yet powerful. When you claim a deduction, it directly lowers your adjusted gross income (AGI). Your AGI is a crucial figure because it’s used to determine eligibility for various other tax credits and deductions. A lower AGI means a smaller portion of your income falls into higher tax brackets, potentially pushing you into a lower overall bracket and reducing the amount of tax you owe. The value of a deduction depends on your marginal tax rate. If you are in the 22% tax bracket, a $1,000 deduction saves you $220 in taxes (22% of $1,000). This demonstrates that the higher your tax bracket, the more significant the financial benefit of each dollar you deduct.

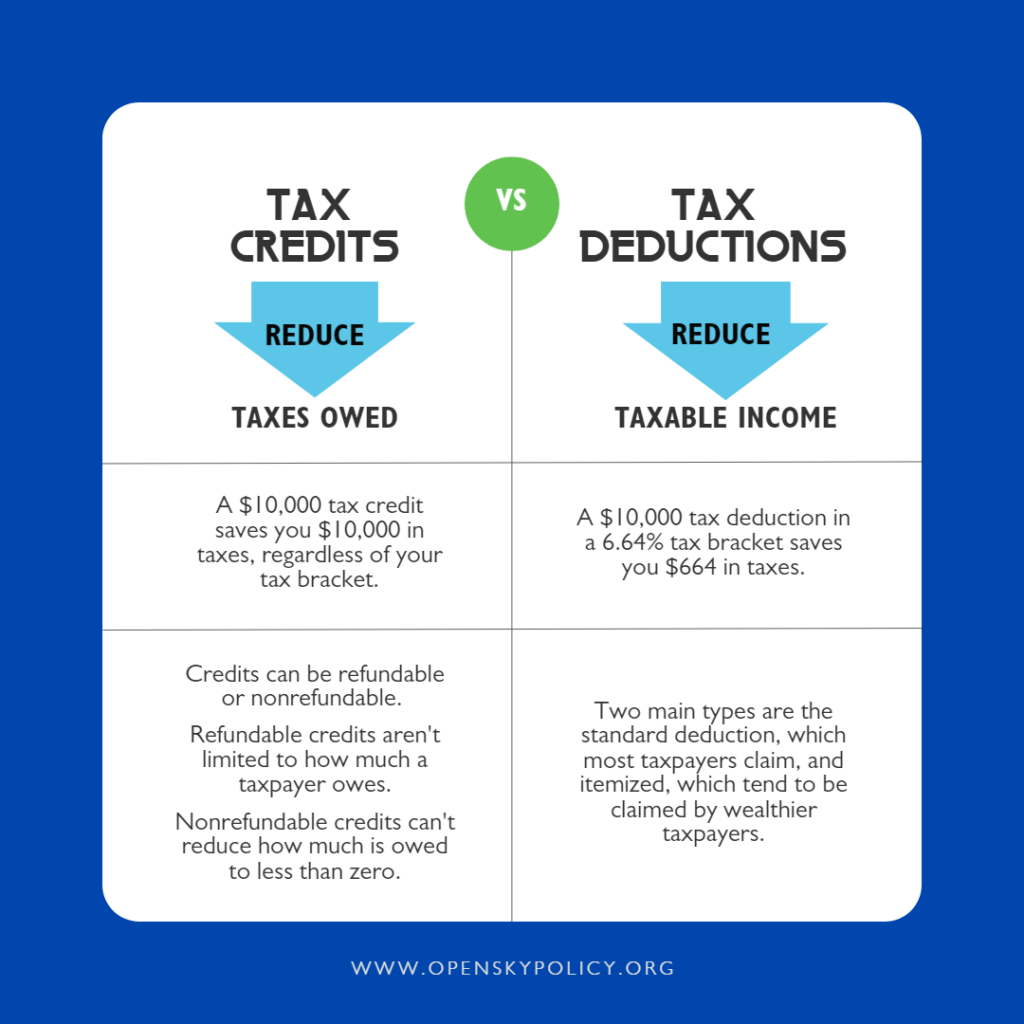

The Difference Between Deductions and Credits

It’s vital to distinguish between tax deductions and tax credits, as they serve different purposes and offer varying levels of savings.

- Tax Deductions reduce your taxable income. The amount of tax saved depends on your tax bracket. For example, a $1,000 deduction for someone in the 22% bracket saves $220.

- Tax Credits directly reduce the amount of tax you owe, dollar-for-dollar. A $1,000 tax credit reduces your tax bill by $1,000, regardless of your tax bracket. Some credits are even refundable, meaning you can get money back even if you owe no tax.

While both are valuable for tax savings, credits generally offer a more significant direct reduction in your tax bill. However, deductions are often more broadly available and can significantly impact your overall financial planning.

Common Categories of Individual Tax Deductibles

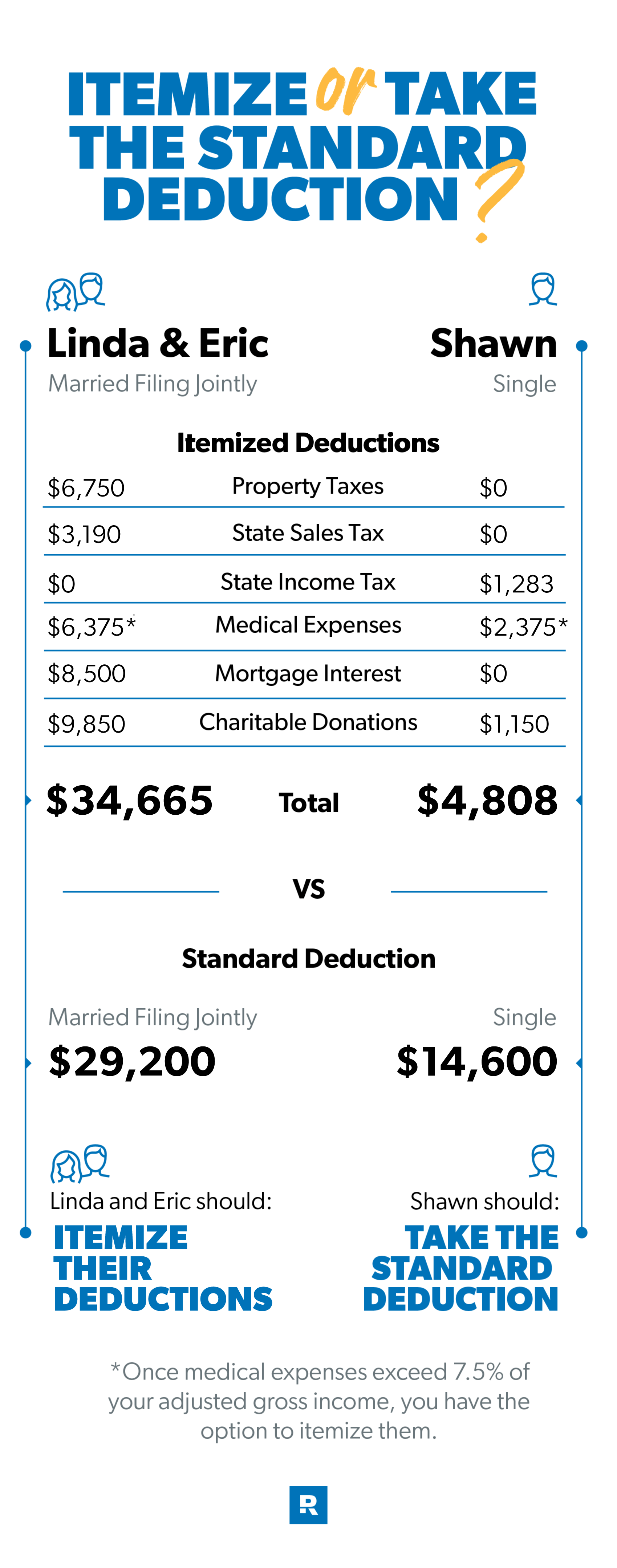

For individual taxpayers, deductibles typically fall into two main categories: the standard deduction or itemized deductions. Choosing which one to take can have a substantial impact on your tax liability.

Standard vs. Itemized Deductions

Every taxpayer has the option to take either the standard deduction or itemize their deductions.

- Standard Deduction: This is a fixed dollar amount set by the IRS that varies based on your filing status (e.g., single, married filing jointly, head of household). It simplifies tax filing for many, as it doesn’t require documenting specific expenses. For many taxpayers, the standard deduction is higher than their total itemized deductions.

- Itemized Deductions: This involves listing and totaling specific eligible expenses. You would choose to itemize if your total eligible expenses exceed the standard deduction amount for your filing status. Common itemized deductions include medical expenses, state and local taxes, mortgage interest, and charitable contributions.

Deciding between the standard and itemized deduction is a crucial step in tax preparation and depends entirely on your personal financial situation.

Medical and Dental Expenses

If your unreimbursed medical and dental expenses exceed a certain percentage of your Adjusted Gross Income (AGI) – for instance, 7.5% for the 2023 tax year – you can deduct the amount above that threshold. This includes payments for diagnosis, cure, mitigation, treatment, or prevention of disease, as well as for treatments affecting any structure or function of the body. Examples include doctor visits, hospital stays, prescription medications, dental work, vision care, and even certain travel expenses to receive medical care.

State and Local Taxes (SALT)

Taxpayers can deduct state and local income taxes, real estate taxes, and personal property taxes. However, the Tax Cuts and Jobs Act (TCJA) of 2017 imposed a cap of $10,000 on the total amount of SALT deductions that can be claimed per household ($5,000 for married individuals filing separately). This cap significantly impacted taxpayers in high-tax states.

Mortgage Interest

One of the most significant deductions for many homeowners is the interest paid on a mortgage. You can deduct interest on up to $750,000 ($375,000 if married filing separately) of qualified residence loan debt incurred after December 15, 2017. For debt incurred on or before that date, the limit is $1 million ($500,000 if married filing separately). This deduction applies to both a primary residence and a second home.

Charitable Contributions

Donations to qualified charitable organizations can be deducted. These can include cash contributions, goods, or even property. For cash contributions, you generally cannot deduct more than 60% of your AGI, though there are special rules and limits. Non-cash donations are typically valued at their fair market value, and specific rules apply to their deductibility. Proper documentation, such as receipts or acknowledgments from the charity, is essential.

Student Loan Interest and Education Expenses

If you paid interest on a qualified student loan, you might be able to deduct up to $2,500 of that interest, even if you don’t itemize your deductions. This is an “above-the-line” deduction, meaning it reduces your AGI directly. Additionally, certain education expenses, like tuition and fees for higher education, might qualify for various tax credits, which, as mentioned, are even more beneficial than deductions.

Retirement Plan Contributions

Contributions to traditional Individual Retirement Accounts (IRAs) and certain employer-sponsored retirement plans (like 401(k)s, 403(b)s, and SEP IRAs) are often tax-deductible. These deductions not only reduce your current taxable income but also help you save for retirement, offering a powerful dual benefit. The deductibility depends on your income level, filing status, and whether you or your spouse are covered by a retirement plan at work.

Tax Deductibles for Self-Employed Individuals and Businesses

Business owners and self-employed individuals have a broader array of deductible expenses, as almost any “ordinary and necessary” expense incurred in the course of business can be deducted. This distinction is crucial for understanding the true profitability of a venture.

Business Expenses (Office, Supplies, Travel)

For businesses, the range of deductible expenses is extensive. This includes costs such as office rent or mortgage interest, utilities, office supplies, internet and phone bills, software subscriptions, marketing and advertising costs, professional development and education, and vehicle expenses (either actual expenses or the standard mileage rate). Business travel expenses, including airfare, lodging, and 50% of the cost of business meals, are also generally deductible. The key is that these expenses must be both “ordinary” (common and accepted in your industry) and “necessary” (helpful and appropriate for your business).

Health Insurance Premiums

Self-employed individuals who pay for their own health insurance premiums can often deduct these costs. This is an “above-the-line” deduction, meaning it reduces your AGI, provided you are not eligible to participate in an employer-sponsored health plan (either through your own employment or a spouse’s).

Self-Employment Tax Deduction

Self-employed individuals pay both the employer and employee portions of Social Security and Medicare taxes, collectively known as self-employment tax. However, the IRS allows you to deduct one-half of your self-employment taxes paid from your gross income. This helps offset the additional tax burden faced by independent contractors and small business owners.

Home Office Deduction

If you use a portion of your home exclusively and regularly for your business, you may be able to claim a home office deduction. There are two methods: the simplified option (a flat rate per square foot of home office space, up to a maximum) or the regular method (calculating actual expenses, including a portion of utilities, insurance, depreciation, and mortgage interest/rent). Strict rules apply to this deduction, requiring clear separation of business and personal use of the space.

Depreciation of Assets

Businesses can deduct the cost of certain long-lasting assets (like equipment, machinery, and vehicles) over their “useful life” through a process called depreciation. Instead of deducting the entire cost in the year of purchase, the expense is spread out over several years. Special rules like Section 179 deduction and bonus depreciation allow businesses to deduct a significant portion or even the full cost of eligible assets in the year they are placed in service, providing an immediate tax break.

Strategies for Maximizing Your Tax Deductions

Maximizing your tax deductions requires proactive planning, diligent record-keeping, and an understanding of the ever-evolving tax landscape.

Maintaining Meticulous Records

The golden rule for tax deductions is documentation. The IRS requires proof for every deduction you claim. This means keeping clear, organized records of all relevant expenses, including receipts, invoices, bank statements, canceled checks, and mileage logs. Digital record-keeping solutions can be invaluable here, ensuring easy access and backup of critical financial data. Without proper documentation, a deduction may be disallowed during an audit, leading to penalties and back taxes.

Understanding Tax Law Changes

Tax laws are not static; they change frequently, sometimes annually. Staying informed about new legislation, expiring provisions, and updated limits is crucial for effective tax planning. Subscribing to financial news, following IRS updates, or working with a knowledgeable tax professional can help you adapt your strategy to the current tax environment.

Strategic Timing of Payments

Sometimes, the timing of when you incur or pay an expense can impact its deductibility in a given tax year. For instance, if you’re close to the end of the year and anticipate itemizing, prepaying certain deductible expenses (like property taxes or charitable contributions) before December 31st might allow you to claim them in the current year, potentially increasing your deductions. This strategy is often referred to as “tax-loss harvesting” or “bunching” deductions.

Consulting a Tax Professional

While understanding the basics is important, the complexities of tax law often warrant professional guidance. A qualified tax accountant or enrolled agent can provide personalized advice, identify deductions you might overlook, and ensure your tax strategy is optimized and compliant. Their expertise can be invaluable, especially for complex financial situations, self-employment, or significant life changes.

The Importance of Compliance and Avoiding Pitfalls

While maximizing deductions is a savvy financial move, it’s paramount to do so legally and ethically. Aggressive or unsubstantiated claims can lead to significant problems.

Accurate Reporting and Documentation

Every deduction claimed must be legitimate and substantiated by proper records. Misrepresenting expenses or claiming deductions for which you don’t qualify can result in an audit, penalties, and interest on underpaid taxes. Honesty and accuracy are non-negotiable.

The Risk of Audits

The IRS uses various methods to select returns for audit, including identifying unusually high deductions compared to income levels or industry norms. While most taxpayers will never face an audit, those who do must be prepared to provide comprehensive documentation to support every claim. A robust record-keeping system is your best defense.

When in Doubt, Seek Expert Advice

If you are ever unsure about the deductibility of an expense or the best way to report certain income, err on the side of caution and consult a tax professional. Their guidance can prevent costly mistakes and ensure peace of mind that your tax filings are accurate and fully compliant with the law.

In conclusion, tax deductibles are more than just a line item on a tax form; they are a powerful tool for financial optimization and a critical component of personal and business financial strategy. By diligently understanding, tracking, and appropriately claiming these eligible expenses, individuals and businesses can significantly reduce their taxable income, lowering their overall tax burden and freeing up capital for savings, investment, or other financial goals. With meticulous record-keeping, ongoing education, and professional guidance when needed, you can confidently navigate the tax landscape and harness the full potential of tax deductibles.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.