The housing market has undergone a seismic shift over the last few years, transitioning from the historic lows of the pandemic era to the highest interest rates seen in two decades. As we look toward 2025, both prospective homebuyers and seasoned real estate investors are asking the same critical question: where are mortgage rates headed? Understanding the trajectory of these rates is not merely a matter of curiosity; it is a fundamental component of financial planning, impacting everything from monthly household budgets to the long-term viability of investment portfolios.

Forecasts for 2025 suggest a landscape defined by “normalization.” While we are unlikely to see a return to the 3% rates that fueled the post-2020 housing boom, the consensus among economists points toward a gradual easing. Navigating this environment requires a deep dive into the macroeconomic levers moving the market and a strategic approach to personal finance.

The Macroeconomic Landscape: Factors Influencing 2025 Projections

Mortgage rates do not exist in a vacuum. They are the product of complex interactions between government policy, global economic health, and investor sentiment. To understand what 2025 holds, we must first analyze the primary drivers that dictate the cost of borrowing.

Federal Reserve Policy and the Interest Rate Cycle

While the Federal Reserve does not directly set mortgage rates, its influence is paramount. The federal funds rate—the rate at which banks lend to each other overnight—serves as the benchmark for the entire economy. Throughout 2023 and 2024, the Fed maintained a restrictive stance to combat persistent inflation.

As we move into 2025, the narrative is shifting from “rate hikes” to “rate cuts.” Economists expect that as inflation approaches the Fed’s 2% target, the central bank will continue to lower the federal funds rate. This downward pressure typically trickles down to the mortgage market, lowering the yields required by investors and, consequently, the interest rates offered to consumers.

Inflation Targets and the Consumer Price Index (CPI)

Inflation is the greatest enemy of fixed-income investments like mortgages. When inflation is high, the purchasing power of the future interest payments a lender receives is eroded. To compensate for this risk, lenders demand higher interest rates.

The outlook for 2025 hinges on the Consumer Price Index (CPI) remaining on a cooling trend. If inflation remains “sticky” or experiences a rebound due to geopolitical tensions or supply chain disruptions, mortgage rates may remain higher for longer. However, most financial models for 2025 assume a stabilized inflationary environment, which provides the necessary “breathing room” for mortgage rates to descend into a more manageable range.

The 10-Year Treasury Yield and the Spread

Historically, the 30-year fixed mortgage rate tracks the movement of the 10-year U.S. Treasury note very closely. Typically, there is a “spread” or gap of about 1.5 to 2 percentage points between the two. In recent years, this spread widened significantly due to market volatility and uncertainty.

In 2025, analysts expect this spread to compress as the market stabilizes. If the 10-year Treasury yield sits around 3.5% to 4%, and the spread returns to historical norms, we could see mortgage rates settle comfortably in the 5.5% to 6.2% range. This compression is a key factor that could make 2025 a more favorable year for borrowing than the previous two.

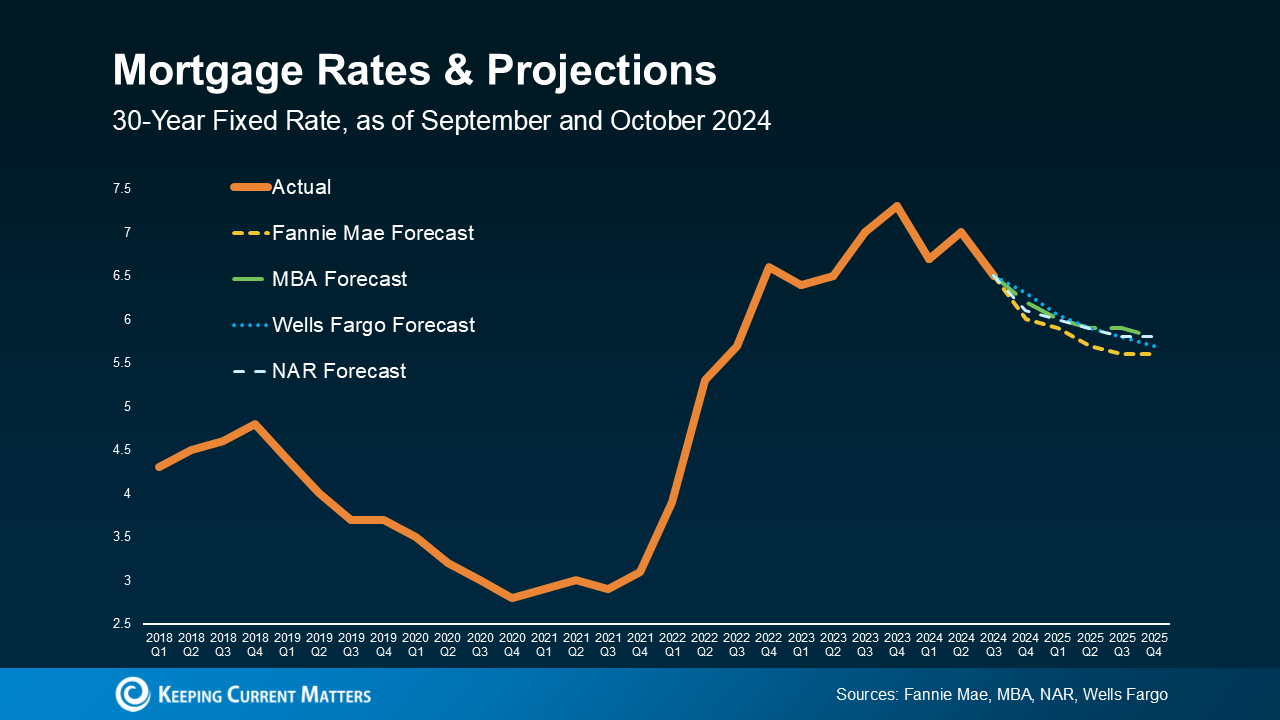

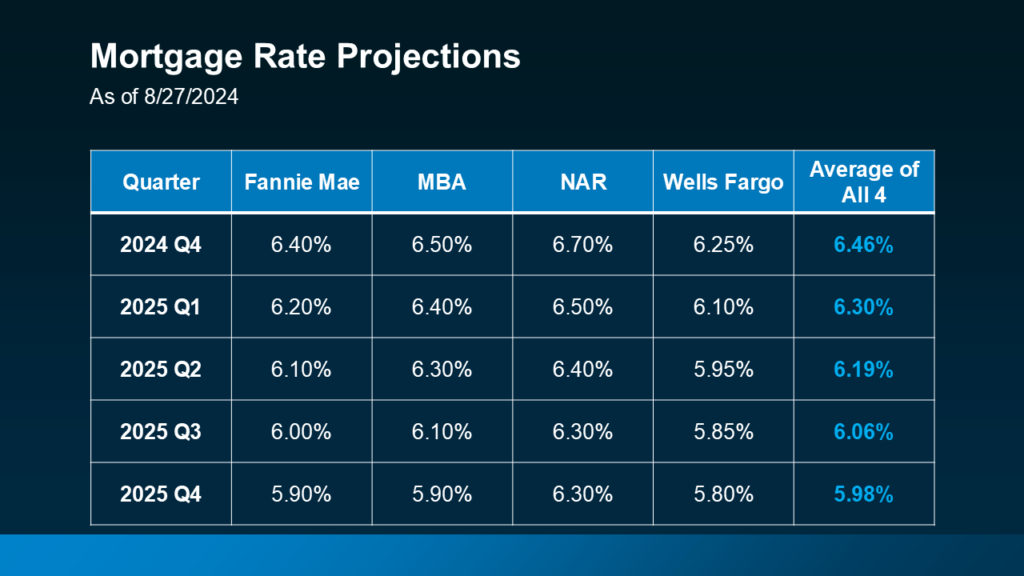

Expert Forecasts: Where Will Rates Land?

Major financial institutions and housing authorities—such as the Mortgage Bankers Association (MBA), Fannie Mae, and Freddie Mac—continuously update their projections. While their specific numbers vary, the general trend for 2025 is one of cautious optimism.

Analysis of MBA and Fannie Mae Projections

The Mortgage Bankers Association has been one of the more bullish organizations, projecting that rates could dip toward the high 5% range by mid-2025. Their reasoning is built on the expectation of a mild economic slowdown that forces the Fed to be more aggressive with rate cuts.

Conversely, Fannie Mae’s projections have been slightly more conservative, often placing the 2025 average in the low-to-mid 6% range. The difference between these forecasts often comes down to differing views on economic growth; higher growth usually means higher rates, while a slowing economy leads to lower borrowing costs. For the average consumer, these forecasts suggest that the days of 7.5% or 8% rates are likely behind us.

Why 5.5% to 6% is the New “Gold Standard”

It is essential for borrowers in 2025 to recalibrate their expectations. The era of 3% mortgages was an anomaly caused by a global crisis. In a healthy, functioning economy, a mortgage rate between 5.5% and 6.5% is actually quite low by historical standards.

Financial planners often refer to this as the “normalization” of the market. At 6%, a buyer still maintains significant purchasing power compared to the double-digit rates of the 1980s. For 2025, the “Gold Standard” for a “good” rate will likely be anything starting with a 5. This psychological threshold is expected to trigger a significant amount of “sideline” capital to enter the housing market.

Scenarios for a “Higher for Longer” Environment

While the consensus is a downward trend, a “Money” niche analysis must account for risk. There is a “Higher for Longer” scenario where rates stay above 6.5% throughout 2025. This could occur if the labor market remains unexpectedly tight, driving up wages and preventing inflation from hitting the 2% target. In this scenario, the Fed would be forced to keep interest rates elevated to prevent the economy from overheating, which would keep mortgage costs high for the foreseeable future.

Strategies for Homebuyers and Investors in 2025

With rates expected to fluctuate in a lower range, the strategy for 2025 shifts from “survival” to “optimization.” Whether you are looking for a primary residence or an investment property, your financial approach must be surgical.

Timing the Market vs. Time in the Market

A common mistake in personal finance is waiting for the absolute “bottom” of the rate cycle. If rates drop significantly in 2025, there will likely be a surge in buyer demand. This increased competition can drive home prices up, potentially offsetting any savings gained from a lower interest rate.

The mantra for 2025 should be: “Marry the house, date the rate.” If you find a property that fits your long-term needs and the math works at current rates, it may be wiser to purchase and plan for a refinance later. Trying to time the market perfectly often leads to missed opportunities as prices escalate.

Refinancing Opportunities in a Cooling Rate Environment

For those who purchased homes in 2023 or 2024 at rates of 7% or higher, 2025 could be the “Year of the Refinance.” A general rule of thumb in personal finance is that if you can lower your rate by 0.75% to 1%, a refinance is often worth the closing costs.

As rates potentially dip into the high 5s in 2025, millions of homeowners will enter the “refinance window.” This move can shave hundreds of dollars off monthly payments or allow homeowners to switch from a 30-year to a 15-year mortgage, significantly building equity faster and saving thousands in interest over the life of the loan.

The Impact on Real Estate Investment Portfolios

For investors, 2025 presents a different set of challenges. Lower rates improve “cash-on-cash” returns, making rental properties more attractive. However, lower rates also mean more competition from traditional homebuyers.

Investors in 2025 should focus on “value-add” opportunities—properties that need work but are in high-demand areas. By using 2025’s lower rates to secure financing, and then increasing the property’s value through renovations, investors can maximize their internal rate of return (IRR) regardless of minor fluctuations in the broader economy.

Navigating the 2025 Housing Market: Inventory and Affordability

Mortgage rates are only one side of the affordability coin. The other side is the supply of homes available for sale. In 2025, the relationship between rates and inventory will be the defining characteristic of the real estate market.

The “Lock-in Effect” and Its Potential Thaw

For the past two years, the market has suffered from the “lock-in effect.” Homeowners with 3% mortgages were unwilling to sell because they didn’t want to trade their low rate for a 7% rate. This effectively froze the inventory of existing homes.

As rates trend toward 5.5% or 6% in 2025, the “gap” between a homeowner’s current rate and a new rate narrows. This is expected to trigger a “thaw,” encouraging more people to list their homes. Increased inventory is good for buyers as it slows price appreciation and provides more choices, but it remains to be seen if the increase in supply will be enough to meet the pent-up demand.

Credit Score Management for Optimal Rates

In a 2025 market where every basis point counts, your personal financial health is your greatest asset. Mortgage lenders have tightened their standards, and the “best” rates—those touted in the headlines—are reserved for borrowers with top-tier credit scores (usually 760 or higher).

Prospective buyers in 2025 should focus on debt-to-income (DTI) ratios and credit utilization. Lowering high-interest consumer debt not only improves your credit score but also increases the amount of mortgage you can qualify for. In an environment where rates are settling into a new normal, being a “prime” borrower can save you tens of thousands of dollars over the duration of your mortgage.

Final Outlook: A Year of Transition

As we look toward 2025, the forecast for mortgage rates is one of stability and gradual improvement. We are moving away from the volatility of the post-pandemic recovery and toward a more sustainable economic equilibrium. While the days of “free money” are over, the projected rates for 2025 offer a much more hospitable environment for achieving the American dream of homeownership and for building wealth through real estate.

Success in the 2025 market will not come from luck, but from disciplined financial preparation. By understanding the macroeconomic forces at play, monitoring expert forecasts, and maintaining a high credit profile, you can position yourself to take full advantage of the shifting mortgage landscape. Whether you are buying, selling, or refinancing, 2025 promises to be a pivotal year in personal finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.