In the intricate landscape of personal finance and retirement planning, few instruments offer the unique blend of tax advantages and flexibility that a Roth IRA does. For many, the acronym IRA immediately conjures thoughts of deferred taxes and future security, but the “Roth” distinction introduces a powerful twist: tax-free growth and withdrawals in retirement. This article will demystify the Roth IRA, exploring its core mechanics, strategic benefits, and how it can serve as a cornerstone for a robust financial future. Whether you’re a seasoned investor or just beginning your savings journey, understanding the nuances of a Roth IRA is crucial for optimizing your long-term wealth accumulation.

Understanding the Roth IRA: A Foundation for Retirement Savings

At its heart, a Roth IRA is a specific type of individual retirement account that offers a distinct tax treatment compared to its traditional counterpart. It flips the script on conventional retirement savings, providing a powerful incentive for those who anticipate being in a higher tax bracket in retirement than they are today. This seemingly simple difference underpins a wealth of strategic planning opportunities that can significantly impact your financial well-being decades down the line.

Defining the Roth IRA: The Post-Tax Advantage

The fundamental characteristic of a Roth IRA is that contributions are made with after-tax dollars. This means that when you contribute to a Roth IRA, you don’t receive an immediate tax deduction in the year of the contribution, as you would with a traditional IRA. However, this upfront tax bite is a small price to pay for the tremendous benefit that follows: all qualified withdrawals in retirement are completely tax-free. This includes both your original contributions and all the earnings they’ve generated over the years. Imagine decades of compounding returns, completely untouched by the IRS when you finally access them. This tax-free withdrawal feature is the ultimate selling point and a powerful motivator for many investors.

How Roth IRAs Differ from Traditional IRAs

To truly appreciate the Roth IRA, it’s essential to understand its contrast with the traditional IRA. The core difference lies in the timing of the tax benefit.

- Traditional IRA: Contributions may be tax-deductible in the year they are made, leading to immediate tax savings. However, withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions are not tax-deductible. All qualified withdrawals in retirement are entirely tax-free.

This distinction creates a crucial decision point: do you want your tax break now (Traditional IRA) or later (Roth IRA)? The answer often depends on your current income level, your projected income level in retirement, and your overall tax strategy. If you believe your tax bracket will be higher in retirement, a Roth IRA is generally more advantageous. Conversely, if you expect to be in a lower tax bracket in retirement, a traditional IRA’s upfront deduction might be more appealing. Many financial planners advocate for a blended approach, utilizing both types of accounts to diversify tax risk.

Who Can Contribute? Income Limits and Eligibility

While the Roth IRA is undeniably appealing, it’s not universally accessible. The IRS imposes income limitations on who can directly contribute to a Roth IRA. These limits are adjusted annually for inflation. For instance, in a given year, if your modified adjusted gross income (MAGI) exceeds a certain threshold, your ability to contribute directly to a Roth IRA may be reduced or eliminated entirely.

- Full Contribution Eligibility: Individuals whose MAGI falls below a certain income level can contribute the maximum allowable amount.

- Partial Contribution Eligibility: As MAGI rises past the initial threshold, the amount you can contribute phases out.

- No Direct Contribution Eligibility: If your MAGI exceeds the upper threshold, you are generally not allowed to make direct contributions.

It’s important to note that even if you’re above the income limits for direct contributions, there’s a widely utilized strategy known as the “Backdoor Roth IRA.” This involves contributing to a non-deductible traditional IRA and then immediately converting those funds to a Roth IRA. While this bypasses the direct contribution limits, it comes with its own set of rules and considerations, particularly regarding the “pro-rata rule” if you hold other pre-tax IRA accounts.

The Mechanics of a Roth IRA: Contributions, Withdrawals, and Growth

Understanding the basic concept is only the first step; delving into the operational mechanics of a Roth IRA reveals its full potential and the rules governing its use. From how much you can put in to when and how you can take money out, these details are critical for effective financial planning.

Contribution Rules and Limits

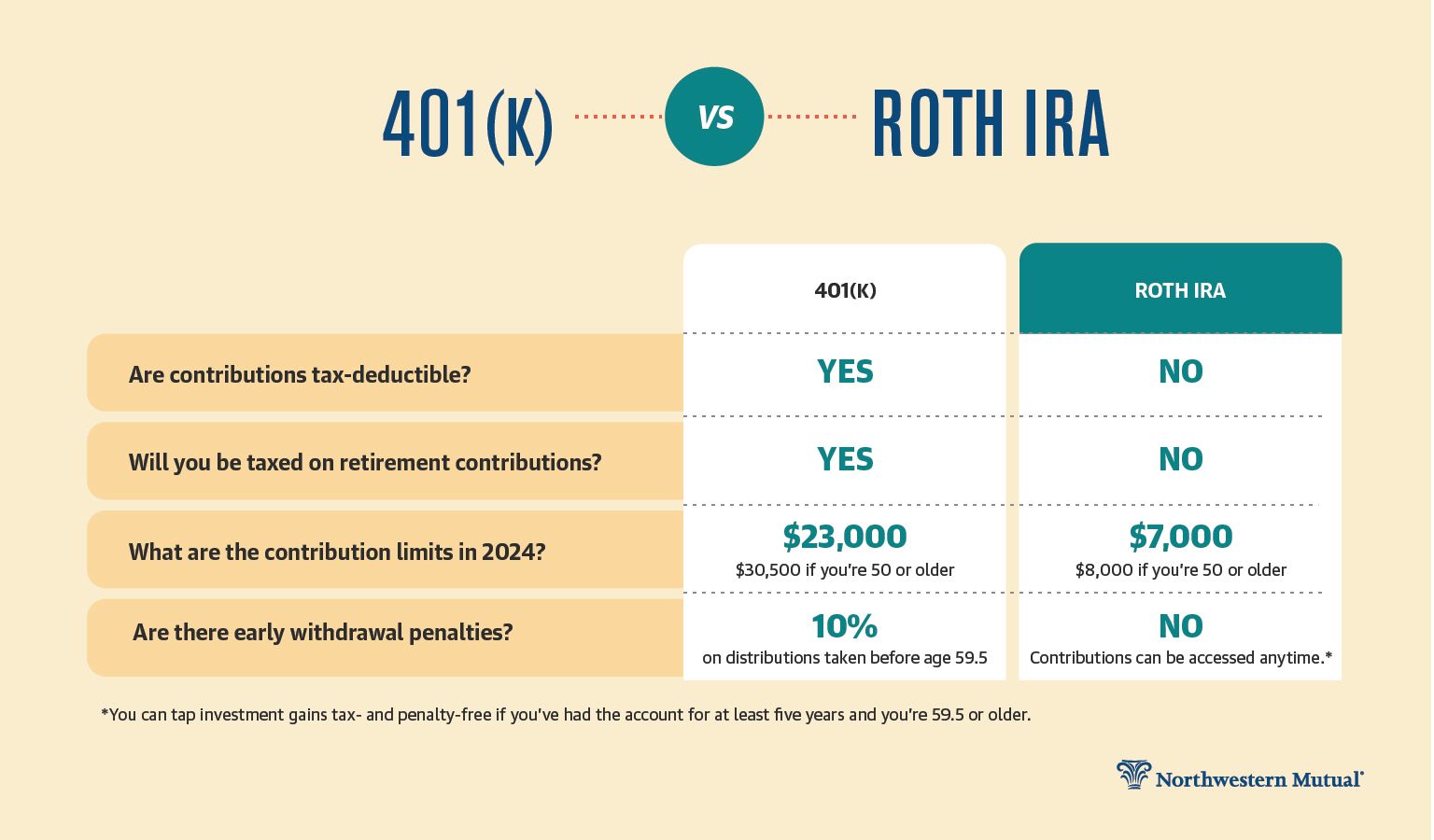

The IRS sets annual limits on how much an individual can contribute to an IRA (Roth or Traditional combined). These limits typically include a standard amount and an additional “catch-up” contribution for those aged 50 and over. These figures are subject to change annually, so staying updated on the current limits is essential. It’s also important to remember that contributions cannot exceed your earned income for the year. If you earn $5,000 in a year, you cannot contribute more than $5,000, even if the annual limit is higher. These contributions can be made up until the tax filing deadline of the following year (typically April 15th).

Qualified vs. Non-Qualified Withdrawals: The Tax-Free Promise

The tax-free nature of Roth IRA withdrawals is its most celebrated feature, but it comes with a critical condition: the withdrawal must be “qualified.” A qualified distribution meets two criteria:

- The Five-Year Rule: The Roth IRA must have been open for at least five years, starting from January 1st of the year you made your first contribution.

- A Qualifying Reason: You must meet one of the following conditions:

- You are age 59½ or older.

- You are disabled.

- You are using the funds for a qualified first-time home purchase (up to a lifetime limit).

- The distribution is made to your beneficiary after your death.

If a withdrawal is qualified, both your contributions and earnings are entirely tax-free and penalty-free.

The Five-Year Rule Explained

The five-year rule is often a point of confusion. It applies separately to contributions and conversions. For contributions, it means that even if you’re over 59½, you won’t enjoy tax-free earnings until five years have passed since your first Roth IRA contribution. If you contribute in January 2024, the five-year clock starts January 1, 2024, and the earliest you can take qualified withdrawals is January 1, 2029. This rule is crucial for planning when you might need to access funds.

Investment Options Within a Roth IRA

A Roth IRA is not an investment itself; rather, it is a type of account that holds investments. Inside your Roth IRA, you have a vast array of investment choices, similar to a traditional brokerage account. These typically include:

- Stocks: Individual company shares.

- Bonds: Government or corporate debt securities.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other investments.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but trade like stocks on an exchange.

- Certificates of Deposit (CDs): Time deposits offered by banks.

- Money Market Funds: Low-risk funds that invest in short-term debt securities.

The specific investments you choose will depend on your risk tolerance, financial goals, and investment horizon. The power of tax-free growth is amplified by wise investment choices that deliver strong returns over decades.

Strategic Benefits and Considerations of a Roth IRA

Beyond the basic mechanics, the Roth IRA offers several strategic advantages that make it a powerful tool for long-term wealth building and financial flexibility. These benefits extend beyond simple tax savings, influencing estate planning and income management in retirement.

Tax-Free Growth and Withdrawals in Retirement

This is the cornerstone benefit. Imagine investing $500,000 over your working life into a Roth IRA. If that money grows to $2 million by the time you retire, you could withdraw the entire $2 million without paying a single cent in federal income taxes (and likely state taxes, depending on your state). This complete tax exemption on earnings, especially when compounded over decades, is an unparalleled advantage compared to taxable brokerage accounts or even tax-deferred accounts like 401(k)s and traditional IRAs. It provides immense clarity and predictability regarding your retirement income.

Flexibility for Early Withdrawals (Penalty-Free, but Cautiously)

One often-overlooked feature of the Roth IRA is its surprising flexibility regarding early withdrawals. Since your contributions are made with after-tax dollars, you can withdraw your original contributions at any time, for any reason, without paying taxes or penalties. This acts as an emergency fund of last resort, offering a safety net without compromising your retirement savings goals if not strictly necessary.

However, it’s crucial to exercise caution. While penalty-free, withdrawing contributions diminishes your principal, thereby reducing the amount available for future tax-free growth. Accessing earnings before age 59½ or before the five-year rule is met typically incurs both income tax and a 10% early withdrawal penalty, unless an exception applies. Therefore, while flexible, a Roth IRA should primarily be viewed as a long-term retirement vehicle.

No Required Minimum Distributions (RMDs) for the Original Owner

Unlike traditional IRAs and 401(k)s, Roth IRAs do not require the original account owner to take Required Minimum Distributions (RMDs) during their lifetime. This is a significant advantage for those who may not need their Roth IRA funds immediately in retirement. It allows your money to continue growing tax-free for as long as you live, providing greater control over your retirement income stream and potentially reducing your taxable income in later years by delaying draws from other taxable accounts. This feature also makes Roth IRAs excellent vehicles for wealth transfer, as the account can continue to grow for beneficiaries.

Estate Planning Advantages

The absence of RMDs for the original owner, combined with the tax-free nature of qualified withdrawals, makes the Roth IRA an exceptionally powerful estate planning tool. If you pass away with Roth IRA assets, your beneficiaries can inherit the account and often continue to take tax-free withdrawals. This allows for a tax-efficient transfer of wealth to future generations. For non-spouse beneficiaries, the Secure Act mandates that the account be fully distributed within 10 years, but these distributions will still be tax-free if the original five-year rule was met by the original owner. This ability to pass on a tax-advantaged asset is a compelling reason for high-net-worth individuals to consider Roth contributions or conversions.

Is a Roth IRA Right for You? Key Decision Factors

Deciding whether a Roth IRA fits into your financial strategy requires a thoughtful evaluation of your current circumstances and future projections. There’s no one-size-fits-all answer, but by considering several key factors, you can make an informed decision that aligns with your long-term goals.

Current vs. Future Tax Brackets: A Crucial Calculation

The most significant factor in the Roth vs. Traditional IRA debate is your expectation of future tax rates.

- If you anticipate being in a higher tax bracket in retirement than you are today: A Roth IRA is generally more advantageous. You pay taxes now at a lower rate, securing tax-free income when your rates are higher. This is often the case for younger professionals just starting their careers, who expect their income and tax bracket to increase significantly over time.

- If you anticipate being in a lower tax bracket in retirement: A traditional IRA might be more beneficial. You get an upfront tax deduction when you’re in a higher bracket, and pay taxes on withdrawals when you’re in a lower bracket. This can be true for individuals nearing retirement whose income has peaked, or those who expect to live on a substantially reduced income in their golden years.

It’s important to remember that tax laws can change, making precise predictions difficult. Many investors mitigate this uncertainty by contributing to a mix of Roth and pre-tax accounts, thereby diversifying their tax risk.

Income Levels and Eligibility (Backdoor Roth Strategy)

As discussed, direct Roth IRA contributions are subject to income limitations. If your modified adjusted gross income (MAGI) exceeds these limits, you might still be able to contribute indirectly through a “Backdoor Roth IRA.” This strategy involves contributing after-tax money to a traditional IRA and then converting it to a Roth IRA. While seemingly straightforward, it requires careful execution, especially if you hold other pre-tax IRA accounts, due to the IRS’s “pro-rata” rule. Consulting with a financial advisor is highly recommended if you’re considering this strategy to avoid unintended tax consequences.

Roth IRA Conversion: A Path to Future Tax Freedom

Beyond direct contributions, existing pre-tax retirement accounts (like traditional IRAs or old 401(k)s) can be converted into a Roth IRA. This is known as a Roth conversion. When you convert, the amount converted from pre-tax funds is treated as taxable income in the year of conversion. This means you’ll pay taxes on that money upfront, but then it grows tax-free and can be withdrawn tax-free in retirement (provided the five-year rule for conversions is met, which is separate from the contribution rule).

Roth conversions are particularly appealing during periods of lower income or when you anticipate a significant increase in future tax rates. For example, if you retire early and have a few years of lower income before taking Social Security or a pension, that could be an opportune time to convert some traditional IRA funds to Roth.

Integrating a Roth IRA into Your Broader Financial Plan

A Roth IRA should not exist in isolation. It’s a component of a comprehensive financial plan that typically includes other retirement accounts (401(k), 403(b)), taxable investment accounts, emergency savings, and debt management.

- Diversify Tax Risk: By utilizing both pre-tax (e.g., traditional 401(k)/IRA) and after-tax (Roth) accounts, you create flexibility in retirement. You can strategically draw from different accounts to manage your taxable income in retirement, keeping you in lower tax brackets.

- Prioritize Contributions: For many, contributing enough to an employer-sponsored 401(k) to get the full company match is a top priority, as it’s “free money.” After that, funding a Roth IRA is often the next logical step, especially for those who anticipate higher future tax brackets.

- Consider Future Healthcare Costs: Tax-free Roth withdrawals can be incredibly valuable for covering healthcare expenses in retirement, which are often significant and unpredictable.

Setting Up and Managing Your Roth IRA

Establishing and managing a Roth IRA is a relatively straightforward process, but choosing the right custodian and understanding your investment options are key to maximizing its benefits.

Choosing a Custodian: Brokerage Firms and Investment Platforms

The first step is to open a Roth IRA account with a financial institution that acts as a custodian. Common options include:

- Online Brokerage Firms: Companies like Fidelity, Vanguard, Charles Schwab, and E*TRADE offer a wide range of investment options, competitive fees, and robust online platforms. They are popular choices for self-directed investors.

- Robo-Advisors: Services like Betterment or Wealthfront automate investment management based on your risk tolerance, making them suitable for those who prefer a hands-off approach.

- Traditional Banks or Credit Unions: While some offer IRAs, their investment options may be more limited, and fees potentially higher.

When choosing a custodian, consider factors such as investment selection, fees (trading commissions, expense ratios for funds, account maintenance fees), customer service, and the quality of their online tools and research.

Funding Your Account and Investment Selection

Once your account is open, you can begin funding it. This can typically be done via electronic transfers from your bank account, check deposits, or even direct deposit from your paycheck. After funding, you’ll need to select your investments.

- For self-directed investors: Research and choose individual stocks, ETFs, or mutual funds that align with your investment strategy. Many opt for low-cost index funds or target-date funds for broad diversification and simplicity.

- For those seeking guidance: Consider using a robo-advisor or working with a financial advisor who can help you select appropriate investments and manage your portfolio.

Regularly reviewing your investment performance and making adjustments as needed is crucial for long-term success.

Regular Contributions and Rebalancing

To truly leverage the power of a Roth IRA, consistent contributions are vital. Setting up automatic monthly or bi-weekly contributions can help you “set it and forget it,” ensuring you maximize your annual contribution limit and benefit from dollar-cost averaging.

Furthermore, it’s good practice to periodically rebalance your portfolio. Over time, some investments may grow faster than others, shifting your asset allocation away from your target. Rebalancing involves selling some of the overperforming assets and buying more of the underperforming ones to bring your portfolio back to your desired allocation, aligning with your risk tolerance and investment objectives.

In conclusion, the Roth IRA is a powerful and flexible retirement savings vehicle, celebrated for its tax-free withdrawals in retirement, absence of RMDs for the original owner, and surprising liquidity for contributions. While income limits and the five-year rule require careful consideration, its strategic advantages make it an indispensable tool for many seeking to build a secure and tax-efficient financial future. Understanding its intricacies and integrating it thoughtfully into your overall financial plan can significantly enhance your journey towards retirement independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.