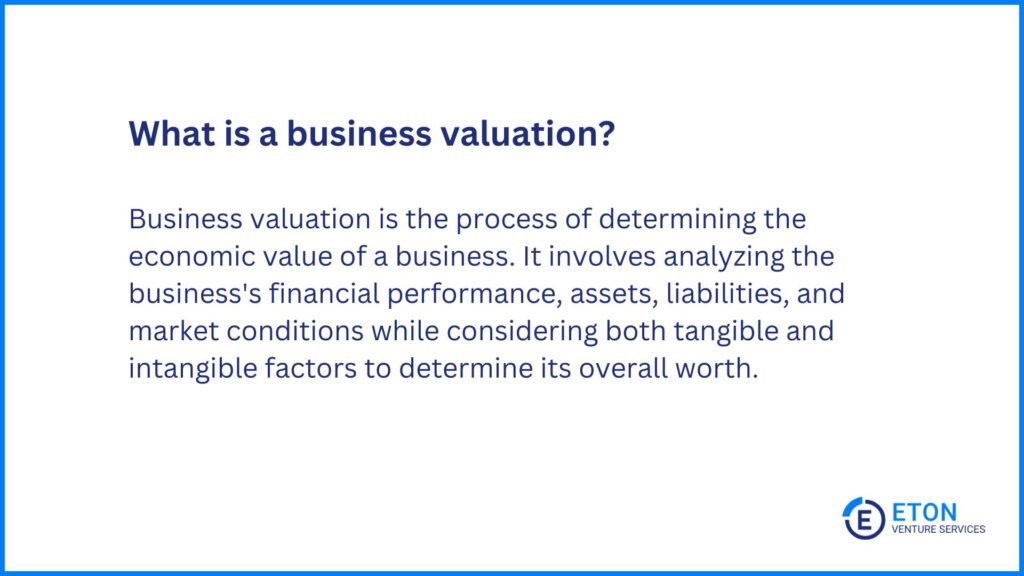

In the intricate world of finance, few concepts hold as much sway as “valuation.” Whether you’re an aspiring investor, a seasoned business owner, or simply curious about the economic engine that drives markets, understanding valuation is paramount. At its core, valuation is the process of determining the current worth of an asset or a company. It’s not merely a theoretical exercise; it’s a critical tool that underpins investment decisions, mergers and acquisitions, capital raising, financial reporting, and even personal financial planning. Without a robust framework for valuation, financial markets would operate in a fog of uncertainty, making informed decisions nearly impossible.

This comprehensive guide will demystify valuation, breaking down its fundamental principles, exploring key methodologies, identifying the myriad factors that influence it, and navigating the inherent challenges. Our goal is to equip you with an insightful understanding of how value is created, assessed, and ultimately realized in the financial landscape.

The Core Principles of Valuation

Before diving into the mechanics, it’s crucial to grasp the foundational principles that govern all valuation exercises. These principles provide the intellectual scaffolding upon which more complex models are built, ensuring a consistent and logical approach to determining worth.

Why Valuation Matters

The significance of valuation permeates almost every facet of finance and business. For investors, it’s the bedrock of making informed choices, helping them identify undervalued assets to buy and overvalued assets to sell. For businesses, valuation is essential for strategic planning, determining a fair price for an acquisition or sale, attracting investors for capital injections, and even for internal performance assessment. Banks use it to assess collateral for loans, while regulators often rely on it for financial reporting and compliance. Without a clear understanding of an asset’s or company’s value, stakeholders are left guessing, risking suboptimal decisions that can have far-reaching financial consequences. It acts as a compass, guiding capital to its most productive uses and ensuring market efficiency.

Intrinsic vs. Relative Value

A fundamental distinction in valuation lies between intrinsic value and relative value. Intrinsic value represents the true, underlying worth of an asset based on its fundamental characteristics, independent of market fluctuations or investor sentiment. It’s often derived from an analysis of future cash flows, growth prospects, risk profile, and tangible assets. The pursuit of intrinsic value is the holy grail for value investors, who believe that markets can, at times, misprice assets relative to their true worth.

In contrast, relative value assesses an asset’s worth by comparing it to similar assets or companies in the market. This approach relies on the principle that comparable assets should trade at comparable prices. Analysts use various multiples (e.g., price-to-earnings, enterprise value-to-EBITDA) to gauge whether an asset is cheap or expensive relative to its peers. While simpler and market-driven, relative valuation is susceptible to overall market sentiment; if the entire sector is overvalued, a relatively cheap asset within that sector might still be intrinsically overpriced. Both approaches have their merits and are often used in conjunction to provide a holistic view.

The Role of Risk and Return

At the heart of all financial decisions, and especially valuation, lies the inseparable relationship between risk and return. Investors demand a higher return for taking on greater risk. Consequently, an asset’s expected future cash flows must be discounted back to the present at a rate that reflects the inherent risks associated with realizing those cash flows. This discount rate is a critical input in valuation models. A higher perceived risk (e.g., volatile market, uncertain economic outlook, unstable management) will necessitate a higher discount rate, which in turn leads to a lower present value or valuation. Conversely, an asset with stable, predictable cash flows and lower risk will command a lower discount rate and, consequently, a higher valuation. Understanding and accurately quantifying risk—whether it’s market risk, operational risk, financial risk, or regulatory risk—is therefore indispensable for arriving at a realistic and defensible valuation.

Key Valuation Methodologies

The journey to determine an asset’s worth involves traversing various analytical paths. While the goal remains the same—to estimate value—the methodologies employed differ significantly in their approach, data requirements, and applicability. Mastering these techniques is crucial for anyone engaging in serious financial analysis.

Discounted Cash Flow (DCF) Analysis

Often considered the gold standard of intrinsic valuation, Discounted Cash Flow (DCF) analysis posits that the value of a business is the present value of its future free cash flows, discounted at an appropriate rate that reflects the risk of those cash flows. The process typically involves several steps:

- Projecting Free Cash Flows (FCF): Forecasting the cash generated by the business after accounting for operating expenses and capital expenditures over a explicit forecast period (e.g., 5-10 years).

- Determining the Discount Rate: Calculating the Weighted Average Cost of Capital (WACC), which represents the average rate of return a company expects to pay to all its security holders (debt and equity).

- Estimating Terminal Value: Calculating the value of the company’s cash flows beyond the explicit forecast period, assuming it grows at a constant, sustainable rate into perpetuity. This often accounts for a significant portion of the total value.

- Discounting and Summing: Discounting all projected FCFs and the Terminal Value back to the present using the WACC.

DCF is powerful because it’s forward-looking and based on fundamental economics. However, it’s highly sensitive to assumptions (growth rates, margins, discount rate, terminal growth rate), making it prone to “garbage in, garbage out” if inputs are not meticulously researched and justified.

Comparable Company Analysis (CCA) / Multiples Valuation

Comparable Company Analysis (CCA), also known as “multiples valuation” or “relative valuation,” assesses a company’s worth by comparing it to publicly traded companies in the same industry with similar characteristics. This method assumes that similar businesses should trade at similar valuations. The process involves:

- Identifying a Peer Group: Selecting publicly traded companies that are similar in terms of industry, size, growth prospects, and business model.

- Calculating Key Valuation Multiples: Computing metrics like Price-to-Earnings (P/E), Enterprise Value-to-EBITDA (EV/EBITDA), Price-to-Sales (P/S), or Price-to-Book (P/B) for the comparable companies.

- Applying Multiples to the Target Company: Taking the average or median multiple from the peer group and applying it to the target company’s corresponding financial metric to arrive at an implied valuation.

CCA is popular for its simplicity and market relevance, reflecting current market sentiment. However, finding truly “comparable” companies can be challenging, and market multiples can be distorted by irrational exuberance or pessimism. It offers a snapshot rather than a deep dive into intrinsic value.

Precedent Transactions Analysis

Precedent Transactions Analysis (or “transaction comps”) determines a company’s value by looking at prices paid for similar companies in past merger and acquisition (M&A) deals. The logic is that recent transactions involving similar companies provide a good benchmark for what a buyer might be willing to pay today. This methodology involves:

- Searching for Relevant Transactions: Identifying M&A deals involving companies similar in industry, size, and other characteristics to the target company.

- Analyzing Transaction Multiples: Calculating the implied valuation multiples (e.g., EV/EBITDA, EV/Sales) paid in those previous deals. Note that these multiples often include a control premium, reflecting the extra price paid for acquiring a controlling stake.

- Applying Multiples to the Target: Applying the observed transaction multiples to the target company’s financial metrics to derive an estimated valuation range.

Precedent transactions are valuable because they reflect actual prices paid and incorporate control premiums. However, they can be historical and not always representative of current market conditions, and unique deal-specific factors (synergies, strategic motivations) can skew the multiples, making direct comparability difficult.

Asset-Based Valuation

Asset-Based Valuation determines a company’s value by summing the fair market value of its individual assets and subtracting its liabilities. This method is particularly relevant for companies with significant tangible assets, such as manufacturing firms, real estate companies, or for businesses nearing liquidation. It can also be used as a floor for valuation in other methods. Approaches include:

- Liquidation Value: Estimating the net cash that would be realized if the company’s assets were sold off quickly and liabilities paid.

- Book Value: The value of assets as recorded on the balance sheet, often not reflective of market value.

- Adjusted Book Value: Modifying book values to reflect current market values for assets and liabilities.

While straightforward for asset-heavy businesses, this method struggles with valuing intangible assets (brands, intellectual property, customer relationships) which can represent a significant portion of a modern company’s value. It also doesn’t account for a company’s ability to generate future earnings or cash flows.

Factors Influencing Valuation

Valuation is rarely a static figure; it’s a dynamic assessment influenced by a multitude of internal and external forces. A thorough valuation considers not just the company’s internal financials but also the broader economic and market landscape in which it operates.

Macroeconomic Environment

The prevailing macroeconomic conditions cast a long shadow over valuation. Factors like interest rates are critical; higher rates increase the cost of capital, making future cash flows less valuable when discounted. Inflation erodes purchasing power and can impact input costs and pricing power. Economic growth directly influences consumer spending, business investment, and overall demand, thereby affecting a company’s revenue and profit projections. Geopolitical stability, regulatory changes, and government fiscal and monetary policies also play significant roles. A robust economy generally fosters higher valuations, while an economic downturn or recession typically leads to downward revisions.

Industry-Specific Dynamics

Beyond the broad economy, the specific industry in which a company operates is a major valuation determinant. Industries with high growth rates (e.g., technology, renewable energy) often command higher multiples due to their future potential. The level of competition within an industry dictates pricing power and profit margins; highly fragmented or commodity-based industries tend to have lower valuations. Regulatory landscape and technological disruption can create barriers to entry or render existing business models obsolete, significantly impacting long-term prospects. Understanding industry trends, competitive intensity, and the maturity of the sector is vital for a realistic valuation.

Company-Specific Attributes

Perhaps the most direct influences on a company’s valuation are its intrinsic characteristics. The quality of management and their strategic vision can unlock significant value or destroy it. A strong competitive advantage (e.g., proprietary technology, strong brand, network effects, cost leadership) allows a company to sustain profitability and market share. Future growth prospects and the predictability of those growth rates are fundamental drivers. Furthermore, the company’s financial health—its balance sheet strength, profitability margins, cash flow generation, and debt levels—directly impacts its risk profile and ability to fund future expansion, all of which feed into its valuation.

Market Sentiment and Liquidity

Even with rigorous financial analysis, market forces can significantly influence how a company is valued. Market sentiment, or the overall psychological mood of investors, can lead to periods of irrational exuberance or excessive pessimism. During bull markets, investors might pay higher multiples for growth, while bear markets tend to suppress valuations. Liquidity also plays a role; publicly traded companies with high trading volumes often command higher valuations than illiquid private companies, simply because their shares can be bought and sold more easily. While fundamental analysis aims for intrinsic value, acknowledging the impact of market sentiment and liquidity provides a more pragmatic and complete picture of market valuation.

Challenges and Best Practices in Valuation

Valuation, while grounded in financial principles, is as much an art as it is a science. It involves making numerous assumptions about an uncertain future, which introduces inherent challenges and necessitates adherence to best practices to minimize errors and biases.

The Art and Science of Valuation

The “science” of valuation lies in its mathematical models, financial statements analysis, and systematic application of methodologies. It involves crunching numbers, understanding accounting principles, and applying discount rates. However, the “art” emerges in the judgment required for selecting appropriate comparables, making reasonable assumptions about future growth rates, forecasting discretionary capital expenditures, and estimating the terminal growth rate. It demands critical thinking, industry knowledge, and an understanding of qualitative factors that don’t always fit neatly into a spreadsheet. The subjective nature of these inputs means that two equally competent analysts might arrive at slightly different valuation figures, underscoring that valuation is a range, not a single precise number.

Common Pitfalls to Avoid

Navigating the valuation landscape requires vigilance against common traps. One significant pitfall is over-optimism in forecasting growth and profitability, which can inflate valuations unrealistically. Conversely, excessive pessimism can lead to undervaluation. Cherry-picking comparables—selecting only those peer companies that support a desired valuation outcome—is another dangerous bias. Over-reliance on a single valuation method can also be misleading; a holistic approach using multiple methods (e.g., DCF, CCA, and Precedent Transactions) provides a more robust and defensible range. Neglecting to account for dilution from future equity issuance or the impact of off-balance-sheet liabilities can also lead to skewed results.

The Importance of Sensitivity Analysis

Given the inherent uncertainty in forecasting future variables, sensitivity analysis is an indispensable best practice. This involves systematically changing key input assumptions (e.g., revenue growth rate, operating margins, discount rate, terminal growth rate) to see how the valuation changes. By creating a range of scenarios—base case, optimistic case, and pessimistic case—analysts can understand the sensitivity of their valuation to different outcomes. This provides a more realistic understanding of the potential valuation range and helps investors assess the risks associated with their assumptions. It transforms a single point estimate into a more informative spectrum of possible values.

Continuous Learning and Adaptation

The financial markets are constantly evolving, driven by technological advancements, shifts in consumer behavior, regulatory changes, and geopolitical events. Therefore, valuation is not a one-time exercise but an ongoing process that demands continuous learning and adaptation. New business models, such as those prevalent in the tech sector, might require bespoke valuation approaches that go beyond traditional metrics. The rise of ESG (Environmental, Social, and Governance) factors, for instance, is increasingly influencing investor perception and, consequently, valuation. Staying abreast of industry trends, economic shifts, and evolving financial theory ensures that valuation methodologies remain relevant, accurate, and truly insightful.

Conclusion

Valuation is more than just a numerical calculation; it is a profound journey into understanding the true economic potential and inherent risks of an asset or a business. From the foundational principles of intrinsic versus relative value to the sophisticated mechanics of DCF and multiples analysis, each aspect plays a crucial role in forming a coherent picture of worth. While influenced by a myriad of factors—from the global economy to the specific strengths of a management team—valuation ultimately boils down to a well-reasoned estimate of future cash flows and their present value.

Mastering valuation requires diligence, critical thinking, and a disciplined approach to assumptions. It is a vital skill for investors seeking to identify opportunities, for entrepreneurs aiming to raise capital, and for anyone looking to make sound financial decisions. By embracing its complexities, acknowledging its inherent subjectivity, and employing a multi-faceted approach, you can unlock deeper insights into the financial world and navigate it with greater confidence and success. Ultimately, understanding “what’s valuation” is understanding the very language of financial opportunity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.