The question of when mortgage rates will finally trend downward has become a central focus for prospective homebuyers, real estate investors, and current homeowners looking to refinance. After nearly a decade of historically low borrowing costs, the rapid ascent of interest rates in recent years has fundamentally altered the landscape of personal finance and real estate. Understanding the trajectory of mortgage rates requires a deep dive into the macroeconomic machinery that governs the cost of capital, from the Federal Reserve’s monetary policy to the volatility of the bond market.

While no economist possesses a crystal ball, a careful analysis of current financial data and inflationary trends provides a roadmap for what to expect in the coming months and years. This article explores the mechanics behind interest rate fluctuations and offers a strategic outlook on when the market might finally see relief.

The Current State of the Mortgage Market: Understanding the High-Rate Environment

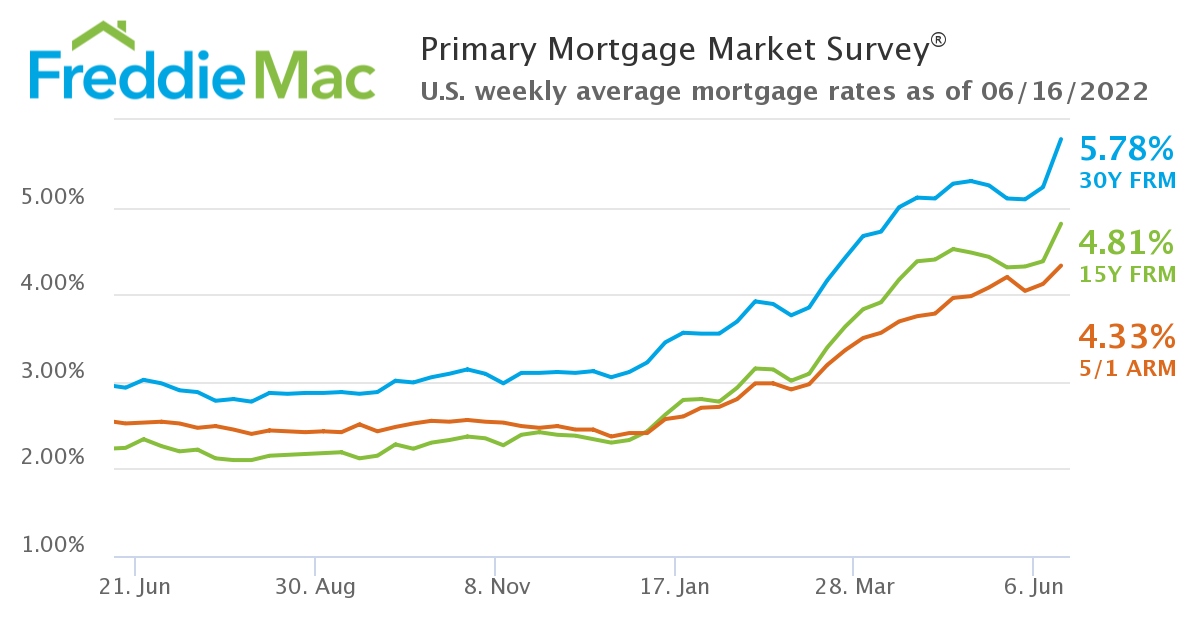

To understand when rates will go down, one must first understand why they went up. The era of the “3% mortgage” was an anomaly born of the global pandemic and the massive liquidity injected into the financial system to prevent an economic collapse. As the economy reopened, this surge in demand, coupled with supply chain disruptions, led to the highest inflation seen in four decades.

The Federal Reserve’s Aggressive Tightening Cycle

The primary driver of the recent surge in mortgage rates has been the Federal Reserve’s campaign to combat inflation. By raising the federal funds rate—the overnight lending rate between banks—the Fed effectively increased the cost of borrowing across the entire economy. While the Fed does not directly set mortgage rates, their actions dictate the baseline for all consumer debt.

The Spread Between the 10-Year Treasury and Mortgage Rates

Historically, the interest rate on a 30-year fixed-rate mortgage tracks the yield on the 10-year U.S. Treasury note, typically with a “spread” or gap of about 150 to 200 basis points (1.5% to 2%). Recently, this spread has widened significantly, sometimes exceeding 300 basis points. This widening is a reflection of market volatility and uncertainty. Investors in mortgage-backed securities (MBS) demand a higher premium to compensate for the risk of rapid fluctuations in the market.

Key Economic Indicators: What Moves the Needle on Mortgage Rates?

Mortgage rates do not move in a vacuum. They are highly sensitive to several specific economic indicators that signal the health of the U.S. economy and the future direction of inflation.

Inflation and the Consumer Price Index (CPI)

Inflation is the “arch-nemesis” of fixed-income investments like mortgages. When inflation is high, the purchasing power of the future interest payments a lender receives is eroded. Therefore, when CPI data shows that inflation is cooling, mortgage rates typically respond by moving lower. The Federal Reserve has a stated target of 2% inflation; until the market sees consistent evidence that inflation is sustainably heading toward that goal, mortgage rates are likely to remain elevated.

The Labor Market and Unemployment Data

A “hot” labor market is often a double-edged sword. While low unemployment is generally good for the economy, it can lead to wage-push inflation. If the monthly jobs report shows robust hiring and significant wage growth, the Federal Reserve is more likely to keep interest rates higher for longer to prevent the economy from overheating. Conversely, a cooling labor market often signals that the Fed can begin to ease its restrictive policy, which would lead to a decline in mortgage rates.

The Role of Mortgage-Backed Securities (MBS)

Most mortgages are bundled into securities and sold to investors. The demand for these securities plays a critical role in determining the rates offered to consumers. When the Federal Reserve was “tapering” its balance sheet—meaning it stopped buying mortgage-backed securities—it removed a major buyer from the market, which naturally pushed yields (and mortgage rates) higher. For rates to drop significantly, we need to see renewed investor appetite for these bonds.

Expert Forecasts: When Can We Expect a Meaningful Decline?

Economists from major financial institutions and housing organizations, such as Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Realtors (NAR), have been closely monitoring the situation to project a timeline for rate relief.

The “Higher for Longer” Narrative in 2024

Throughout much of 2024, the prevailing sentiment has been one of cautious patience. While many initially expected rates to drop early in the year, sticky inflation data forced a pivot in expectations. Current forecasts suggest that while we may see incremental decreases toward the end of the year, a return to the 5% range is more likely a story for late 2025 or beyond.

Projections for 2025 and 2026

Most industry experts agree that the peak of mortgage rates is likely behind us. As the effects of the Fed’s previous rate hikes continue to permeate the economy, growth is expected to slow, and inflation is projected to settle closer to the 2% target. Financial models suggest a gradual “staircase” decline. We may see rates stabilize in the low 6% range before potentially dipping into the high 5% range as the market gains confidence in the long-term economic stability.

Factors That Could Accelerate the Decline

There are “black swan” events or specific economic shifts that could cause mortgage rates to drop faster than anticipated. A significant recession, for instance, would force the Federal Reserve to cut rates aggressively to stimulate the economy. Additionally, if the geopolitical landscape stabilizes and global energy prices drop, inflation could fall faster than expected, providing the necessary room for mortgage rates to retreat.

Strategic Financial Planning: Navigating the Market While Rates Are High

For those currently in the market for a home or considering a move, waiting for the “perfect” rate can be a risky strategy. Financial planning in a high-rate environment requires a more nuanced approach than simply looking at the headline interest rate.

The Concept of “Marrying the House, Dating the Rate”

This popular real estate adage suggests that buyers should focus on finding the right property at the right price today, with the intention of refinancing in the future when rates eventually drop. The logic is that if you wait for rates to fall, you may face increased competition and higher home prices, as lower rates typically bring more buyers back into the market, driving up demand.

Improving Your Financial Profile

Regardless of the national average, your personal mortgage rate is determined by your creditworthiness. While waiting for the market to shift, focus on:

- Credit Score Optimization: Even a 20-point increase in your credit score can move you into a different pricing tier, potentially saving you thousands of dollars over the life of the loan.

- Debt-to-Income (DTI) Ratio: Paying down existing high-interest debt, such as credit cards, improves your DTI and makes you a more attractive borrower.

- Increasing the Down Payment: A larger down payment reduces the lender’s risk and can sometimes help you secure a lower interest rate or eliminate the need for Private Mortgage Insurance (PMI).

Considering Alternative Loan Products

In a high-rate environment, fixed-rate 30-year mortgages aren’t the only option. Adjustable-Rate Mortgages (ARMs) have regained popularity. These loans typically offer a lower initial interest rate for a set period (such as 5, 7, or 10 years). For buyers who plan to move or refinance before the adjustment period begins, an ARM can be a strategic tool to manage monthly costs in the short term.

The Long-Term Outlook: Will We Ever See 3% Again?

It is essential to maintain a historical perspective when discussing mortgage rates. The sub-3% rates seen in 2020 and 2021 were a historical anomaly, fueled by unprecedented government intervention. Looking back at the last 50 years, the average mortgage rate in the United States has hovered around 7.7%.

The New Normal for Mortgage Rates

Most financial analysts believe that we are entering a “new normal” where mortgage rates will likely settle between 5.5% and 6.5%. While this feels high compared to the recent past, it is actually quite moderate in a historical context. A return to 3% would likely require a severe economic crisis, which is an event most would prefer to avoid.

The Impact on Housing Inventory and Prices

One of the reasons mortgage rates are so impactful right now is the “lock-in effect.” Many current homeowners have mortgages at 3% or 4% and are reluctant to sell and move into a new home with a 7% rate. This has kept housing inventory low, which in turn has kept home prices high. As rates begin to drift down toward the 5% mark, many experts believe this will unlock a significant amount of inventory, potentially normalizing the housing market and providing more options for buyers.

![]()

Conclusion: Patience and Preparation

In summary, while mortgage rates are expected to trend downward, the decline will likely be gradual rather than immediate. The timeline is heavily dependent on inflation data and the Federal Reserve’s response to a changing economic landscape. For those in the world of personal finance and investing, the best course of action is not to try and “time” the market perfectly, but rather to prepare your finances so that you are ready to act when the right opportunity—and a slightly better rate—presents itself. Understanding that the days of ultra-cheap debt are likely over allows for more realistic and robust long-term financial planning.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.