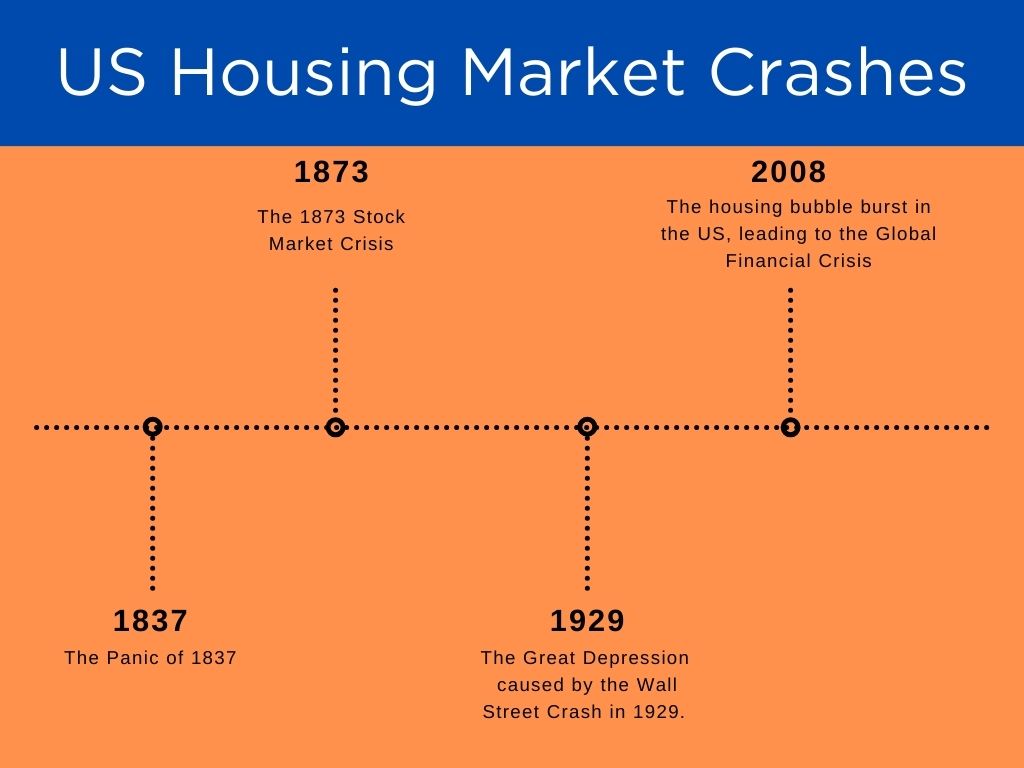

The question “what year did the housing market crash?” often refers to the severe economic downturn that began to manifest in the United States around 2008, culminating in what is now known as the Great Recession. While signs of distress appeared earlier, particularly in the subprime mortgage market in 2006-2007, 2008 was the year the crisis fully erupted and sent shockwaves through the global financial system. This wasn’t merely a dip in housing prices; it was a catastrophic failure rooted in years of predatory lending, unchecked financial innovation, and a widespread belief that housing prices would only ever go up. Understanding this pivotal moment is crucial for anyone involved in personal finance, investing, or comprehending the intricate workings of the modern economy.

The Anatomy of the 2008 Housing Market Crash

To truly grasp the 2008 crisis, one must dissect the complex factors that converged to create the perfect storm. It wasn’t a single cause but a perilous cocktail of loose lending practices, speculative fervor, and opaque financial engineering that ultimately destabilized the entire system.

The Subprime Mortgage Crisis: A Ticking Time Bomb

At the heart of the crisis was the proliferation of subprime mortgages. These were home loans offered to borrowers with poor credit histories, low incomes, or high debt-to-income ratios – individuals who would not qualify for conventional prime loans. Lenders, driven by the promise of high returns and enabled by a lax regulatory environment, aggressively marketed these loans. Many of these mortgages featured “teaser rates” – artificially low initial interest rates that reset after a few years to much higher, unaffordable levels. When these rates adjusted, millions of homeowners found their monthly payments skyrocketing beyond their means, leading to a wave of defaults and foreclosures. This widespread failure of subprime borrowers to meet their obligations was the initial crack in the foundation.

Securitization and Derivatives: Spreading the Risk

The danger of subprime mortgages was amplified by complex financial instruments. Investment banks bundled thousands of these mortgages into securities called Mortgage-Backed Securities (MBS). These MBS were then further sliced and repackaged into even more complex products known as Collateralized Debt Obligations (CDOs). The idea was to diversify risk by pooling different mortgages, but in reality, it spread the risk of inherently flawed subprime loans across the global financial system. Rating agencies, often incentivized by the very banks creating these products, gave these risky securities top credit ratings, misleading investors into believing they were safe. When the underlying mortgages started to default, the value of MBS and CDOs plummeted, leaving financial institutions around the world holding trillions of dollars in essentially worthless assets.

The Housing Bubble Bursts

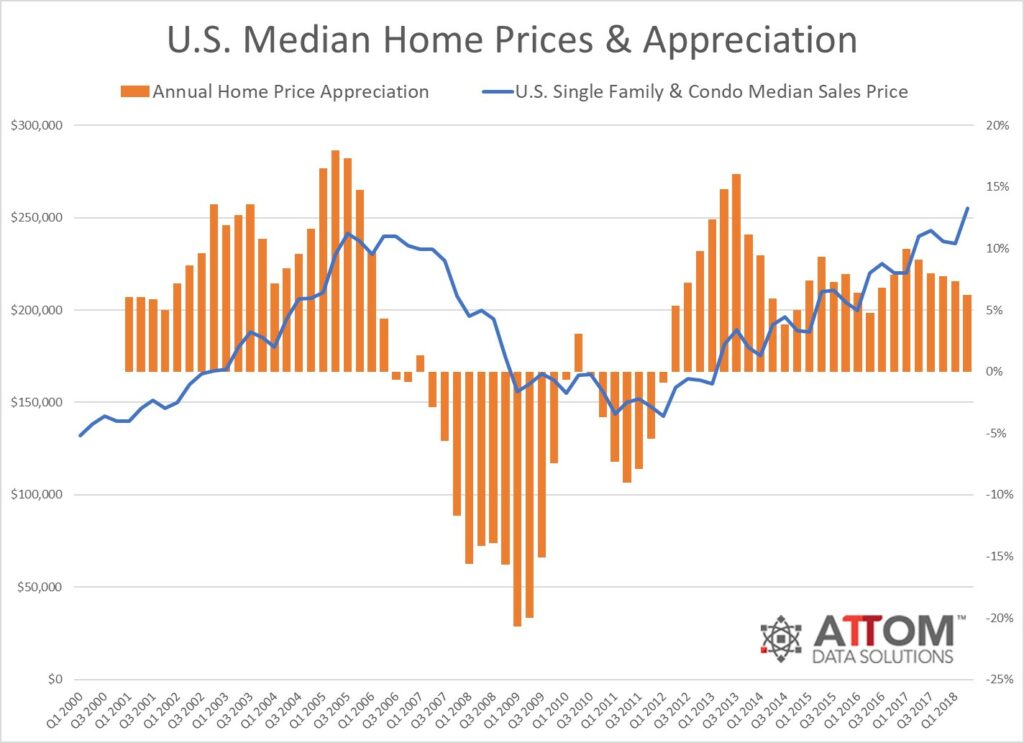

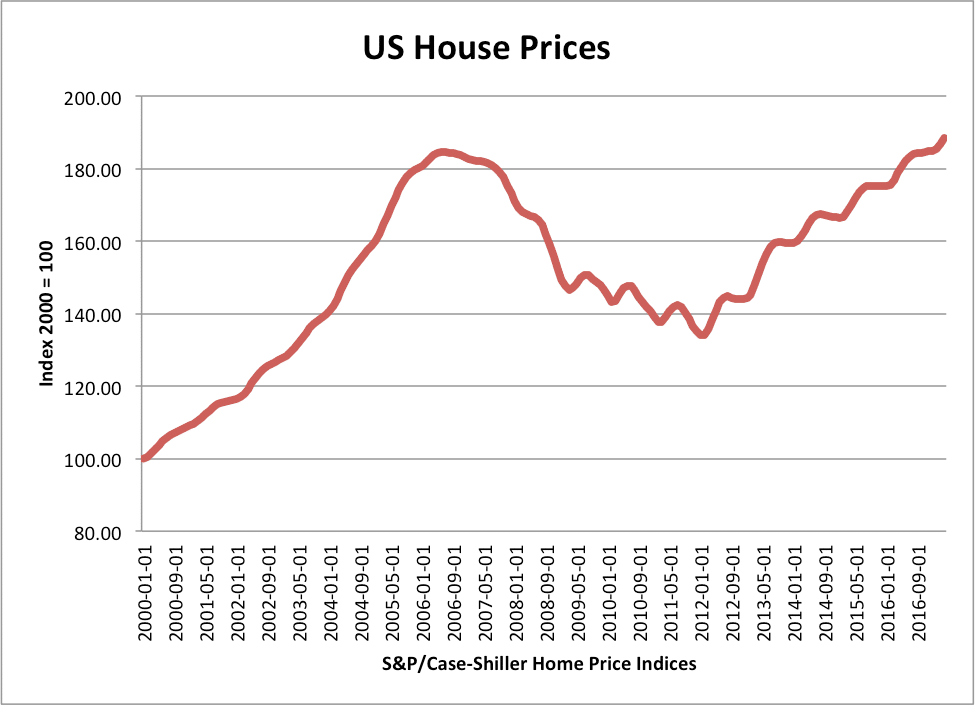

For years leading up to the crash, the U.S. housing market experienced an unprecedented boom. Driven by low interest rates, easy credit, and speculative buying, home prices soared to unsustainable levels, creating a classic economic bubble. Many homeowners treated their homes as ATMs, extracting equity through refinancing to fund consumption, assuming that property values would always appreciate. However, by 2006-2007, the supply of homes began to outpace demand, and the rising interest rates on adjustable-rate mortgages started to bite. When foreclosures increased, an influx of distressed properties hit the market, leading to a rapid decline in home values. The bursting of this bubble destroyed trillions in household wealth and triggered a domino effect across the financial sector.

Repercussions: Beyond Just Housing

The housing market crash was not an isolated incident; its effects rippled through every facet of the economy, both domestically and internationally. The impact extended far beyond mere property values, ushering in a period of profound economic contraction.

The Great Recession: Economic Fallout

The collapse of the housing market and the ensuing financial crisis plunged the U.S. into the Great Recession, one of the most severe economic downturns since the Great Depression. Banks, laden with toxic assets and distrustful of each other, stopped lending, effectively freezing the credit markets vital for business operations and consumer spending. Businesses faced immense pressure, leading to widespread layoffs and unemployment rates peaking at 10% in October 2009. Consumer confidence plummeted, further dampening demand and extending the economic pain. The crisis revealed deep vulnerabilities in the global financial architecture and the interconnectedness of major economies.

Impact on Personal Finance and Wealth

For millions of ordinary Americans, the crash was devastating. Homeowners saw their equity vanish overnight, leaving many “underwater” – owing more on their mortgages than their homes were worth. For those who had used their homes as investment vehicles, retirement savings plans were shattered. The stock market experienced a dramatic decline, eroding 401(k)s and other investment portfolios. The loss of wealth, combined with job insecurity, forced many families to cut back drastically on spending, delay major life milestones, and face immense financial hardship. The crisis underscored the dangers of over-leveraging and concentrating a large portion of one’s wealth in a single asset class like real estate, especially when driven by speculative forces.

Global Contagion: An Interconnected World

The securitization of subprime mortgages meant that financial institutions worldwide held these toxic assets. European banks, in particular, had significant exposure to MBS and CDOs. When the U.S. housing market crumbled, these institutions also faced massive losses, leading to a global credit crunch. The interconnectedness of the financial system meant that a crisis originating in the U.S. housing market quickly became an international emergency, highlighting the need for global cooperation in financial regulation and stability.

Government Responses and Regulatory Overhaul

In the face of an unprecedented economic crisis, governments and central banks around the world, particularly in the U.S., undertook extraordinary measures to prevent a complete collapse of the financial system. These interventions were controversial but largely credited with stabilizing the economy.

Bailouts and Stimulus Packages

The U.S. government, under both the Bush and Obama administrations, implemented a series of aggressive measures. The Troubled Asset Relief Program (TARP), enacted in October 2008, authorized the Treasury to purchase or insure troubled assets, primarily from financial institutions. The Federal Reserve aggressively cut interest rates to near zero and initiated Quantitative Easing (QE), buying vast amounts of government bonds and mortgage-backed securities to inject liquidity into the market. These actions, while often criticized for bailing out “too big to fail” institutions, were deemed necessary to restore confidence and unfreeze credit markets. Additionally, the American Recovery and Reinvestment Act of 2009 provided a massive fiscal stimulus package to boost the economy through government spending and tax cuts.

Dodd-Frank Act: Preventing Future Crises

To address the systemic weaknesses exposed by the crisis, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act in 2010. This landmark legislation aimed to prevent a repeat of 2008 by significantly reforming financial regulation. Key provisions included establishing the Financial Stability Oversight Council to monitor systemic risk, creating the Consumer Financial Protection Bureau (CFPB) to protect consumers in financial markets, imposing stricter capital requirements on banks, and regulating derivatives markets more tightly. While its effectiveness and reach have been debated and sometimes rolled back, Dodd-Frank represented a substantial effort to rein in the excesses of the financial sector.

A New Era of Lending Standards

One of the most immediate and lasting impacts of the crisis was a dramatic tightening of mortgage lending standards. Gone were the days of “no-doc” loans or mortgages with little to no down payment for risky borrowers. Lenders became much more stringent, requiring higher credit scores, larger down payments, and thorough verification of income and employment. The ability-to-repay rule, a key component of Dodd-Frank, mandated that lenders verify a borrower’s capacity to repay a mortgage before extending credit. While making homeownership more challenging for some, these stricter standards have generally led to a more stable mortgage market with fewer risky loans.

Lessons Learned for Investors and Homeowners

The 2008 housing market crash served as a brutal, expensive lesson for individuals, institutions, and governments alike. Its legacy continues to shape financial planning and economic policy today.

The Importance of Due Diligence

For investors, the crisis highlighted the critical importance of understanding what you’re investing in. The complexity and opacity of MBS and CDOs, coupled with misleading credit ratings, underscored the need for rigorous due diligence rather than blindly trusting financial products. Homeowners, too, learned the hard way about the fine print of their mortgages, particularly adjustable-rate features and predatory clauses. Financial literacy and independent research are indispensable.

Diversification and Risk Management

The notion that housing prices would always rise proved to be a dangerous fallacy. The crisis starkly illustrated the perils of over-concentrating wealth in a single asset class, even one as seemingly stable as real estate. It reinforced the fundamental principle of diversification in investment portfolios and the importance of having an emergency fund to weather economic storms. Avoiding excessive leverage, whether in personal debt or investment strategies, became a core tenet of prudent financial management.

Market Cycles and Economic Indicators

The 2008 crash was a stark reminder that markets operate in cycles, and booms are inevitably followed by busts. Learning to recognize the warning signs of speculative bubbles – rapidly accelerating prices, widespread irrational exuberance, and loose lending – is crucial. Paying attention to key economic indicators like interest rates, unemployment figures, inflation, and consumer debt levels can provide valuable insights into the health of the economy and potential market shifts.

Building Financial Resilience

For homeowners, the crisis underscored the value of maintaining a significant equity stake in their homes, avoiding excessive refinancing, and ensuring that mortgage payments are comfortably within their budget. For all individuals, building a robust financial safety net through savings, managing debt responsibly, and having diversified investments are essential for weathering future economic uncertainties, whatever their source may be.

The Housing Market Today: Is Another Crash Looming?

Given the trauma of 2008, a natural and recurring question is whether another housing market crash is on the horizon. While caution is always warranted, the current landscape presents significant differences compared to the pre-2008 environment.

Current Market Conditions vs. 2008

Today’s housing market, particularly in the U.S., is characterized by much tighter lending standards. The widespread proliferation of subprime mortgages is largely absent, and borrowers generally have stronger credit profiles and larger down payments. Homeowners also possess significantly more equity in their homes than in 2006-2007, making them more resilient to price fluctuations. While prices have seen substantial appreciation in recent years, especially post-pandemic, the underlying dynamics of leverage and speculative excess are not as pronounced as they were during the peak of the last bubble. Inventory levels have also remained historically low, contributing to price growth through supply-demand imbalances, rather than purely speculative forces.

Factors Influencing Stability (or Instability)

Several factors influence the current housing market’s stability. Rising interest rates, a response to inflation, have begun to cool demand and temper price growth. This is a deliberate policy to bring inflation under control and stabilize the economy, not a sign of predatory lending. A robust job market and rising wages (though sometimes lagging inflation) provide support for housing affordability. However, high inflation, a potential economic recession, and geopolitical instability remain potential headwinds. The key difference is the current financial system’s increased resilience and tighter regulatory oversight, which should prevent a crisis of the same systemic magnitude as 2008, even if localized market corrections occur.

Prudent Planning for Future Uncertainties

For both aspiring homeowners and existing property owners, prudent financial planning remains paramount. This includes maintaining a healthy emergency fund, avoiding taking on more mortgage debt than comfortably affordable, and considering the long-term commitment of homeownership. Investors should continue to diversify their portfolios and avoid emotional decisions driven by market hype or fear. While economic cycles are inevitable, the lessons of 2008 have equipped regulators, financial institutions, and informed individuals with better tools and understanding to navigate future challenges.

In conclusion, the housing market crash of 2008 was a defining moment in recent financial history, serving as a stark reminder of the interconnectedness of global finance and the critical importance of sound financial principles. It was a crisis born of lax regulation, speculative excess, and unsustainable lending. While the scars remain, the profound lessons learned continue to guide financial decisions, regulatory policy, and our approach to personal finance and investing in the dynamic world of money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.