Understanding the landscape of stock market participation in the United States is more than just a statistical exercise; it’s a critical lens through which to view economic health, wealth distribution, and the financial strategies of millions of households. The stock market, historically a powerful engine for wealth creation, plays a pivotal role in retirement planning, long-term savings, and overall financial security for many Americans. However, access to and engagement with this market are far from universal, reflecting a complex interplay of economic status, demographics, financial literacy, and technological advancements.

This article delves into the dynamic figures behind stock market ownership, dissecting not just the raw percentages but also the underlying factors that influence who invests, how they invest, and the profound implications of these patterns for individual financial futures and the broader economy. We’ll explore historical trends, identify key demographic disparities, examine the drivers and barriers to participation, and consider the impact of market engagement on wealth building, all strictly through the lens of personal finance and investing.

The Shifting Landscape of American Stock Ownership

The notion of “Americans in the stock market” is not a static concept but rather a fluid measure influenced by economic cycles, regulatory changes, and evolving investment technologies. Over the decades, the pathways and prevalence of stock ownership have undergone significant transformations, leading to today’s diverse participation rates.

Historical Trends and Evolution

Before the mid-20th century, direct stock ownership was largely the domain of the wealthy, characterized by active trading and speculative ventures. The landscape began to shift dramatically with the post-World War II economic boom and, more profoundly, with the advent of employer-sponsored retirement plans. The Employee Retirement Income Security Act (ERISA) of 1974 and the subsequent popularization of 401(k) plans in the 1980s fundamentally democratized access to the stock market. These plans, often offering matching contributions from employers, provided a simple and effective vehicle for employees to invest in mutual funds and other securities, albeit often indirectly.

The dot-com boom of the late 1990s saw a surge in direct retail investing, fueled by easier access through discount brokers and the dawn of online trading. While the subsequent bust tempered some of this enthusiasm, the trend toward greater accessibility continued. The 2008 financial crisis momentarily reduced participation as market volatility scared some investors away, but the recovery and subsequent bull market, combined with further technological innovations, have brought new waves of investors into the fold. More recently, the rise of commission-free trading platforms, fractional share investing, and user-friendly mobile apps has lowered the entry barrier even further, attracting a younger and more diverse cohort of retail investors.

Current Participation Rates (Approximate Figures)

Determining the precise percentage of Americans in the stock market requires careful definition, as ownership can be direct (individual stocks) or indirect (mutual funds, exchange-traded funds, 401(k)s, IRAs). Data from reputable sources like the Federal Reserve Board’s Survey of Consumer Finances (SCF), Gallup, and the Investment Company Institute (ICI) provide valuable insights, though their methodologies may yield slightly different numbers.

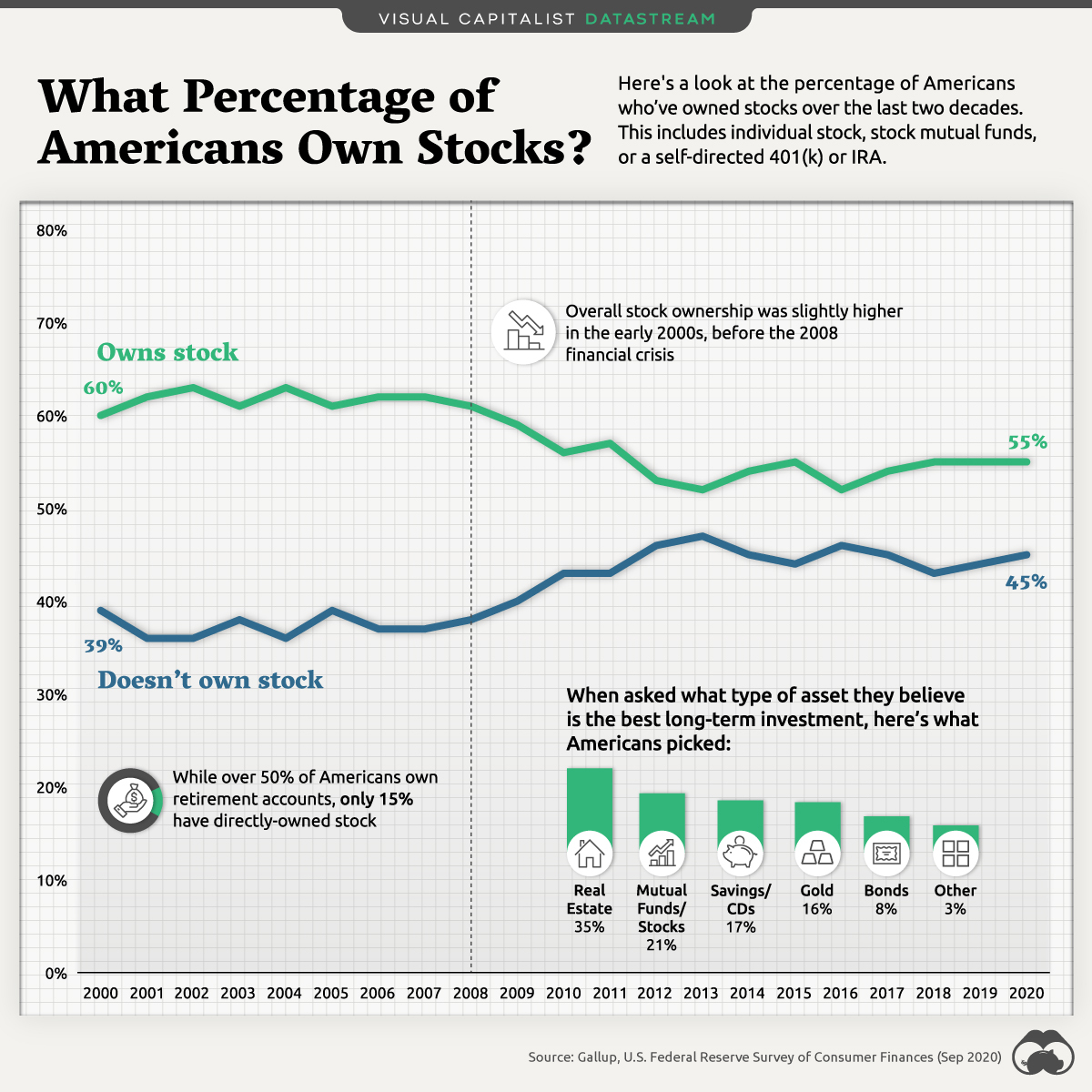

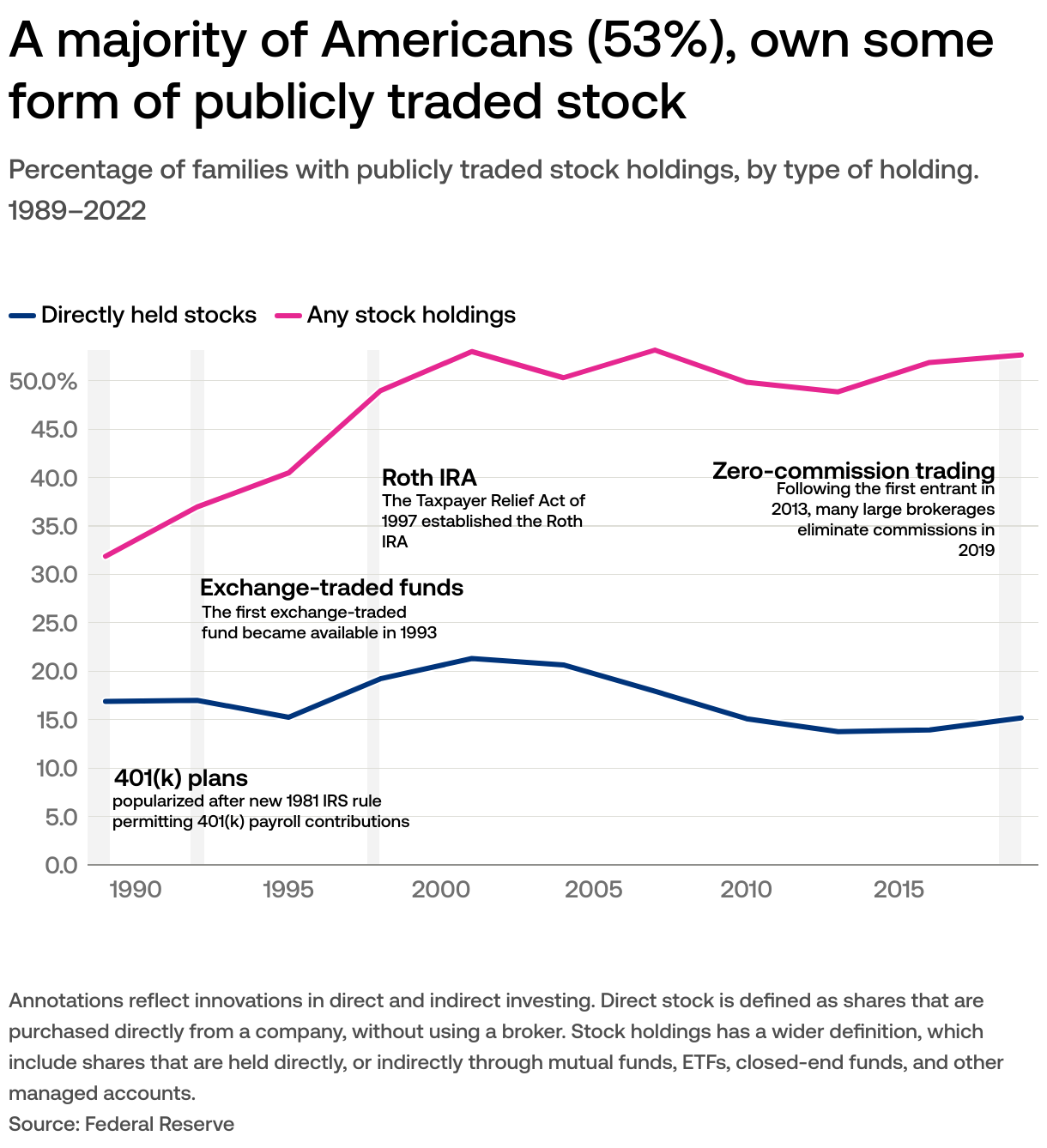

Generally, when considering all forms of stock market participation – including direct stock holdings, mutual funds, ETFs, and retirement accounts like 401(k)s and IRAs that invest in equities – the percentage of U.S. households owning stocks has typically hovered between 50% and 60% in recent years. For instance, the Federal Reserve’s SCF data often shows around 55-60% of households holding stocks directly or indirectly through retirement accounts. Gallup polls have also frequently reported figures in this range, though sometimes slightly lower for direct ownership only.

It’s crucial to distinguish: a much smaller percentage of Americans hold individual stocks directly (often in the 15-25% range), while the larger percentage reflects ownership through diversified funds within retirement accounts, which is the primary mode of stock market participation for the majority. This indirect ownership is a testament to the success of retirement savings vehicles in bringing mainstream Americans into the equity markets.

Demographics of Stock Market Participation

While the overall percentage offers a broad view, a deeper dive reveals significant disparities across various demographic groups. These differences underscore underlying inequalities in wealth, income, education, and access to financial resources, fundamentally shaping who benefits from market gains.

Age and Life Stage

Age is a significant predictor of stock market participation. Younger individuals, particularly those in their 20s and early 30s, typically have lower participation rates due to factors like lower incomes, student loan debt, and a focus on immediate financial goals (e.g., saving for a down payment). However, this trend is shifting as new platforms make investing more accessible to younger generations. Millennials and Gen Z, despite facing economic headwinds, are increasingly engaging with the market, often starting with smaller amounts via micro-investing apps or fractional shares.

Participation generally peaks among those in their prime working years (ages 35-64) as incomes rise, careers stabilize, and retirement planning becomes a more urgent priority. Employer-sponsored retirement plans are a major driver for this group. Participation remains high for those nearing retirement and in early retirement (65-74) as they manage their accumulated wealth, though asset allocation might shift towards more conservative investments.

Income and Wealth Disparities

Perhaps the most pronounced disparity is observed along income and wealth lines. Stock market participation is strongly correlated with higher income and greater wealth. Households in the top income quintile (the wealthiest 20%) consistently show participation rates well above 80-90%, and often close to 100% in some forms. As income levels decrease, so does participation. Households in the lowest income quintile often have participation rates below 20-30%.

This strong correlation highlights a critical aspect of wealth inequality: those who already have more are better positioned to invest and benefit from the compounding returns of the stock market, further widening the wealth gap. Access to surplus income, beyond essential living expenses, is a fundamental prerequisite for investing.

Education and Financial Literacy

Higher levels of education are generally associated with greater stock market participation. Individuals with college degrees or advanced degrees are more likely to invest, often due to higher earning potential, increased financial literacy, and greater exposure to financial planning concepts. Education often correlates with an understanding of financial instruments, risk tolerance, and the long-term benefits of investing, making individuals more confident in navigating the market.

Conversely, a lack of financial literacy and understanding of basic investment principles can act as a significant barrier. Many non-investors express feeling overwhelmed by the complexity of the stock market or unsure of where to start, even if they have some disposable income.

Race and Ethnicity

Disparities in stock market participation also exist across racial and ethnic groups in the U.S., often reflecting broader socioeconomic inequalities. White households typically have higher rates of stock ownership compared to Black and Hispanic households. For instance, data often shows White households’ participation rates being 1.5 to 2 times higher than those of Black or Hispanic households. These disparities are often intertwined with differences in income, wealth accumulation, historical systemic barriers, and access to financial education and institutions. Addressing these gaps requires targeted efforts to improve financial inclusion and combat structural inequalities.

Drivers and Barriers to Stock Market Entry

Understanding why some Americans invest while others do not is crucial for designing policies and tools that can foster broader financial inclusion. Both powerful motivators and significant obstacles shape an individual’s decision to enter the stock market.

Factors Encouraging Participation

- Employer-Sponsored Retirement Plans: For many, the 401(k) or 403(b) plan is their first and often only direct interaction with the stock market. Auto-enrollment features, employer matching contributions, and payroll deductions make saving and investing relatively effortless, lowering the psychological and practical barriers to entry.

- Accessibility Through Technology: The digital revolution has democratized investing. Commission-free trading, fractional shares, robo-advisors, and user-friendly mobile apps have made it easier and cheaper than ever to start investing with small amounts of capital. This has particularly resonated with younger generations.

- Increased Financial Education and Awareness: Growing access to financial information through online resources, blogs, podcasts, and social media has empowered more individuals to learn about investing. While quality varies, the sheer volume of available knowledge helps demystify the market for many.

- Long-Term Wealth Creation Potential: The historical performance of the stock market, despite its volatility, makes it one of the most effective tools for building long-term wealth, outpacing inflation and other savings vehicles. The promise of compounding returns is a powerful draw for those focused on retirement or other significant life goals.

Obstacles Preventing Investment

- Lack of Disposable Income/Savings: This is arguably the most significant barrier. Many Americans live paycheck to paycheck, struggling with high living costs, stagnant wages, and emergency expenses. Without surplus income, investing simply isn’t an option.

- Fear of Risk and Market Volatility: The inherent volatility of the stock market can be a major deterrent. Memories of market crashes (e.g., 2000, 2008, 2020) can instill a fear of loss, leading individuals to keep their money in “safer” but lower-growth options like savings accounts.

- Perceived Complexity and Lack of Financial Knowledge: Despite increased access to information, many still find the stock market intimidating and complex. A lack of understanding of basic investment concepts (diversification, risk vs. return, asset allocation) prevents many from taking the first step.

- Mistrust in the Financial System: A lingering distrust of Wall Street, financial institutions, and the broader economic system, particularly among those who feel left behind or exploited, can prevent engagement.

- Debt Prioritization: For many, tackling high-interest debt (credit card, student loans) takes precedence over investing. While a sound financial strategy often balances both, the psychological and financial burden of debt can leave no room for market participation.

The Impact of Stock Market Participation on Wealth Building

For those who do participate, the stock market serves as a primary engine for building substantial wealth over time. Its role is central to retirement security and intergenerational wealth transfer, though its uneven distribution means its benefits are not equally shared.

Long-Term Growth and Compounding

The stock market has historically outperformed most other asset classes over the long term. Investing in equities allows individuals to participate in the growth of companies and the broader economy. The power of compounding – earning returns not only on the initial investment but also on accumulated interest and dividends – is the cornerstone of significant wealth accumulation. A modest, consistent investment made early can grow into a substantial sum over decades, far exceeding what simple savings accounts can offer. This long-term growth is critical for funding retirements, buying homes, or financing children’s education.

Bridging the Wealth Gap (or Widening It)

Ideally, broader stock market participation could serve as a powerful tool to bridge the wealth gap, allowing more segments of the population to build assets. However, in practice, the current distribution of ownership tends to exacerbate existing inequalities. Those who can afford to invest grow wealthier, while those who cannot fall further behind. Policies and initiatives aimed at increasing equitable access to investment opportunities are essential if the market is to become a more inclusive mechanism for wealth building. A robust economy also benefits from widespread investment, as it provides capital for businesses to innovate and expand.

The Role of Financial Planning

Stock market participation is most effective when integrated into a comprehensive financial plan. This includes setting clear financial goals, understanding one’s risk tolerance, diversifying investments across various asset classes, and maintaining a long-term perspective. Professional financial advisors can play a crucial role in guiding individuals through this process, helping them make informed decisions and avoid common pitfalls, though access to such advice is another layer of privilege. For those without advisors, accessible educational resources and user-friendly tools are vital.

Strategies to Increase Stock Market Participation

Recognizing the disparities and the importance of investing for financial well-being, various strategies are being explored to encourage broader and more equitable stock market participation across the American population.

Enhancing Financial Education

Investing in financial literacy from an early age is paramount. Integrating personal finance into school curricula, launching public awareness campaigns about saving and investing, and providing accessible online resources can empower individuals with the knowledge and confidence to engage with the market. Demystifying complex financial concepts and highlighting the long-term benefits of investing are key objectives.

Policy Initiatives

Government policies can significantly influence participation rates. Auto-enrollment and auto-escalation features in employer-sponsored retirement plans have proven highly effective in increasing participation and savings rates. Tax incentives for saving and investing (e.g., IRAs, 401(k)s) also encourage participation. Furthermore, policies that simplify investment products and reduce regulatory hurdles for small investors could make the market less intimidating. Exploring options for universal savings accounts or targeted savings programs could also help bring lower-income households into the investment fold.

Technological Innovation

The financial technology (FinTech) sector continues to innovate, creating more user-friendly and affordable investment solutions. Continued development of micro-investing platforms, fractional share capabilities, and sophisticated yet intuitive robo-advisors can further lower the barrier to entry, making it feasible for individuals to start investing with very small amounts of money. These technologies can particularly appeal to younger investors and those new to the market.

Conclusion

The question of “what percentage of Americans are in the stock market” reveals a story of progress and persistent challenges. While a significant portion of U.S. households—around 50-60%—participates directly or indirectly, primarily through retirement accounts, this engagement is far from uniform. Deep demographic divides based on income, wealth, age, education, and race underscore fundamental inequalities in access to wealth-building opportunities.

The stock market remains an indispensable tool for long-term wealth creation, offering the potential for significant compounding returns that can secure financial futures. As technology continues to lower barriers and financial education efforts expand, there is a growing opportunity to foster more widespread and equitable participation. However, addressing the root causes of financial exclusion, such as income inequality and lack of savings, alongside improving financial literacy and trust, will be critical to ensuring that the benefits of market investment are truly accessible to all Americans, contributing to a more financially secure and robust society.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.