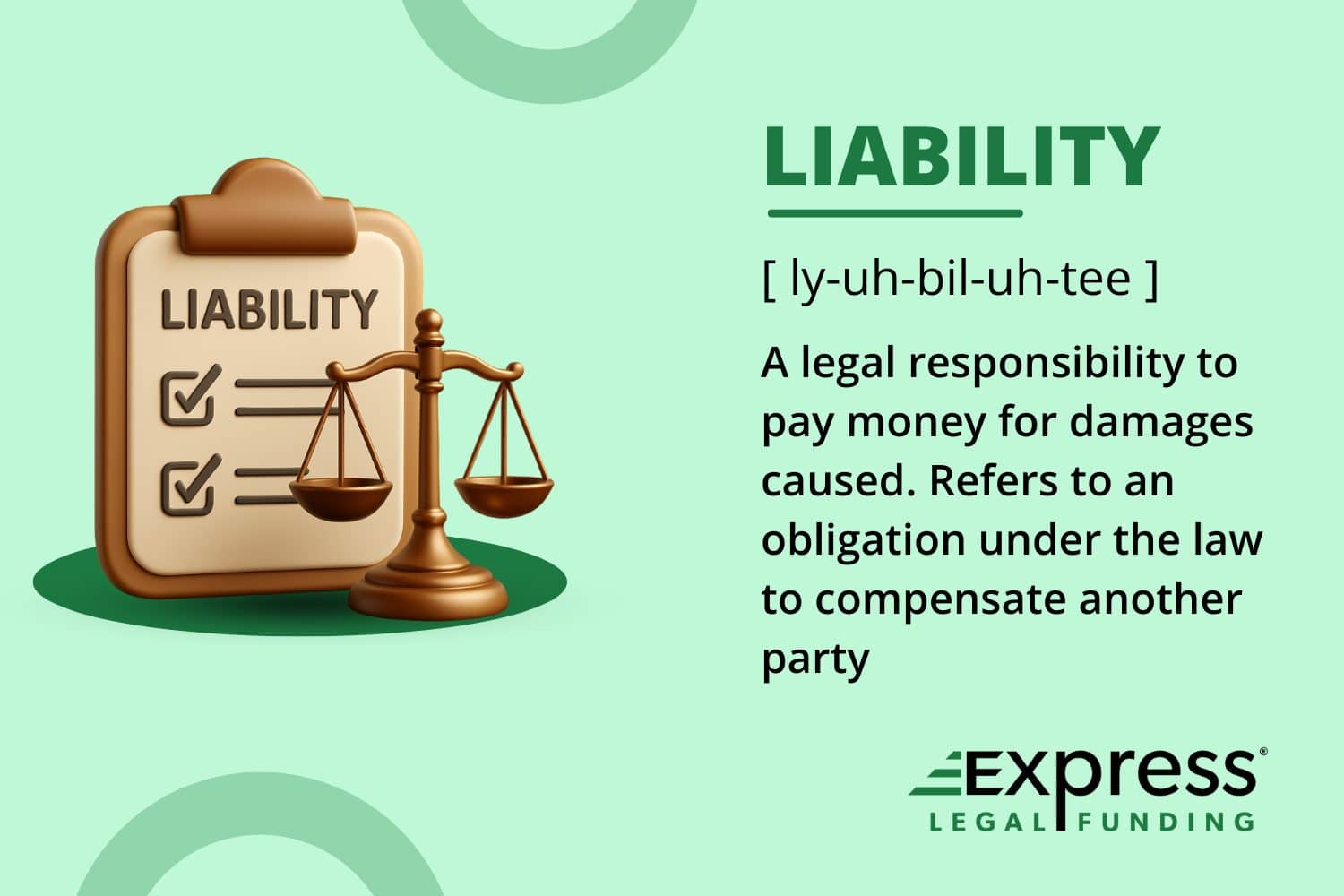

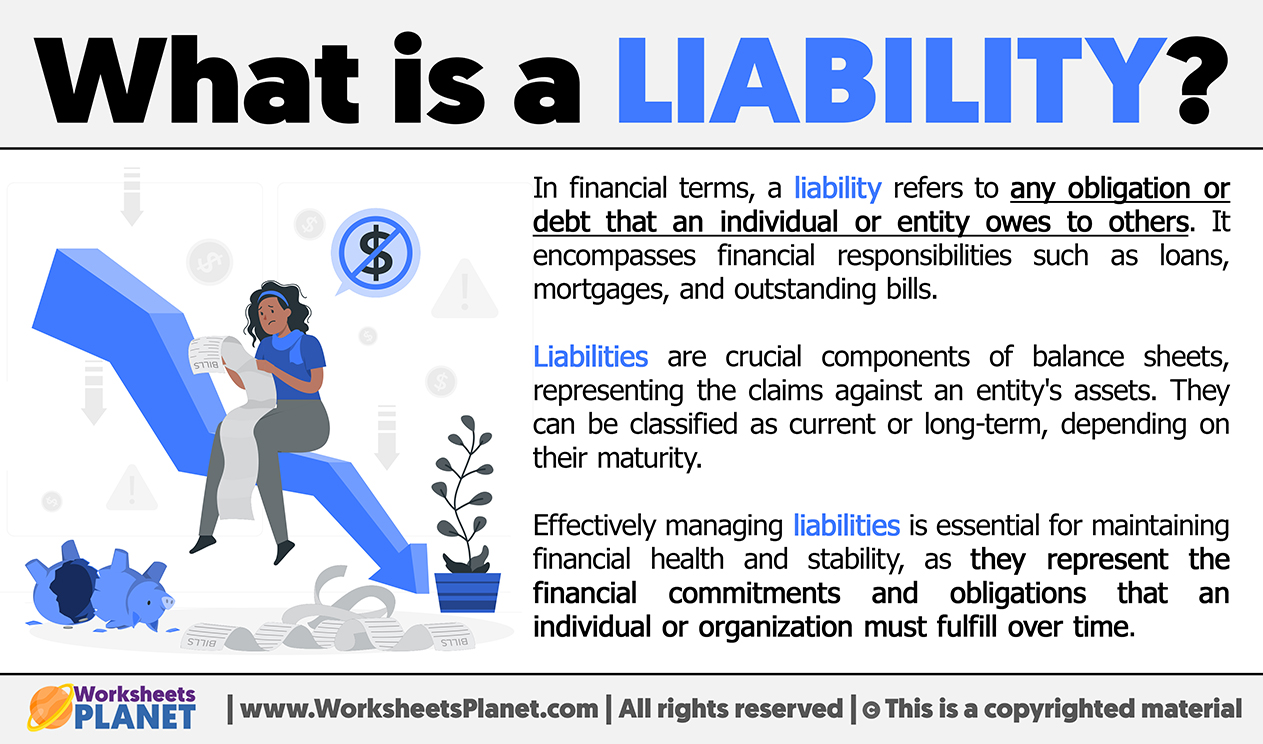

In the intricate world of finance, business, and personal economics, few terms carry as much weight and widespread relevance as “liability.” Far from being a mere accounting jargon, understanding what constitutes a liability is fundamental to assessing financial health, making informed investment decisions, and navigating one’s personal financial journey. At its core, a liability represents a financial obligation or debt that an individual, company, or government owes to another party. It is a future economic sacrifice that arises from past transactions or events. Essentially, if you owe something to someone else, that “something” is a liability. This comprehensive exploration will delve into the multifaceted nature of liabilities, dissecting their various forms, their critical role in financial analysis, and strategies for effective management, all firmly rooted in the domain of money and finance.

What Exactly is a Liability? A Fundamental Definition

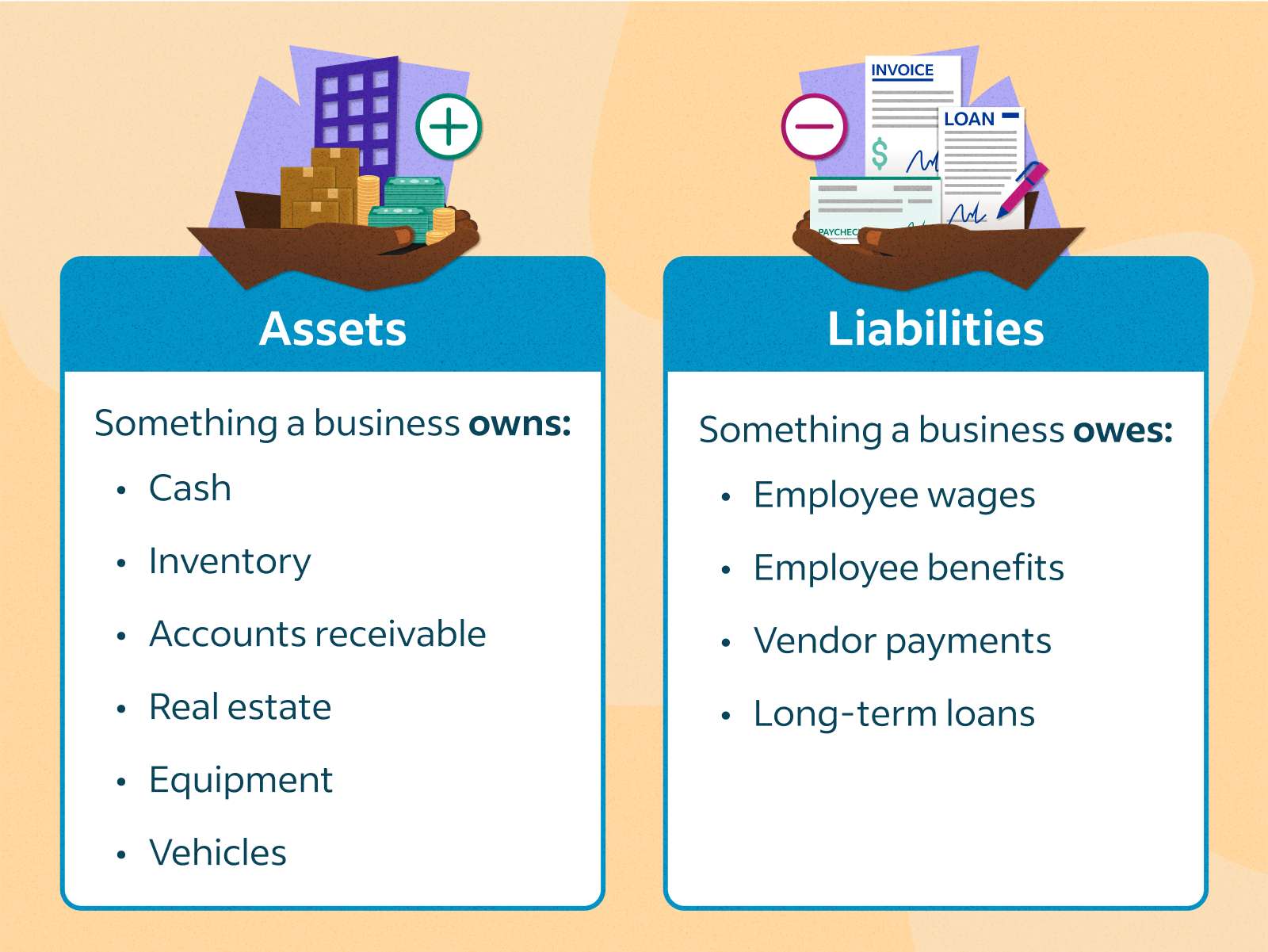

To truly grasp the essence of a liability, we must first establish a clear and concise definition, understanding its place within the broader financial ecosystem. In accounting and finance, liabilities are legally binding obligations to transfer economic benefits (e.g., cash, goods, or services) to another entity as a result of past transactions or events. They are distinct from assets, which represent economic resources expected to provide future benefits, and equity, which is the residual claim on assets after deducting liabilities.

The Accounting Equation: Assets, Liabilities, and Equity

The foundation of double-entry accounting, and indeed much of financial reporting, rests on the fundamental accounting equation:

Assets = Liabilities + Equity

This equation illustrates the intrinsic relationship between these three core components. It signifies that everything a company owns (its assets) is financed either by borrowing from external parties (liabilities) or by investments from owners and retained earnings (equity). For individuals, a similar principle applies: your possessions (assets) are offset by what you owe (liabilities) and your net worth (equity). When a business takes out a loan, it increases both its assets (cash received) and its liabilities (the loan payable). When a customer buys on credit, the business records an asset (accounts receivable) and recognizes revenue which eventually increases equity, but if the business owes a supplier, it records a liability (accounts payable). This balance is crucial for transparency and provides a snapshot of an entity’s financial structure.

Key Characteristics of a Liability

For an item to be classified as a liability, it must exhibit several key characteristics:

- It Involves a Future Sacrifice: There must be an obligation to transfer assets or provide services at some point in the future. This future sacrifice is the core of what defines a liability.

- It is an Obligation: The entity has little or no discretion to avoid the transfer of economic benefits. This obligation can be legal (e.g., a contract, a loan agreement) or constructive (e.g., a warranty for a product sold, where there’s an implied obligation based on past practice or public statements).

- It Arises from Past Transactions or Events: The obligation must stem from an event that has already occurred. For example, taking out a loan creates a liability now for future repayment, not when the loan is merely contemplated. Similarly, purchasing inventory on credit creates an accounts payable liability as soon as the purchase is made.

Understanding these characteristics is vital because they differentiate genuine liabilities from mere intentions, commitments, or contingent possibilities that may not yet meet the criteria for recognition on a balance sheet.

Categorizing Liabilities: Current, Non-Current, and Contingent

Liabilities are not monolithic; they come in various forms, primarily categorized by the timeframe within which they are expected to be settled. This classification is crucial for financial analysis, offering insights into an entity’s liquidity and long-term solvency.

Current Liabilities: The Short-Term Picture

Current liabilities are obligations that are expected to be settled within one year of the balance sheet date or within the normal operating cycle of the business, whichever is longer. These are crucial indicators of a company’s short-term financial health and its ability to meet immediate financial obligations. A healthy proportion of current assets (like cash, accounts receivable, and inventory) to current liabilities suggests strong liquidity.

Common examples of current liabilities include:

- Accounts Payable: Money owed to suppliers for goods or services purchased on credit.

- Notes Payable (Short-Term): Promissory notes due within a year.

- Salaries and Wages Payable: Money owed to employees for work performed but not yet paid.

- Interest Payable: Interest accumulated on loans but not yet paid.

- Income Taxes Payable: Taxes owed to the government.

- Unearned Revenue (Deferred Revenue): Money received from customers for goods or services not yet delivered (e.g., a subscription paid in advance).

- Current Portion of Long-Term Debt: The portion of a long-term loan that is due for repayment within the next 12 months.

Non-Current (Long-Term) Liabilities: The Enduring Commitments

Non-current liabilities, also known as long-term liabilities, are obligations that are not expected to be settled within one year or the normal operating cycle. These represent more enduring financial commitments that often involve larger sums and are critical for understanding an entity’s long-term financial structure and solvency. They are typically used to finance long-term assets or operations.

Key examples of non-current liabilities include:

- Bonds Payable: Debt securities issued by companies or governments to raise capital, typically maturing in several years.

- Long-Term Notes Payable: Promissory notes due beyond one year.

- Mortgages Payable: Loans secured by real estate, repaid over many years.

- Deferred Tax Liabilities: Taxes that are accrued but not yet paid, often due to differences in accounting and tax treatment of certain items.

- Pension Obligations: Liabilities related to defined benefit pension plans owed to employees upon retirement.

- Lease Liabilities: Obligations arising from long-term lease agreements, often reflecting the right-of-use asset under IFRS 16 or ASC 842.

Contingent Liabilities: Unfolding Uncertainties

Unlike current and non-current liabilities, contingent liabilities are potential obligations that depend on the outcome of a future event. These are not recognized on the balance sheet if their probability of occurrence is remote. However, if the likelihood of the event occurring is probable and the amount can be reasonably estimated, the liability is recognized. If the likelihood is reasonably possible but not probable, or if the amount cannot be reasonably estimated, it is typically disclosed in the notes to the financial statements rather than recorded as a specific liability on the balance sheet itself.

Examples of contingent liabilities include:

- Lawsuits and Legal Claims: Potential financial obligations arising from ongoing legal proceedings.

- Product Warranties: Obligations to repair or replace defective products within a specified period.

- Environmental Liabilities: Potential costs associated with environmental clean-up or regulatory fines.

- Guarantees: Promises to pay the debt of another party if they default.

The treatment of contingent liabilities requires careful judgment and can significantly impact an entity’s reported financial position and risk profile.

The Crucial Role of Liabilities in Financial Analysis

Understanding liabilities is not merely an academic exercise; it is a vital component of financial analysis for businesses, investors, and individuals alike. Liabilities provide a window into an entity’s financial health, risk exposure, and operational efficiency.

For Businesses: Evaluating Solvency and Liquidity

For business owners and managers, meticulously tracking and analyzing liabilities is paramount for strategic decision-making.

- Liquidity Ratios: Current liabilities are central to liquidity ratios (e.g., current ratio, quick ratio), which measure a company’s ability to meet its short-term obligations. A high current ratio indicates that a company has sufficient current assets to cover its current liabilities, suggesting good short-term financial health.

- Solvency Ratios: Long-term liabilities are key to solvency ratios (e.g., debt-to-equity ratio, debt-to-asset ratio), which assess a company’s ability to meet its long-term obligations and its overall financial stability. High debt-to-equity ratios can signal higher financial risk, as the company relies heavily on borrowed funds rather than owner equity.

- Capital Structure Decisions: Businesses must strategically manage their mix of debt (liabilities) and equity to optimize their cost of capital, manage risk, and fund growth initiatives. Too much debt can lead to financial distress, while too little can mean missed growth opportunities.

For Investors: Uncovering Risk and Opportunity

Investors scrutinize a company’s liabilities to make informed decisions about buying, selling, or holding securities.

- Risk Assessment: High levels of debt can signal increased risk. If a company struggles to generate sufficient cash flow, it may face difficulty servicing its debt, leading to potential bankruptcy. Understanding the terms of a company’s debt (interest rates, maturity dates, covenants) is crucial.

- Growth Potential: While debt implies risk, it can also be a powerful tool for growth. Companies often take on long-term liabilities to fund expansion, research and development, or acquisitions. An investor needs to evaluate if the debt is being used productively to generate future returns.

- Financial Leverage: Debt can magnify returns on equity. If a company can earn a higher rate of return on its borrowed money than the interest it pays, it effectively leverages its equity. However, this also works in reverse, amplifying losses if investments underperform.

For Personal Finance: Understanding Your Financial Obligations

On a personal level, liabilities represent your personal debts and obligations, which are crucial for managing your financial well-being and planning for the future.

- Budgeting and Cash Flow: Understanding your current liabilities (e.g., credit card bills, utility payments, rent/mortgage payments) is essential for effective budgeting and managing monthly cash flow.

- Net Worth Calculation: Your personal net worth is calculated by subtracting your total liabilities (mortgages, car loans, student loans, credit card debt) from your total assets (home equity, savings, investments, car value). A positive and growing net worth is a key indicator of financial health.

- Credit Score Impact: How you manage your personal liabilities, particularly debt repayment, directly impacts your credit score, which, in turn, affects your ability to borrow money for major purchases like a home or car, and even influences insurance rates.

- Retirement Planning: Long-term liabilities, such as outstanding mortgage principal, must be factored into retirement planning to ensure financial security in later years.

Effective Management and Strategic Mitigation of Liabilities

Managing liabilities effectively is critical for sustained financial health, whether for a multinational corporation or an individual. It involves not just paying bills on time, but strategic planning and ongoing assessment.

Best Practices for Businesses

Businesses employ various strategies to manage their liabilities:

- Debt Management Policies: Establishing clear policies for taking on new debt, managing existing debt, and ensuring timely repayment. This includes evaluating the cost of debt versus equity financing.

- Cash Flow Forecasting: Robust cash flow forecasting ensures that a business has sufficient liquidity to meet its current liabilities and debt service obligations.

- Refinancing Debt: Taking advantage of lower interest rates or more favorable terms by refinancing existing loans can reduce interest expenses and improve cash flow.

- Hedging Strategies: For businesses with foreign currency-denominated liabilities, hedging strategies can mitigate currency risk.

- Diversification of Funding Sources: Relying on a mix of debt types and lenders reduces dependence on any single source and can provide more flexibility.

- Strong Internal Controls: Implementing effective internal controls helps prevent fraud, errors, and unrecorded liabilities, maintaining financial integrity.

Smart Strategies for Individuals

For individuals, proactive liability management is key to building wealth and achieving financial independence:

- Budgeting and Debt Repayment Plans: Creating a budget helps track income and expenses, allowing for strategic allocation of funds towards debt repayment. The “debt snowball” or “debt avalanche” methods are popular strategies for prioritizing which debts to pay down first.

- Building an Emergency Fund: A robust emergency fund (3-6 months of living expenses) acts as a buffer against unexpected expenses, preventing the need to take on new, often high-interest, debt.

- Minimizing High-Interest Debt: Prioritizing the repayment of high-interest debts, such as credit card balances, is crucial, as the interest can rapidly accumulate and hinder financial progress.

- Responsible Borrowing: Only taking on debt that can be comfortably repaid and for assets that appreciate or generate income (e.g., a reasonable mortgage, student loans for a valuable education) is a cornerstone of smart personal finance.

- Monitoring Credit Reports: Regularly checking credit reports helps identify inaccuracies and potential fraud, which could impact your ability to manage existing and future liabilities.

- Seeking Professional Advice: For complex personal financial situations, consulting with a financial advisor can provide tailored strategies for debt management, investment, and long-term planning.

In conclusion, “liability” is far more than a word on an accountant’s ledger; it is a dynamic concept that shapes financial decisions at every level. From the strategic maneuvers of global corporations to the daily spending habits of individuals, understanding, classifying, analyzing, and proactively managing liabilities is indispensable. It empowers us to gauge financial risk, assess opportunities, and ultimately chart a course towards greater financial stability and prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.