Understanding the intricacies of income distribution in the United States is more than just a statistical exercise; it’s a window into economic mobility, societal structures, and individual financial realities. When we talk about “the top 10% income,” we’re not just referring to the handful of billionaires dominating headlines, but rather a significant segment of households and individuals who, through various means, have achieved a level of financial prosperity that places them distinctly above the national average. This deep dive aims to demystify what it truly means to be among the highest earners in the US, exploring the thresholds, the demographics, and the underlying dynamics that shape this elite financial tier.

In an economy as vast and diverse as that of the United States, income figures can vary dramatically based on location, profession, education, and household structure. Discerning the cutoff for the top 10% requires a careful examination of various data sources, recognizing that these numbers are fluid and subject to change with economic shifts, inflation, and policy alterations. Our goal here is to provide a comprehensive, insightful, and engaging perspective on this crucial aspect of American wealth.

Understanding Income Brackets: The Landscape of Wealth in America

The United States is characterized by significant income disparities, a reality that prompts ongoing discussions about economic fairness, opportunity, and the definition of financial success. To grasp what constitutes “top income,” it’s essential to first understand how income is typically measured and categorized.

Defining “Top 10%” Income

When financial experts or government bodies refer to the “top 10% income,” they are generally identifying the income level that a household or individual must exceed to be considered among the wealthiest 10% of the population. This isn’t a fixed dollar amount across all contexts but rather a dynamic threshold determined by the distribution of all incomes within a given period. For instance, if you line up all US households from lowest to highest income, the top 10% threshold is the income level of the household that sits at the 90th percentile. This figure is critical for understanding economic inequality and the concentration of wealth. It’s also important to distinguish between income (what you earn) and wealth (what you own, including assets like real estate, investments, and savings, minus debts). While income contributes to wealth, they are distinct concepts.

Key Data Sources and Methodologies

Accurate data on income distribution is typically compiled by several authoritative sources, each with its own methodology and reporting frequency. The most commonly cited include:

- The U.S. Census Bureau: Through its annual American Community Survey (ACS) and Current Population Survey (CPS), the Census Bureau collects extensive data on household and individual incomes, demographic characteristics, and poverty levels. Their data often provides the most comprehensive snapshot of income distribution across the nation.

- The Internal Revenue Service (IRS): The IRS publishes data based on tax returns, offering insights into taxable income. While this data is highly accurate for reported income, it might not capture all forms of income or represent the full economic picture for every household.

- The Federal Reserve Board’s Survey of Consumer Finances (SCF): Conducted every three years, the SCF is a gold standard for understanding household finances, wealth, and debt. It provides detailed information on assets, liabilities, and income, often shedding light on disparities that other surveys might miss.

These sources use varying definitions of “income” (e.g., pre-tax vs. post-tax, cash income vs. total income including benefits), which can lead to slightly different reported thresholds. However, they consistently paint a picture of significant stratification, with a clear distinction between the middle-class, upper-middle-class, and the top echelons of earners.

The Current Threshold: What It Takes to Be in the Top 10%

Pinpointing an exact, universally accepted figure for the top 10% income threshold is challenging due to the dynamic nature of economic data and differing methodologies. However, based on the latest available comprehensive data, we can establish a general understanding.

National Averages vs. Regional Disparities

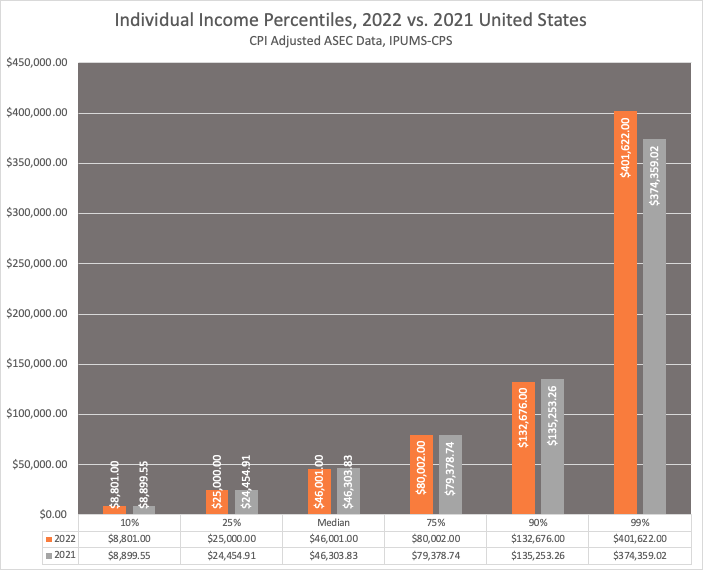

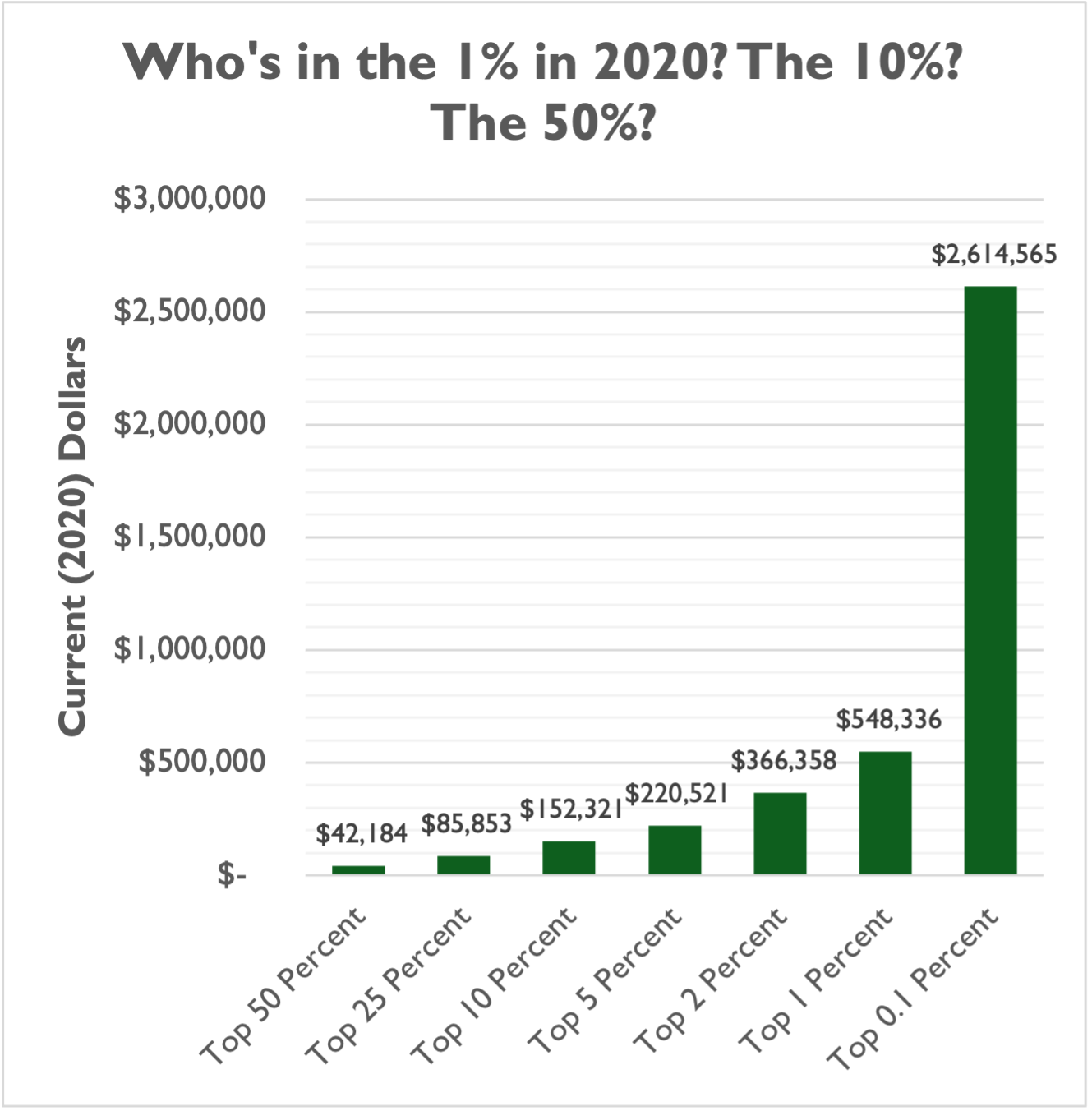

As of recent data (e.g., 2022-2023 figures from the Census Bureau and other financial analyses), the approximate income threshold for a household to be in the top 10% in the US typically hovers around $200,000 to $220,000 annually. For individuals, this figure is considerably lower, often closer to $120,000 to $150,000 annually, depending on the specific source and measurement. It’s crucial to remember these are national averages.

Regional disparities play a massive role. Earning $200,000 in a low-cost-of-living area in the Midwest provides a significantly higher quality of life and purchasing power than earning the same amount in a high-cost-of-living metropolitan area like San Francisco, New York City, or Washington D.C. In these expensive coastal cities, the income required to be in the top 10% can be substantially higher, often exceeding $300,000 or even $400,000 for households, reflecting the inflated costs of housing, goods, and services. Conversely, in more rural or less expensive urban areas, the threshold for the top 10% might be lower than the national average.

Household vs. Individual Income

The distinction between household and individual income is critical for accurate interpretation.

- Household income refers to the combined gross income of all individuals aged 15 or older who live in the same housing unit, regardless of their relationship. This aggregate figure is often higher because it can include multiple earners (e.g., a dual-income couple).

- Individual income pertains only to what one person earns.

Most analyses of income distribution, particularly those concerning economic inequality and the middle class, focus on household income as it better reflects the financial capacity and standard of living for a family unit. For instance, a household with two working professionals each earning $100,000 would collectively clear the top 10% household threshold, while individually they might be in a lower percentile for individual income.

Characteristics of High-Income Earners: Beyond the Numbers

Beyond the raw income figures, a closer look at the demographics and characteristics of those in the top 10% reveals common patterns related to education, profession, geography, and financial behaviors.

Education and Professional Fields

A strong correlation exists between higher education and higher income. A significant majority of top 10% earners hold at least a bachelor’s degree, with many possessing advanced degrees such as master’s degrees, Ph.D.s, J.D.s (law), or M.D.s (medicine). These degrees often open doors to lucrative professions that demand specialized knowledge and skills.

Typical professional fields that frequently place individuals and households in the top 10% include:

- Healthcare: Physicians, surgeons, specialized nurses, and medical researchers.

- Technology: Software engineers, data scientists, cybersecurity experts, IT managers, and executives in tech companies.

- Finance: Investment bankers, portfolio managers, financial analysts, and corporate finance executives.

- Law: Corporate lawyers, intellectual property attorneys, and senior legal counsel.

- Business and Management: Senior executives (CEOs, CFOs, COOs), management consultants, and successful entrepreneurs.

- Engineering: Petroleum engineers, aerospace engineers, and senior-level engineers in various industries.

These fields often require substantial investment in education and training, long working hours, and a high degree of responsibility, which are compensated accordingly.

Geographic Concentration and Cost of Living

As noted earlier, top earners are disproportionately concentrated in major metropolitan areas and economic hubs. Cities like New York, San Francisco, Boston, Washington D.C., Seattle, and Los Angeles are home to a larger share of high-income households. This concentration is due to several factors:

- Economic Opportunity: These cities are centers for high-paying industries (tech, finance, media, government) that offer numerous high-skill, high-wage jobs.

- Network Effects: The presence of a large professional network and a competitive job market can drive up salaries.

- Cost of Living: High salaries in these areas often reflect the significantly elevated cost of living, particularly housing. While a high income in these regions places one in the top percentile, the discretionary income might not feel as abundant as it would with the same salary in a lower-cost area.

Wealth Accumulation and Investment Strategies

While income is crucial, the accumulation of wealth is what truly distinguishes many in the top 10%. High earners often have the capacity to save and invest a larger portion of their income. Common wealth accumulation strategies include:

- Diversified Investment Portfolios: Investing in stocks, bonds, mutual funds, and exchange-traded funds (ETFs).

- Real Estate: Owning primary residences in appreciating markets, as well as investment properties.

- Retirement Accounts: Maximizing contributions to 401(k)s, IRAs, and other tax-advantaged retirement vehicles.

- Entrepreneurship and Business Ownership: Many top earners derive significant income and wealth from owning successful businesses or having substantial equity stakes.

- Strategic Financial Planning: Utilizing financial advisors, estate planning, and tax optimization strategies to preserve and grow wealth.

Factors Influencing Income Inequality and Upward Mobility

The structure of income distribution is not static; it’s a dynamic outcome influenced by a confluence of economic forces, policy decisions, and societal trends. Understanding these factors is key to comprehending why the top 10% income threshold is what it is, and why it can be challenging for others to reach it.

Economic Trends and Policy Impacts

Several broad economic trends have shaped income distribution over recent decades. Globalization has led to increased competition for certain jobs, while simultaneously opening up new markets for highly skilled professionals and businesses. Technological advancements, particularly in areas like AI, automation, and digital platforms, have created new high-paying industries and roles, often benefiting those with specialized technical skills, while displacing or devaluing other types of labor.

Government policies also play a significant role. Tax policies (e.g., progressive income taxes, capital gains taxes), labor laws, minimum wage regulations, and investments in education and infrastructure all impact how income is earned and distributed. For instance, policies that favor capital over labor or reduce the bargaining power of unions can contribute to wider income gaps. Conversely, investments in public education and affordable healthcare can enhance human capital and improve upward mobility.

The Role of Education and Skills Gap

The “skills gap” is a frequently discussed factor. As the economy becomes more knowledge-based, there’s an increasing demand for highly educated workers with specialized skills, particularly in STEM fields (Science, Technology, Engineering, and Mathematics). Those who possess these skills command higher wages, while those with less specialized or obsolete skills may find it harder to secure high-paying employment. Access to quality education, from K-12 through higher education, becomes a crucial determinant of an individual’s earning potential and their ability to bridge this skills gap. Disparities in educational opportunities therefore translate into disparities in income.

Entrepreneurship and Innovation

Entrepreneurship remains a powerful engine for upward mobility and wealth creation. Successful business founders and innovators often generate substantial income and accumulate significant wealth, propelling them into the top income brackets. The US economy’s relatively robust ecosystem for startups and innovation, characterized by access to venture capital and a culture that supports risk-taking, provides avenues for individuals to create entirely new industries and revenue streams. However, entrepreneurship also carries significant risks and is not a guaranteed path to high income.

Strategies for Financial Advancement: Aiming for the Top

While reaching the top 10% income bracket is a challenging feat, it is not an impossible one. For those aspiring to significantly improve their financial standing, a combination of strategic planning, continuous learning, and astute financial management is essential.

Investing in Human Capital: Education and Skill Development

The clearest pathway to higher income is often through investing in oneself. This means:

- Higher Education: Pursuing advanced degrees or certifications in high-demand fields can unlock significantly higher earning potential.

- Continuous Learning: The job market evolves rapidly. Staying current with industry trends, learning new software, programming languages, or management techniques through online courses, workshops, or professional development programs is crucial.

- Specialization: Becoming an expert in a niche area within your field can make you invaluable and command higher compensation.

Strategic Career Planning and Negotiation

Advancing your career effectively is key to increasing income.

- Identify High-Growth Industries: Focus your career trajectory on sectors with strong growth prospects and a high demand for skilled labor.

- Networking: Building a strong professional network can open doors to new opportunities, mentorship, and insights into career advancement.

- Salary Negotiation: Always negotiate your salary and benefits. Research market rates for your role and experience level, and confidently advocate for your worth during job offers and annual reviews.

- Job Mobility: Don’t be afraid to change jobs if it offers a significant jump in salary, responsibility, or growth opportunities, but do so strategically.

Diversifying Income Streams and Smart Investing

Reaching the top 10% often involves more than just a single paycheck; it requires a proactive approach to wealth creation.

- Side Hustles and Entrepreneurship: Explore opportunities to earn extra income outside your primary job, whether through freelancing, consulting, or starting a small business. This can provide additional income and potentially grow into a primary revenue stream.

- Smart Investing:

- Max out Retirement Accounts: Contribute as much as possible to tax-advantaged accounts like 401(k)s and IRAs early and consistently.

- Diversify Investments: Build a diversified portfolio of stocks, bonds, and potentially real estate or other assets. Understand your risk tolerance and invest for the long term.

- Financial Literacy: Educate yourself about personal finance, investing principles, and wealth management strategies. Consider working with a reputable financial advisor.

- Debt Management: Minimize high-interest debt, such as credit card debt, which can significantly hinder wealth accumulation.

- Developing Financial Acumen: Cultivate a mindset of financial discipline, budgeting, saving, and making informed decisions about spending and investment.

Conclusion

The top 10% income in the US represents a significant financial achievement, typically starting around $200,000 for households nationally, though this figure fluctuates widely based on geography and economic conditions. This segment of the population is often characterized by higher education, specialized professional roles in high-growth industries, and a concentration in major metropolitan areas. More than just a number, this threshold reflects a complex interplay of individual effort, access to opportunity, economic trends, and policy frameworks.

For those aspiring to reach this level, the path often involves a commitment to continuous learning, strategic career development, and disciplined financial management, including smart investing and exploring multiple income streams. Understanding these dynamics is crucial, not only for personal financial planning but also for a broader comprehension of economic opportunity and challenges within the United States. While the journey to the top 10% may be demanding, a clear strategy and persistent effort can significantly improve one’s financial trajectory.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.