The acquisition of a Tesla is often framed as a lifestyle choice or a technological leap, but for the savvy consumer, it is primarily a significant financial transaction. Unlike the traditional dealership experience defined by negotiation and inventory markups, buying a Tesla is a streamlined, digital-first process that requires a different kind of fiscal preparation. From navigating the complexities of federal tax credits to calculating the long-term return on investment (ROI) regarding energy savings, purchasing a Tesla is a masterclass in modern personal finance.

In this guide, we will analyze the economic variables of Tesla ownership, ensuring that your transition to sustainable transport is as sound for your bank account as it is for the environment.

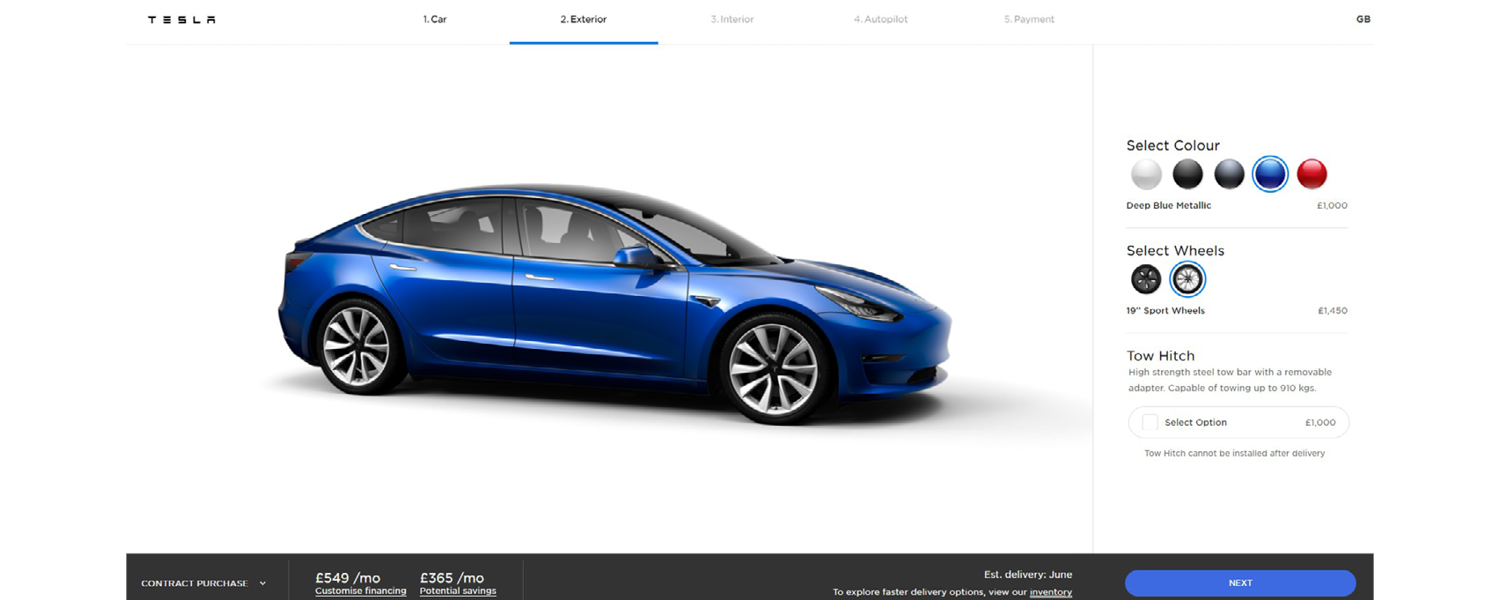

1. Navigating the Direct-to-Consumer Pricing Model

The most jarring difference for first-time Tesla buyers is the “fixed-price” model. Tesla operates without a traditional dealer network, meaning the price you see on the website is the price you pay. From a money management perspective, this eliminates the stress of haggling but requires a precise understanding of how configurations impact your bottom line.

Understanding Base Prices vs. Real-World Costs

When browsing the Tesla inventory, the “price after probable savings” is often the most prominent figure. However, a responsible financial plan must focus on the “Purchase Price.” This includes the base cost of the vehicle, the destination fee, and the order fee. Buyers must distinguish between the Model 3, positioned as an entry-level luxury sedan, and the Model X or S, which represent significant capital outlays. Understanding these price floors is the first step in determining whether the purchase aligns with your debt-to-income ratio.

The Financial Impact of Software and Hardware Upgrades

Tesla’s configuration page is a series of financial forks in the road. Choosing a “Long Range” over a “Rear-Wheel Drive” variant can add $5,000 to $10,000 to the sticker price. More significant is the Full Self-Driving (FSD) capability. As a software-locked feature, FSD is a substantial upfront cost that may not necessarily appreciate at the same rate as the vehicle. Prospective owners must decide whether to buy this feature outright or opt for the monthly subscription model, which allows for better cash flow management and the ability to cancel if the utility does not justify the expense.

2. Maximizing Federal and State Financial Incentives

One of the most compelling “Money” arguments for a Tesla is the suite of government incentives designed to accelerate EV adoption. Leveraging these can effectively shave thousands off the net cost of the vehicle, provided you meet specific fiscal criteria.

The Federal Clean Vehicle Credit

Under the Inflation Reduction Act, many Tesla models qualify for a federal tax credit of up to $7,500. However, this is not a universal discount. From a tax planning perspective, you must ensure your Modified Adjusted Gross Income (AGI) falls below the thresholds: $300,000 for married couples filing jointly or $150,000 for individuals. Furthermore, the vehicle’s MSRP must not exceed $55,000 for sedans or $80,000 for SUVs. For many buyers, the most significant recent change is the “Point of Sale” credit, which allows the $7,500 to be applied directly as a down payment at the time of purchase, rather than waiting for tax season.

State-Level Rebates and Indirect Savings

Beyond federal help, states like California, New York, and Colorado offer additional rebates or tax credits that can range from $500 to $5,000. Additionally, many municipalities offer “Time of Use” (TOU) electricity rates for EV owners, allowing you to charge your car at a significantly reduced cost during off-peak hours. Some regions also offer sales tax exemptions on electric vehicles, which on a $50,000 car, can represent a direct saving of $3,000 to $4,000. Researching these localized financial perks is essential for accurate budget forecasting.

3. Strategic Financing: Loans, Leases, and Cash Flow

How you fund the purchase is just as important as the price of the car itself. Tesla offers internal financing, but it is rarely the only—or best—option for those looking to optimize their interest payments.

Tesla Lending vs. External Credit Unions

Tesla provides an integrated lending experience through its app, often partnering with major banks like Wells Fargo or JPMorgan Chase. While convenient, the interest rates provided by Tesla are often standard market rates. Savvy investors often find better “Green Car Loan” rates at local credit unions. These institutions frequently offer a 0.25% to 0.50% discount on interest rates for electric vehicles. Over a 72-month loan term, this minor difference can save you over $1,500 in interest.

The Buy vs. Lease Analysis

The decision to lease a Tesla involves a unique financial caveat: unlike many other manufacturers, Tesla does not always allow you to buy out the lease at the end of the term (specifically for Model 3 and Model Y). This means a lease is a pure “rental” expense with no hope of building equity. If your goal is to minimize your monthly outflow and you enjoy having the newest tech every three years, leasing is a viable “Money” move. However, if you view a car as a long-term asset, purchasing via a low-interest loan is almost always the superior wealth-building strategy.

4. Total Cost of Ownership (TCO) and ROI

To truly understand “how to buy a Tesla,” one must look past the purchase price and calculate the Total Cost of Ownership (TCO). This is where the financial benefits of an EV become apparent compared to Internal Combustion Engine (ICE) vehicles.

Energy Savings and Charging Infrastructure Costs

The primary driver of ROI in a Tesla is the displacement of gasoline costs. On average, charging a Tesla costs about one-third as much as fueling a comparable gas car. For an individual driving 12,000 miles a year, this can result in annual savings of $1,000 to $1,500. However, the initial “Money” hurdle is the installation of a Level 2 Home Connector. Budgeting $500 to $1,000 for the hardware and $500 to $1,500 for an electrician’s labor is a necessary upfront investment that pays for itself through increased charging efficiency and convenience.

Maintenance and Insurance Premiums

Tesla vehicles have significantly fewer moving parts than traditional cars—no oil changes, spark plugs, or timing belts. This reduces scheduled maintenance costs by roughly 40% over the life of the vehicle. Conversely, insurance for a Tesla can be higher than average due to the high cost of body repairs and the sophisticated sensor suites. Many owners find financial relief through “Tesla Insurance,” a behavior-based program that uses real-time driving data (Safety Score) to determine premiums. For a safe driver, this can result in premiums 20-30% lower than traditional carriers.

5. Depreciation and Resale Value Management

A critical component of any large purchase is the exit strategy. A Tesla is a depreciating asset, but its rate of depreciation is influenced by factors unique to the EV market.

The Impact of Manufacturer Price Adjustments

Tesla is known for sudden, aggressive price cuts on its new inventory to drive volume. While great for new buyers, this can instantly hit the resale value of existing owners. From a financial perspective, the best way to hedge against this volatility is to plan for a long ownership cycle (5–8 years). By holding the asset longer, you allow the fuel and maintenance savings to offset the depreciation hit.

Battery Health as a Valuation Metric

In the used Tesla market, the most significant factor in resale value is “Battery Health.” Much like a high-mileage engine, a degraded battery reduces the car’s worth. To protect your investment, follow optimal charging habits—such as limiting Supercharger use and keeping the charge state between 20% and 80%. A well-maintained battery ensures that when it comes time to sell or trade in the vehicle, you can command a premium price, effectively lowering your lifetime cost of ownership.

Conclusion

Buying a Tesla is more than a simple retail transaction; it is a complex financial maneuver that involves tax strategy, interest rate optimization, and long-term cost analysis. By focusing on the fixed-price model, maximizing government incentives, selecting the right financing vehicle, and understanding the total cost of ownership, you transform a luxury purchase into a strategic financial move. When executed correctly, the transition to a Tesla doesn’t just change the way you drive—it changes the efficiency of your personal balance sheet.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.