Buying a car is a significant financial decision for most individuals and businesses alike. While the sticker price often dominates initial discussions, a more crucial figure—the Annual Percentage Rate (APR)—holds the key to understanding the true cost of financing a vehicle. Far more than just an interest rate, APR encapsulates the comprehensive cost of borrowing, serving as a critical metric for comparing loan offers and making informed financial choices. This guide will demystify APR in the context of car buying, equipping you with the knowledge to navigate the complexities of auto financing and secure the best possible deal.

Understanding the Fundamentals of APR

Before diving into the specifics of car loans, it’s essential to grasp the core concept of APR. It’s a term frequently encountered in personal finance, yet often misunderstood, leading to potentially costly decisions.

Defining Annual Percentage Rate (APR)

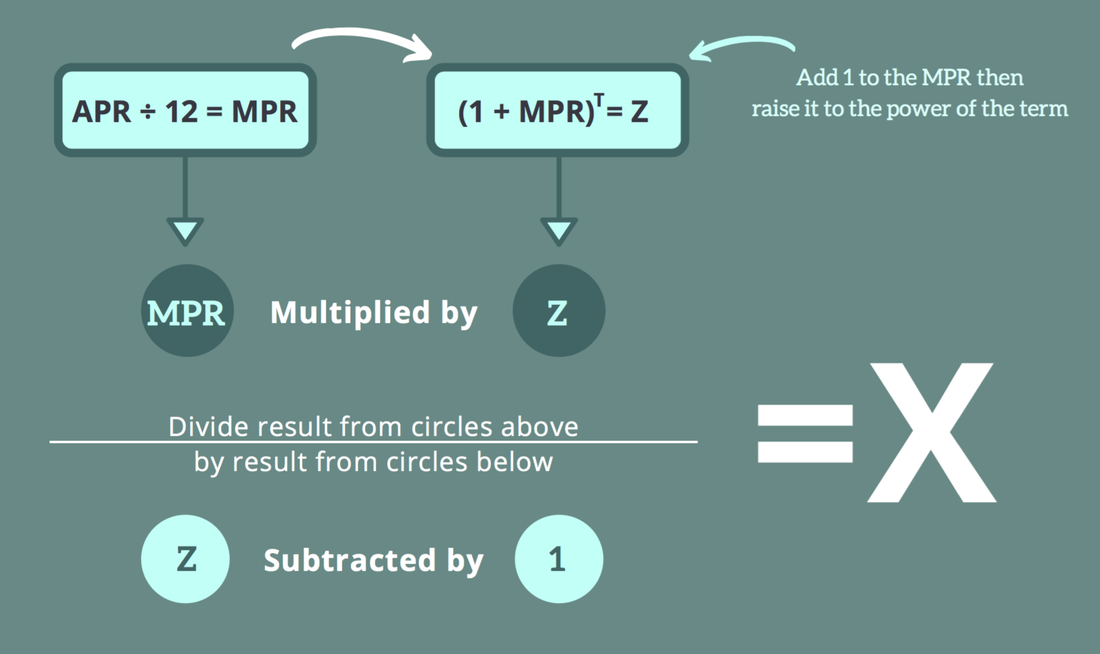

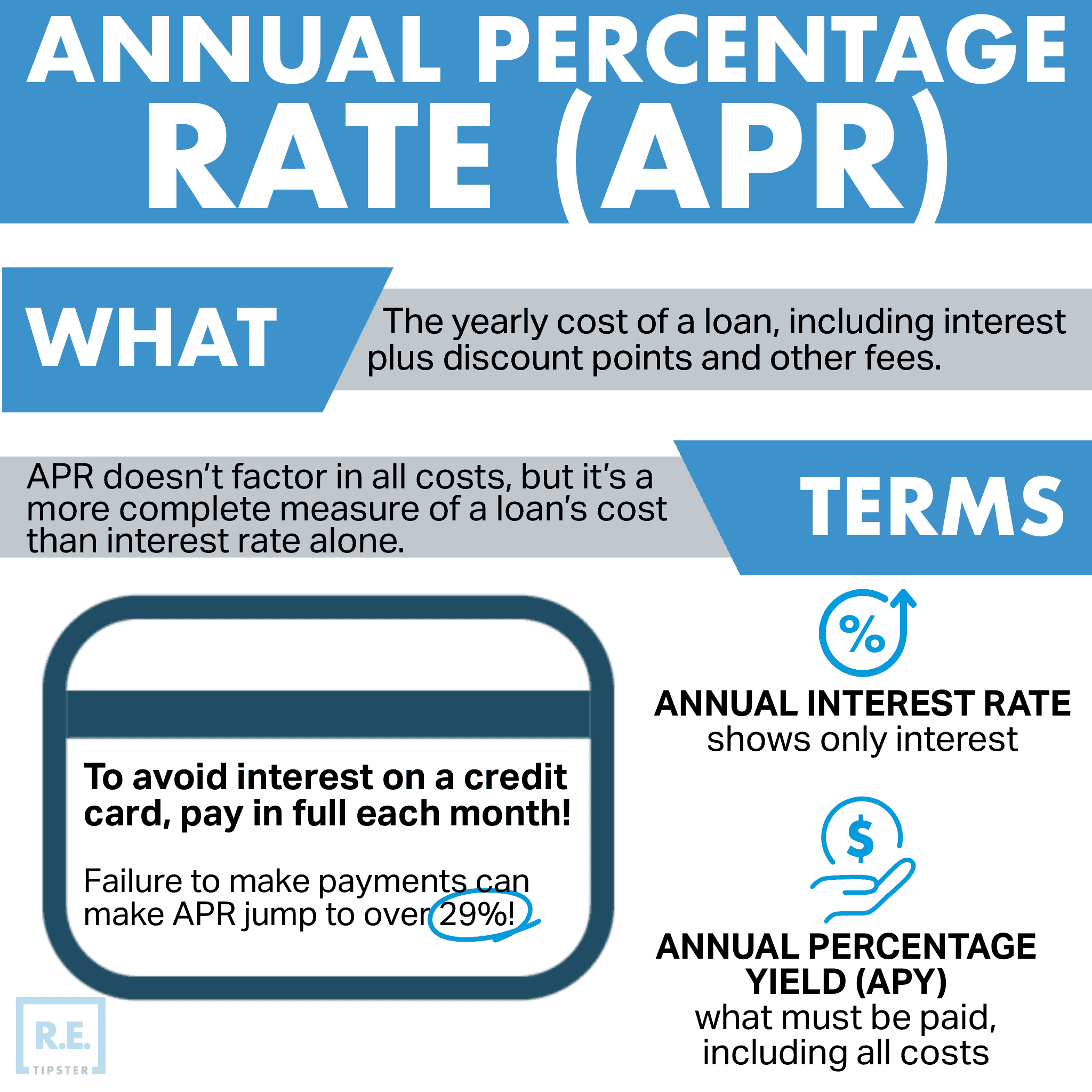

The Annual Percentage Rate (APR) represents the yearly cost of borrowing money, expressed as a percentage. In simple terms, it’s the total interest you pay over the year, plus any additional fees and charges associated with the loan, divided by the loan amount. Unlike a simple interest rate, which only reflects the cost of borrowing the principal, APR provides a holistic view, making it a more accurate measure for comparing different loan products. For car loans, a lower APR translates to lower overall borrowing costs, making it a primary target for savvy buyers.

The Components of APR Beyond Interest

One of the most significant distinctions between APR and a simple interest rate lies in its components. While the interest rate is undeniably the largest factor, APR often includes other charges that can inflate the total cost of your loan. These can vary depending on the lender and the specific loan product, but commonly include:

- Loan Origination Fees: These are charges for processing the loan application.

- Documentation Fees: Costs associated with preparing and handling loan documents.

- Underwriting Fees: Fees for evaluating the borrower’s creditworthiness.

- Certain Brokerage Fees: If a third-party broker facilitates the loan.

- Credit Report Fees: Charges for pulling your credit history.

- Prepaid Finance Charges: Any amount paid by the borrower (or withheld from the loan proceeds) at the time of closing.

It’s crucial to note that not all fees are included in the APR calculation. For instance, late payment fees, appraisal fees for collateral (not typically for car loans), or default charges are generally excluded as they are not fixed costs of obtaining the loan. However, by factoring in the required upfront costs directly related to securing the loan, APR offers a more transparent and standardized way to compare loan offers.

How APR Differs from Interest Rate

The distinction between APR and the nominal interest rate is fundamental. The interest rate is the percentage charged by the lender for the use of borrowed money, applied only to the principal loan amount. If a lender quotes you an “interest rate” of 5%, that’s the base cost of borrowing before other fees are considered.

APR, on the other hand, is designed to give you a more complete picture of the total cost of credit. If the interest rate is 5% but there are significant origination fees, the APR might be 5.5% or 6%. This difference is vital because two loans with the same stated interest rate can have vastly different APRs, and consequently, vastly different total costs, due to varying fees. Always ask for the APR when comparing loan offers to ensure you’re making an apples-to-apples comparison.

The Financial Implications of APR on Your Car Purchase

Understanding APR’s definition is one thing; comprehending its practical impact on your finances is another. The APR directly dictates how much extra you’ll pay above the car’s sticker price over the loan’s lifetime.

The True Cost of Borrowing

The “true cost” of borrowing extends far beyond the principal amount you need for the car. It encompasses all the interest and fees represented by the APR. For a $30,000 car, a 5% APR over 60 months will result in a significantly lower total cost than a 10% APR over the same period. The higher the APR, the more expensive your financing becomes, translating into more money out of your pocket. This extra money could otherwise be saved, invested, or used for other financial goals. It’s a direct reduction in your wealth, highlighting why securing a low APR is paramount.

Impact on Monthly Payments

Your APR has a direct and substantial impact on your monthly car payments. A higher APR means more interest accrues each month, which in turn increases the minimum payment required to service the debt. Even a seemingly small difference in APR—say, 1% or 2%—can translate into dozens of dollars difference in your monthly obligation.

For example, a $30,000 loan over 60 months at a 5% APR might yield a monthly payment around $566. However, at a 7% APR, that payment jumps to approximately $594. While $28 might not seem colossal monthly, it adds up to an extra $1,680 over the loan term. This illustrates how APR influences not just the total cost, but also your immediate cash flow, affecting your budget and financial flexibility.

Total Cost Over Loan Term

The cumulative effect of APR over the entire loan term is where its financial weight truly becomes apparent. The longer the loan term, the more interest you’ll pay, even with a favorable APR. However, a higher APR amplifies this effect exponentially. Over a 5 or 6-year car loan, the difference between a low and high APR can amount to thousands of dollars in additional costs.

Consider again the $30,000 car loan.

- At 5% APR over 60 months, the total interest paid is roughly $3,970.

- At 8% APR over 60 months, the total interest paid is roughly $6,530.

This $2,560 difference is a stark reminder of how significantly APR influences the overall financial burden of your car purchase. Always look at the total cost over the loan term, not just the monthly payment, when evaluating offers.

Factors Influencing Your Car Loan APR

Your eligibility for a specific APR isn’t arbitrary; it’s a calculated decision by lenders based on several key financial indicators and market conditions. Understanding these factors empowers you to improve your standing and negotiate more effectively.

Credit Score: Your Financial Report Card

Your credit score is arguably the most dominant factor influencing the APR you’ll be offered. Lenders use your credit score (e.g., FICO or VantageScore) as a quick indicator of your creditworthiness and your likelihood of repaying the loan.

- Excellent Credit (720+): Borrowers with excellent credit are considered low-risk and typically qualify for the lowest APRs.

- Good Credit (660-719): Still considered low-risk, but might see slightly higher APRs than those with excellent credit.

- Fair Credit (620-659): These borrowers might face moderate APRs, as they represent a slightly higher risk.

- Poor Credit (<620): Borrowers with poor credit are deemed high-risk and will likely be offered significantly higher APRs, if approved at all.

A higher credit score signals a history of responsible borrowing and timely payments, making you a more attractive borrower and justifying a lower risk premium (lower APR) for the lender.

Loan Term Length: Short vs. Long

The duration of your loan also impacts the APR. Generally, shorter loan terms (e.g., 36 or 48 months) tend to come with lower APRs compared to longer terms (e.g., 72 or 84 months). Lenders perceive shorter terms as less risky because there’s less time for economic conditions to change or for the borrower’s financial situation to deteriorate. While longer terms offer lower monthly payments, they often carry a higher APR and result in significantly more interest paid over the life of the loan.

Down Payment and Trade-in Value

Making a substantial down payment or having a valuable trade-in reduces the amount you need to borrow. A smaller loan amount means less risk for the lender, which can translate into a lower APR. A larger down payment also demonstrates your commitment and financial stability. Experts often recommend a down payment of at least 10-20% for a new car to reduce interest costs and minimize the chances of being “upside down” (owing more than the car is worth).

Lender Type and Market Conditions

Different lenders have different risk appetites and business models, leading to variations in APRs.

- Banks and Credit Unions: Generally offer competitive APRs, with credit unions often having a slight edge due to their member-owned structure.

- Captive Finance Companies: These are financing arms of car manufacturers (e.g., Toyota Financial Services, Ford Credit). They often offer promotional APRs (like 0% or very low rates) for new cars to incentivize sales, especially for buyers with excellent credit.

- Dealership Financing: While convenient, dealerships often act as intermediaries, mark up the APR offered by their lending partners to earn a profit. It’s crucial to compare their offer with pre-approvals from other lenders.

- Online Lenders: A growing segment offering competitive rates and streamlined application processes.

Broader market conditions, such as the Federal Reserve’s interest rate policies, also influence the base rates lenders use, subsequently affecting the APRs available to consumers.

Vehicle Type and Age

The type and age of the car you’re buying can also play a role in the APR. Lenders often consider newer cars less risky because they hold their value better and are less likely to require expensive repairs that could strain a borrower’s finances. Used cars, especially older models, might carry slightly higher APRs due to higher perceived risk and faster depreciation. Lenders may also view luxury or performance vehicles differently than standard sedans or SUVs.

Strategies to Secure a Favorable APR

Armed with an understanding of APR and its influencing factors, you can proactively implement strategies to secure the best possible rate for your car loan. This is where diligent financial planning and smart shopping truly pay off.

Improving Your Credit Score

Since your credit score is paramount, taking steps to improve it before applying for a car loan can significantly lower your APR.

- Check Your Credit Report: Obtain free copies of your credit report from Experian, Equifax, and TransUnion. Dispute any errors immediately.

- Pay Bills on Time: Payment history is the most important factor in your credit score. Set up reminders or automatic payments.

- Reduce Debt: Lowering your credit utilization ratio (amount of credit used vs. available credit) can boost your score. Pay down credit card balances.

- Avoid New Credit Inquiries: Opening new credit accounts in the months leading up to a car loan application can temporarily lower your score.

A few points increase in your credit score can save you hundreds, if not thousands, over the life of the loan.

Shopping Around for Lenders

Never take the first loan offer you receive, especially from a dealership. Comparison shopping is vital.

- Get Pre-Approved: Apply for pre-approval from multiple lenders—banks, credit unions, and online lenders—before you even step foot in a dealership. This gives you a clear understanding of the best APR you qualify for.

- Credit Unions: Often offer highly competitive rates due to their non-profit nature.

- Online Lenders: Many reputable online platforms specialize in auto loans and can provide quick quotes.

Gathering multiple pre-approvals within a short timeframe (typically 14-45 days, depending on the credit scoring model) counts as a single inquiry on your credit report, minimizing its impact.

Negotiating Terms

With pre-approval in hand, you gain significant leverage.

- Use Competing Offers: Present your lowest pre-approved APR to the dealership and ask them to beat it. Dealerships have access to multiple lenders and can often match or even slightly improve upon outside offers to secure your business.

- Focus on APR, Not Just Monthly Payment: While a lower monthly payment is appealing, ensure it’s achieved through a lower APR or a reasonable loan term, not by extending the loan term excessively.

Negotiating isn’t just about the car price; it’s also about the financing terms.

Leveraging Down Payments and Trade-ins

Maximize your down payment or trade-in value to reduce the principal amount needing financing.

- Higher Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, making you a less risky borrower and potentially qualifying you for a better APR.

- Negotiate Trade-in Separately: Try to negotiate the trade-in value of your old car as a separate transaction from the new car purchase and financing. This prevents the dealer from obscuring the true value or using it to manipulate other aspects of the deal.

Understanding Loan Pre-qualification vs. Pre-approval

While often used interchangeably, there’s a distinction:

- Pre-qualification: A preliminary check based on basic financial information, providing an estimated rate range. It usually involves a “soft” credit inquiry that doesn’t affect your score.

- Pre-approval: A more thorough review, typically involving a “hard” credit inquiry, which provides a concrete loan offer with a specific APR and loan amount. This is what you need for negotiation leverage.

Always aim for pre-approval to get a firm offer before heading to the dealership.

Common Pitfalls and Smart Decisions

Even with the best intentions, car financing can be fraught with pitfalls. Awareness of these can help you avoid costly mistakes and make smarter financial decisions.

Avoiding Dealer Markups

Dealerships often mark up the interest rates offered by their partner lenders to earn an extra profit, known as a “dealer reserve.” While this is a legitimate business practice, it means you might not be getting the absolute best rate you qualify for. This is precisely why having a pre-approved loan from an external lender is so powerful—it sets a benchmark and empowers you to counter any inflated dealer offers. Always challenge the APR quoted by the dealership if it’s higher than your pre-approval.

Beware of “Too Good to Be True” Offers

Be cautious of extremely low or 0% APR offers, especially on new cars. While these can be genuine, they are typically reserved for buyers with impeccable credit scores (often 750+) and may come with specific conditions, such as shorter loan terms or restrictions on certain vehicle models. Sometimes, a 0% APR offer might mean you forfeit cash rebates or incentives that could ultimately save you more money if you took a slightly higher APR. Always do the math: compare the total cost with the promotional APR vs. a slightly higher APR with additional cash incentives.

The Role of Co-signers and Joint Applicants

If your credit score is not ideal, adding a co-signer with strong credit can significantly improve your chances of approval and help you secure a lower APR. A co-signer legally agrees to be responsible for the loan if you default.

- Co-signer: Primarily acts as a guarantor.

- Joint Applicant: Shares ownership of the car and equal responsibility for the loan.

While beneficial, it’s a significant financial commitment for the co-signer, impacting their credit and potentially their ability to secure future credit. Ensure both parties understand the full implications.

Refinancing Options

If you end up with a higher APR than you’d like, perhaps due to a lower credit score at the time of purchase or poor negotiation, refinancing is often an option. If your credit score has improved, or market rates have dropped since you bought the car, you might qualify for a lower APR by refinancing your existing loan. This could lead to lower monthly payments or a reduced total cost of borrowing. Research lenders that offer auto loan refinancing and compare their APRs against your current loan’s.

In conclusion, the APR is the most critical figure when financing a car, directly impacting your monthly budget and the total financial outlay for your vehicle. By understanding what it is, what influences it, and how to strategically secure the best possible rate, you can transform the car-buying process from a source of anxiety into an empowering financial decision. Approach car financing with diligence, compare offers, and prioritize your long-term financial health over quick convenience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.