In the rapidly evolving landscape of personal finance, the traditional credit card is no longer the sole gatekeeper of purchasing power. The rise of Financial Technology (Fintech) has introduced a variety of flexible spending tools designed to give consumers more control over their cash flow. Among the most innovative of these tools is the Klarna One-Time Use Card. This digital financial instrument combines the security of a virtual card with the flexibility of a “Buy Now, Pay Later” (BNPL) service, allowing users to shop almost anywhere online while maintaining strict budgetary boundaries.

Understanding how to leverage this tool is essential for the modern consumer looking to balance convenience with financial responsibility. This guide provides a deep dive into the mechanics, strategic advantages, and step-by-step processes of using the Klarna One-Time Use Card within a healthy financial ecosystem.

Understanding the Mechanics of Klarna’s One-Time Use Card

Before integrating any new financial tool into your wallet, it is vital to understand its underlying structure. The Klarna One-Time Use Card is a virtual Visa card generated through the Klarna app. Unlike a standard credit card that remains active for years, this card is designed for a single transaction at a specific retailer. Once the purchase is completed, the card number expires, providing a layer of security and financial finality that traditional plastic cannot match.

What is a One-Time Use Virtual Card?

At its core, a virtual card is a digital-only version of a credit or debit card. It comes with a 16-digit number, an expiry date, and a CVV code. The “one-time use” aspect means the card is “burned” or deactivated immediately after the authorized transaction is processed. From a personal finance perspective, this prevents “subscription creep”—where services continue to bill you indefinitely—and ensures that you only spend exactly what you intended for that specific shopping trip.

The Intersection of Fintech and Traditional Credit

Klarna operates on the BNPL model, which essentially provides a short-term, often interest-free loan. When you generate a One-Time Use Card, Klarna pays the merchant in full on your behalf. You, in turn, agree to pay Klarna back, typically in four equal installments over six weeks. This allows for smoother cash flow management, especially for larger necessary purchases, without the high-interest rates associated with revolving credit card debt.

Eligibility and Soft Credit Checks

Unlike applying for a high-limit credit card, which involves a “hard” credit pull that can lower your credit score, Klarna typically performs a “soft” credit check. This allows them to verify your identity and financial standing without impacting your credit report. It is a more accessible entry point for those looking to build a financial history or for those who prefer to keep their credit utilization ratios low on their primary accounts.

Step-by-Step Guide: How to Generate Your Virtual Card

Navigating the Klarna ecosystem is designed to be intuitive, but there are specific financial nuances you must be aware of during the setup process. Because the card acts as a bridge between your bank account and a retailer that may not officially partner with Klarna, the “how-to” involves a few more steps than a standard checkout.

Navigating the Klarna Ecosystem

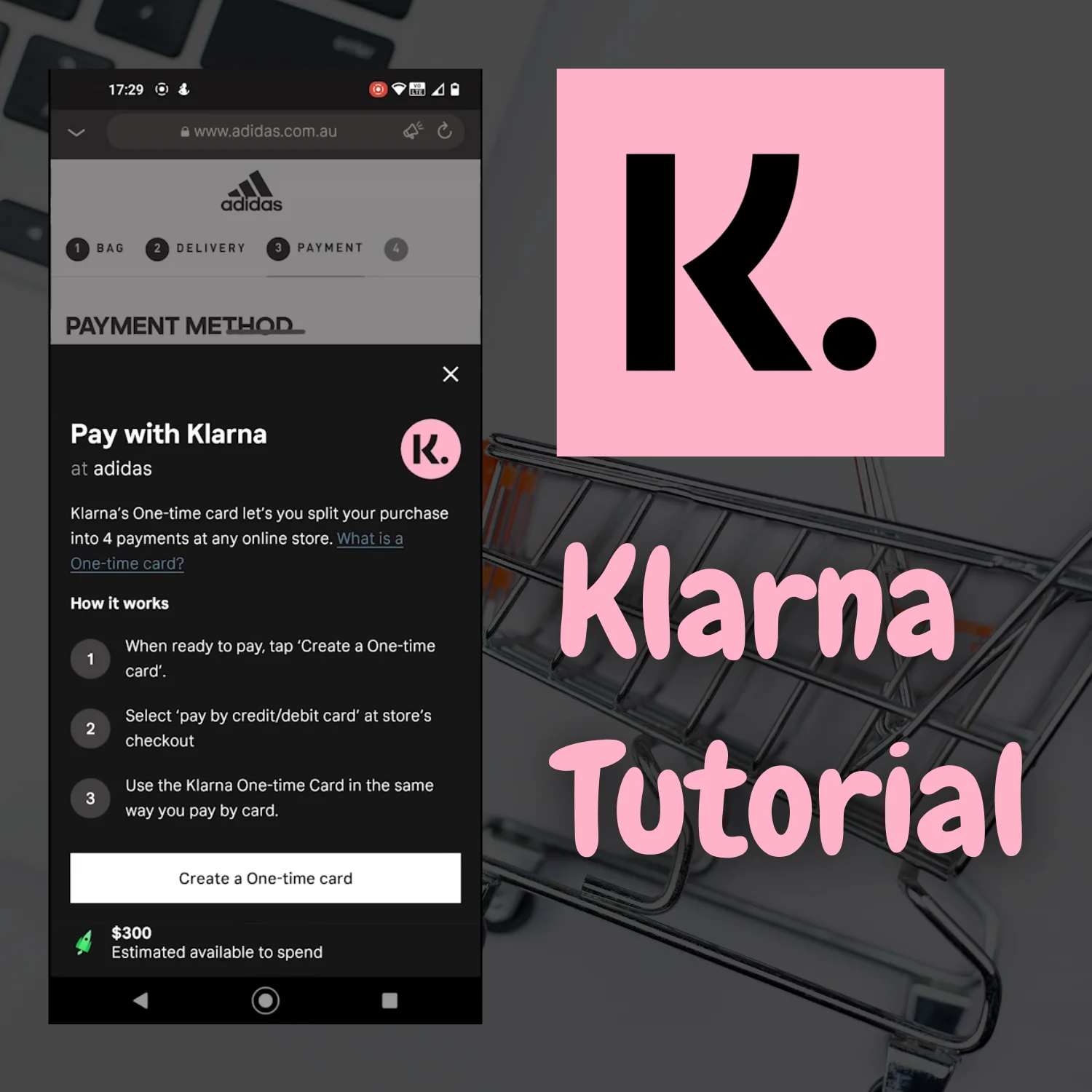

To begin, you must have the Klarna app installed and linked to a valid funding source—usually a debit or credit card. Once logged in, you use the app’s internal browser to find the store where you wish to shop. The One-Time Use Card is specifically designed for retailers that do not have an integrated “Pay with Klarna” button at checkout. By using the Klarna browser, the app “wraps” the retailer’s site, allowing the virtual card to be injected into the payment field.

Setting Your Spending Limit and Creating the Card

Once you have added items to your cart at your chosen retailer, you tap the pink “Pay with K.” button at the bottom of the screen. Here is where strategic budgeting comes into play. You will be asked to enter a “Purchase Amount.” It is wise to include a small buffer for taxes and shipping costs.

For example, if your cart is $92, you might create a card for $100. Klarna will authorize your funding source for the first installment (25% of the total). If the final purchase is only $92, Klarna will automatically adjust the remaining installments and refund the difference from the initial deposit. This “Estimated Total” logic ensures you never overspend your actual budget.

Using the Card at Non-Partnered Retailers

After confirming the amount, the app generates the card details. You then navigate to the retailer’s checkout page and enter these details as you would with any other Visa card. The beauty of this system is its universality; as long as the merchant accepts Visa, you can use the Klarna One-Time Use Card to break your purchase into manageable payments.

Strategic Financial Management with BNPL Tools

While the convenience of “Buy Now, Pay Later” is undeniable, it requires a disciplined approach to personal finance. Using a virtual card is not a license to spend money you do not have; rather, it is a tool for managing the timing of your expenses.

Budgeting and Debt Avoidance

The primary risk of BNPL services is “debt accumulation by a thousand cuts.” Because the individual installments are small, it is easy to lose track of the cumulative total. To use the One-Time Use Card effectively, you should treat each installment as a fixed expense in your monthly budget. Financial experts suggest keeping a dedicated “installment log” to ensure that the total of all your Klarna payments does not exceed 5-10% of your monthly take-home pay.

The Impact on Your Credit Score

While the initial soft credit check doesn’t hurt your score, your behavior afterward can have an impact. In some regions, Klarna may report late payments or defaults to credit bureaus, which can damage your creditworthiness. Conversely, using these tools responsibly and paying on time can demonstrate a pattern of financial reliability. It is a “double-edged sword” that requires diligent oversight.

Managing Repayment Schedules and Autopay

One of the best ways to ensure financial health while using Klarna is to utilize the “Autopay” feature. By aligning your installment dates with your paydays, you ensure that the money is deducted before it can be spent elsewhere. If you find yourself with extra cash, Klarna also allows you to pay off the balance early without penalties, which is a proactive way to reduce your debt-to-income ratio.

Security and Consumer Protection in Digital Transactions

In an era of frequent data breaches, the security benefits of the Klarna One-Time Use Card are as significant as the financial ones. When you use a virtual card, you are practicing a form of “financial obfuscation” that protects your primary bank account.

Why “One-Time Use” Matters for Fraud Prevention

When you provide a merchant with your actual debit card number, that data is stored in their database. If that merchant is hacked, your card details are compromised. With a One-Time Use Card, the data becomes useless the moment the transaction is finished. Even if a hacker steals the card number, there is no balance left to drain and the card is already deactivated. This makes it an ideal tool for shopping at new or less-familiar online boutiques.

Refund Policies and Dispute Resolution

A common concern with virtual cards is the refund process. Fortunately, Klarna’s system is designed to handle this. If you return an item, the merchant refunds the virtual Visa card. Klarna then recognizes this credit and applies it to your remaining balance or refunds your original payment method. Furthermore, Klarna offers “Buyer Protection,” which can act as a secondary layer of insurance if a merchant fails to deliver the goods or services as described.

Integrating Klarna with Digital Wallets

For even greater security and ease of use, Klarna allows users to add their generated cards to Apple Pay or Google Pay. This extends the utility of the One-Time Use Card to physical, “in-store” shopping. This integration ensures that even in a brick-and-mortar environment, you can maintain the same level of budgetary control and digital security that you enjoy online.

The Future of Personal Finance and Virtual Lending

The Klarna One-Time Use Card represents a broader shift in how we interact with money. We are moving away from static, physical assets and toward dynamic, software-defined financial tools.

Moving Beyond Plastic: The Shift to Virtual-First Banking

The decline of physical plastic cards is accelerating. Virtual cards offer a level of customization—such as setting exact spend limits and expiration dates—that physical cards simply cannot match. For the financially savvy individual, these tools provide a granular level of control over every dollar. This shift also reflects a move toward “embedded finance,” where borrowing and payments happen seamlessly within the shopping experience rather than as a separate, cumbersome banking process.

Responsible Borrowing in a Digital Age

Ultimately, the value of a tool like the Klarna One-Time Use Card is determined by the user’s financial literacy. When used as a strategic way to manage cash flow and enhance transaction security, it is a powerful ally. However, it requires a commitment to transparency and self-regulation. By understanding the “how” and the “why” of virtual cards, consumers can navigate the digital marketplace with confidence, ensuring that their shopping habits support, rather than undermine, their long-term financial goals.

In summary, the Klarna One-Time Use Card is more than just a payment method; it is a sophisticated financial tool. By mastering its use, you can enjoy the benefits of modern commerce while maintaining a firm grip on your personal budget and digital security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.