In the landscape of modern finance, few entities command as much gravity as Alphabet Inc. To the casual observer, the name might seem like a corporate abstraction, but to the global investment community, it represents one of the most sophisticated cash-flow engines ever engineered. Alphabet Inc. is the holding company that emerged from a massive corporate restructuring of Google in 2015. While Google remains its most visible and profitable subsidiary, Alphabet serves as the umbrella for a vast portfolio of businesses ranging from life sciences to autonomous driving.

From a “Money” perspective, understanding Alphabet Inc. requires looking past the search bar. It involves analyzing a multi-trillion-dollar market capitalization, a complex dual-class share structure, and a capital allocation strategy that balances the reliable profits of digital advertising with the high-risk, high-reward potential of “moonshot” investments.

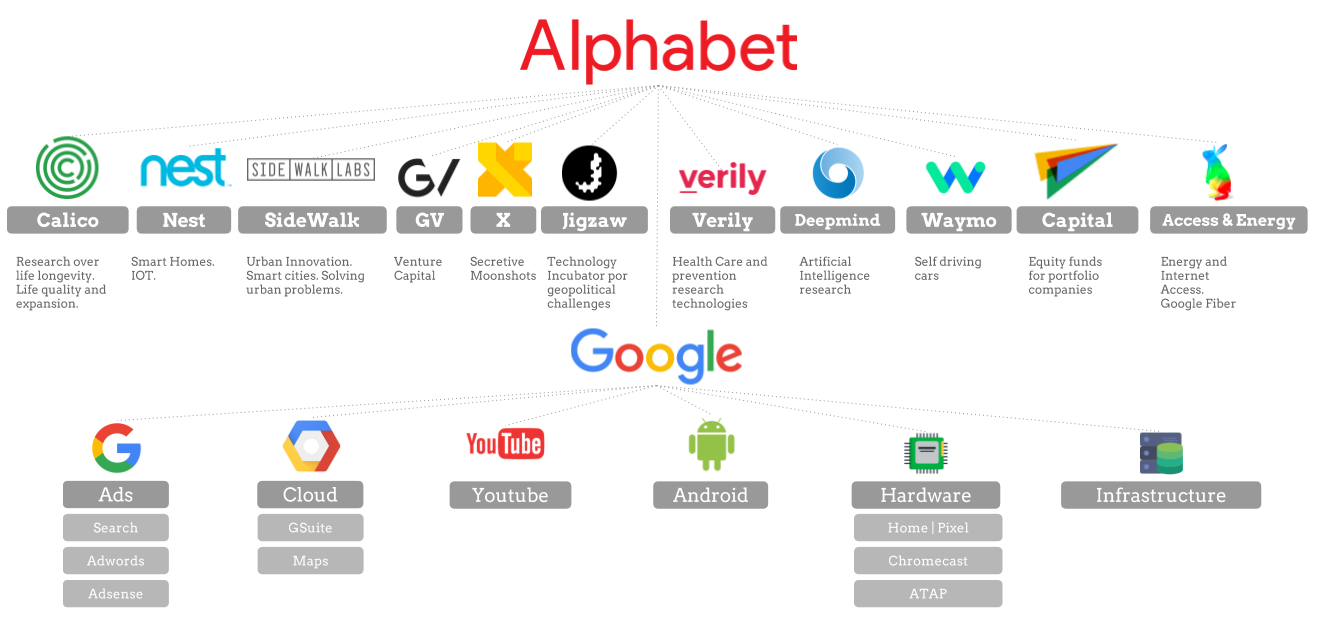

The Conglomerate Structure: Decoding the Alphabet Ecosystem

The transition from Google to Alphabet was not merely a branding exercise; it was a strategic move to provide financial transparency and operational independence to its various business units. Before 2015, Google’s massive search profits often obscured the costs associated with its more experimental ventures. Today, Alphabet’s financial reporting is bifurcated into two primary segments: Google and Other Bets.

Google Services and Cloud: The Core Revenue Drivers

The “Google” segment is the financial bedrock of the corporation. It includes Google Services (Search, YouTube, Chrome, Android, and Google Play) and Google Cloud. For investors, Google Services is the primary interest, as it generates the vast majority of the company’s free cash flow. This segment operates with high margins, leveraging the network effects of billions of users to dominate the global digital advertising market.

Google Cloud, meanwhile, represents the company’s pivot toward enterprise business-to-business (B2B) revenue. While it spent years in a loss-making phase to build out infrastructure, it has recently reached a point of profitability, providing a crucial second pillar for Alphabet’s balance sheet and reducing its historical over-reliance on ad spend.

Why the 2015 Restructuring Mattered for Shareholders

For the investment community, the creation of Alphabet was a landmark event in corporate governance. It allowed Larry Page and Sergey Brin to step back into visionary roles while placing Sundar Pichai at the helm of the core Google business. Financially, this provided “segment reporting,” which allowed analysts to see exactly how much money was being reinvested into “Other Bets.” This transparency helped re-rate the stock, as investors could finally value the core advertising business separately from the speculative ventures, often leading to a higher overall valuation.

Revenue Engines: How Alphabet Generates Billions

To understand Alphabet as a financial entity, one must analyze the mechanics of its income. The company’s revenue model is a masterclass in digital real estate and data monetization. In a typical fiscal year, Alphabet generates over $300 billion in revenue, a figure that rivals the GDP of many mid-sized nations.

The Dominance of Advertising and Search

The lion’s share of Alphabet’s income—roughly 75% to 80%—comes from Google Advertising. This includes Google Search & Other, YouTube ads, and Google Network. The genius of this model lies in its auction-based system. Every time a user searches for a high-intent keyword (like “best car insurance” or “buy gold”), advertisers bid in real-time for that placement. This creates a self-sustaining ecosystem where the price of the “digital real estate” is determined by market demand, ensuring that Alphabet captures the maximum possible value from every click.

YouTube, acquired for a seemingly high $1.65 billion in 2006, has become one of the greatest investments in corporate history. It now generates tens of billions in annual ad revenue while expanding into subscription models like YouTube Premium and YouTube TV, creating a diversified recurring revenue stream within the advertising segment.

Diversification Through Subscription and Hardware

Recognizing the cyclical nature of advertising, Alphabet has aggressively pursued non-ad revenue. This includes “Google Other,” which encompasses hardware (Pixel phones, Nest devices, Fitbit), and Google Play Store commissions. By locking users into an integrated hardware and software ecosystem, Alphabet increases the “lifetime value” of each customer. Furthermore, the growth of subscription services across YouTube and Cloud provides a predictable, monthly cash inflow that helps stabilize the stock price during economic downturns when advertising budgets are typically the first to be cut by corporations.

Investment Strategy and “Other Bets”: The High-Risk Portfolio

Alphabet’s “Other Bets” segment is essentially one of the world’s largest internal venture capital funds. While these businesses currently operate at a cumulative loss, their valuation lies in their potential to disrupt massive industries and become the “next Google.”

Moonshots and Disciplined Capital Allocation

The “Other Bets” segment includes companies like Waymo (autonomous driving), Verily (life sciences), and Wing (delivery drones). For years, critics argued that these were “vanity projects” that burned shareholder cash. However, from a business finance perspective, Alphabet has become more disciplined. Under the leadership of CFO Ruth Porat, the company began seeking external funding for these subsidiaries, bringing in private equity and venture capital firms to validate their valuations and share the financial risk.

Waymo and the Future of Subsidiary Valuation

Waymo is perhaps the most financially significant of the Other Bets. Analysts have estimated its potential valuation in the tens of billions of dollars. By pioneering Level 4 autonomous driving and launching commercial robotaxi services, Waymo represents a massive future revenue stream in the transportation-as-a-service (TaaS) market. For an Alphabet investor, owning the stock is not just a bet on search; it is an indirect stake in a portfolio of pre-IPO-style tech giants that are being incubated using the cash flow from Google’s search engine.

Stock Performance and Shareholder Value: GOOG vs. GOOGL

When an individual decides to invest in Alphabet Inc., they are immediately met with a choice between two primary tickers on the Nasdaq: GOOG and GOOGL. This dual-class structure is a critical component of Alphabet’s corporate identity and its approach to shareholder value.

Understanding the Dual-Class Share Structure

The distinction between the two tickers is primarily about voting rights.

- GOOGL (Class A): These shares carry one vote per share. They are the traditional common stock that allows investors a say in corporate governance.

- GOOG (Class C): These shares have no voting rights. They were created to allow the company to issue stock-based compensation and perform acquisitions without diluting the voting power of the founders, Larry Page and Sergey Brin.

- Class B Shares: These are held exclusively by insiders and carry 10 votes per share. This structure ensures that the founders maintain control over the company’s long-term vision, protecting them from the short-term pressures of activist investors.

Historical Performance and Capital Returns

Alphabet has historically been one of the strongest performers in the S&P 500. For over a decade, the company focused on reinvesting every dollar of profit back into R&D and infrastructure. However, as the company matured, its financial strategy shifted toward returning value to shareholders through massive share buyback programs. By reducing the total number of shares outstanding, Alphabet increases the “Earnings Per Share” (EPS), making the stock more attractive to institutional investors. In 2024, the company reached a new financial milestone by announcing its first-ever quarterly dividend, signaling a transition from a pure “growth” stock to a “growth and income” powerhouse.

The Future Outlook: Balancing Growth with Regulatory Pressures

As we look toward the next decade, Alphabet’s financial health will be determined by its ability to navigate two major forces: the integration of Artificial Intelligence (AI) and the increasing scrutiny from global antitrust regulators.

AI Integration and Capital Expenditure

The rise of Generative AI represents both a threat and an opportunity for Alphabet’s bottom line. To maintain its dominance, Alphabet is investing tens of billions of dollars annually in data centers and specialized AI chips (TPUs). From a money perspective, this “CapEx” (Capital Expenditure) is a double-edged sword. While it secures the company’s future in the AI era, it can temporarily compress profit margins. Investors closely monitor “Cloud margins” and “cost-per-click” metrics to ensure that the transition to AI-powered search doesn’t cannibalize the company’s existing advertising profits.

Navigating Global Antitrust and Financial Risk

Perhaps the greatest risk to Alphabet’s valuation is the regulatory environment. The Department of Justice (DOJ) and the European Union have repeatedly scrutinized Google’s dominance in search and ad-tech. Large-scale fines or mandates to divest certain business units (like Chrome or the Ad-Tech stack) could fundamentally alter the company’s revenue structure. However, many financial analysts argue that even in a “break-up” scenario, the individual parts of Alphabet (YouTube, Search, Cloud) might be worth more as standalone entities than they are as a conglomerate, a concept known as “unlocking the sum-of-the-parts value.”

In conclusion, Alphabet Inc. is much more than a technology company; it is a financial titan. Through its disciplined restructuring, its dominant position in the global advertising market, and its visionary investments in “Other Bets,” it has created a resilient and highly profitable ecosystem. For anyone interested in the intersection of business, finance, and the future of the global economy, Alphabet remains the definitive case study in how to build and maintain a corporate empire in the 21st century.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.