In the landscape of modern personal finance, the seamless movement of money is often taken for granted. Whether you are receiving a paycheck via direct deposit, paying a utility bill online, or sending funds to a friend via a peer-to-peer app, a complex infrastructure of digital identifiers works behind the scenes to ensure your capital reaches the correct destination. At the heart of this infrastructure for JPMorgan Chase customers is the routing number.

Understanding what Chase routing numbers are, how they function, and why a single bank utilizes dozens of different codes is essential for anyone looking to manage their business or personal finances with precision. This guide explores the technical and financial nuances of these nine-digit identifiers, providing the insight needed to navigate the American banking system effectively.

The Fundamental Mechanics of Routing Numbers in Modern Banking

To understand Chase routing numbers, one must first understand the American Bankers Association (ABA) routing transit number (RTN) system. Established in 1910, this system was originally designed to facilitate the sorting and shipping of physical paper checks. Today, it serves as the primary “address” for financial institutions within the United States electronic payment network.

What is an ABA Routing Number?

An ABA routing number is a unique nine-digit code assigned to every financial institution in the United States. It identifies the bank responsible for the funds in a transaction. For a massive entity like JPMorgan Chase, these numbers act as digital zip codes, directing the Federal Reserve’s electronic systems to the specific branch or region where an account is held. Without a routing number, the financial system would have no way of knowing which of the thousands of U.S. banks should receive a specific transfer request.

The Anatomy of a 9-Digit Code

A routing number is not a random string of digits; it is a structured data set. The first four digits represent the Federal Reserve routing symbol, which indicates the geographic district where the bank is located. The next four digits represent the specific financial institution’s unique identifier. The final ninth digit is a “check digit,” calculated using a complex mathematical formula (the Luhn algorithm) to verify that the previous eight digits were entered correctly. This built-in error-checking mechanism prevents millions of dollars from being misrouted due to simple typing errors.

Decoding Chase’s Multi-Routing System

One of the most common points of confusion for Chase customers is the discovery that the bank does not use a single, universal routing number. Because Chase is a “megabank” formed through decades of mergers and acquisitions—including names like Chemical Bank, Washington Mutual, and Bear Stearns—it inherited a vast array of regional infrastructures.

Geographic Distribution and State-Specific Codes

Chase assigns routing numbers based on the state where you originally opened your account. If you opened an account in New York but later moved to California, your routing number will typically remain tied to the New York region unless you close the account and open a new one in your current state.

This geographic fragmentation is a legacy of the era when physical checks had to be cleared through regional Federal Reserve offices. While modern digital banking has made physical distance less relevant, the system remains organized by these regional designations to maintain stability and compatibility with older financial software.

Transaction Types: Wire Transfers vs. ACH

Another critical distinction involves the type of transaction being performed. Chase often utilizes different routing numbers for Automated Clearing House (ACH) transfers and Domestic Wire transfers.

- ACH Transfers: Used for direct deposits, bill payments, and standard transfers between banks. These usually take 1–3 business days.

- Wire Transfers: Used for high-value, immediate transfers that are cleared individually in real-time.

Using an ACH routing number for a wire transfer (or vice versa) is a common financial mistake. It can result in the transaction being rejected, delayed, or subject to additional “correction fees” by the bank.

How to Securely Locate and Use Your Chase Routing Information

Precision is paramount in personal finance. Entering a single digit incorrectly can lead to a “Return to Sender” status on a paycheck or, in worse cases, the accidental transfer of funds to an unintended recipient. Fortunately, Chase provides several secure ways to verify your specific routing details.

Using the Chase Mobile App and Online Portal

The most reliable way to find your routing number is through Chase’s digital platforms. Upon logging into the mobile app or the website, selecting a specific checking or savings account will typically reveal a “See details” or “Account info” link. This section displays both your account number and the specific routing number associated with that account. This is often the safest method, as it accounts for any recent updates or internal bank changes that might not be reflected on older documents.

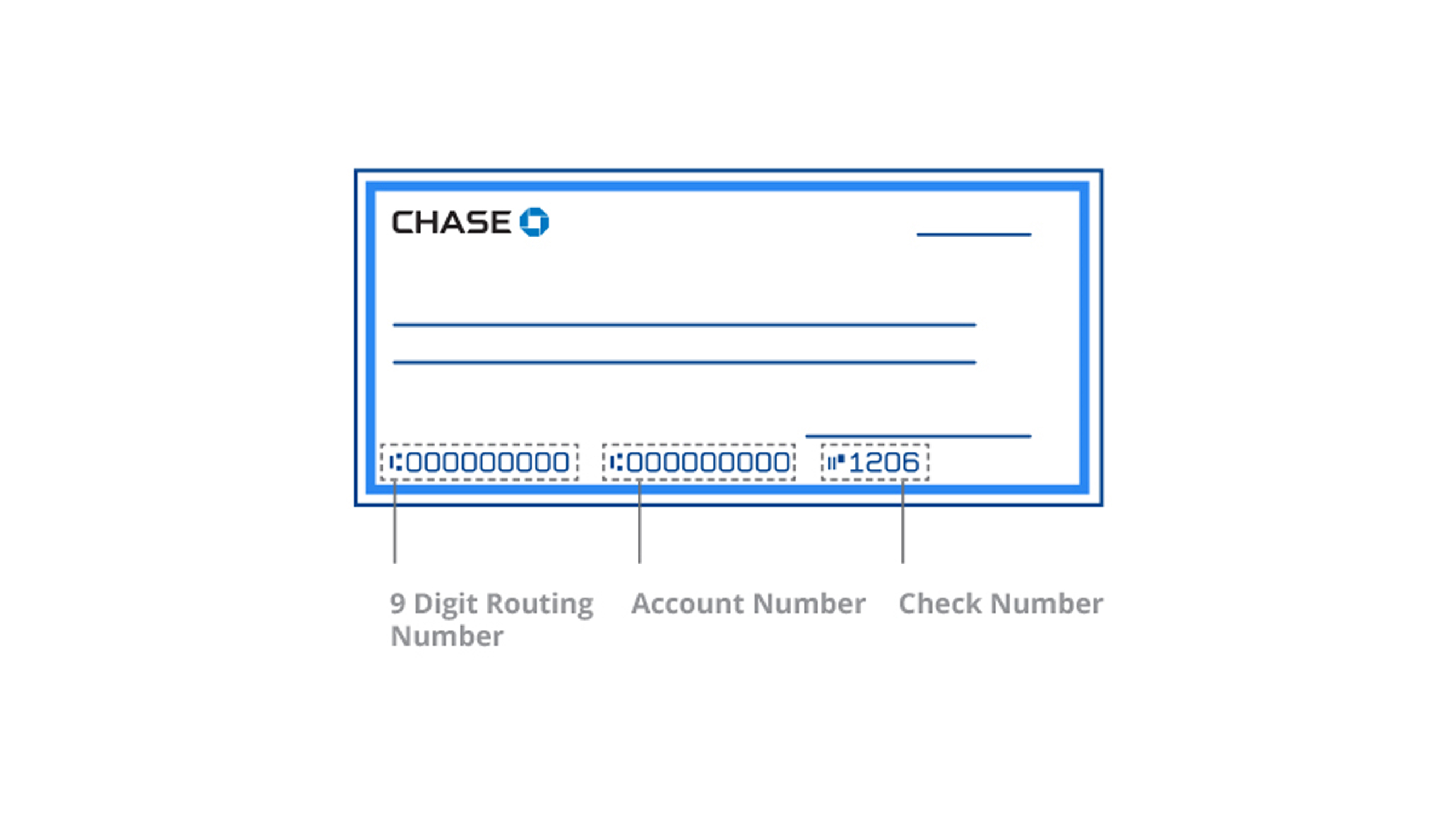

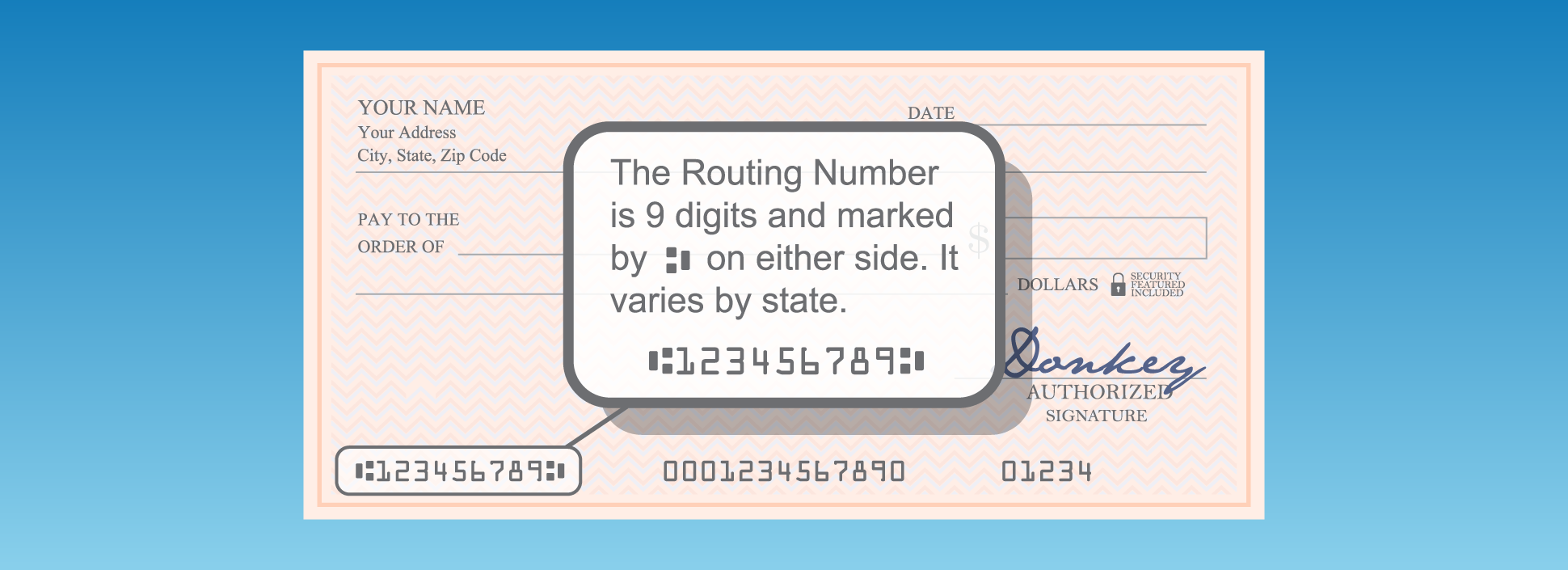

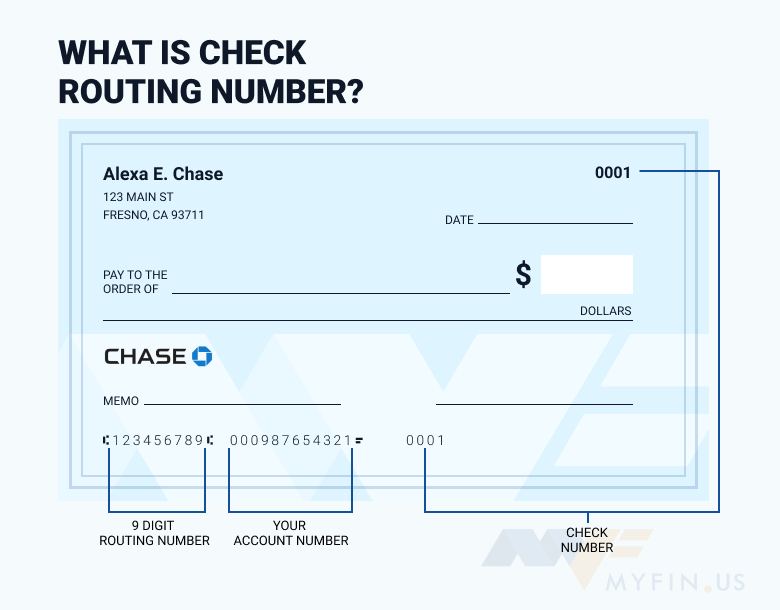

Locating the Number on a Paper Check

For those who still use physical checks, the routing number is readily available at the bottom of the document. Every check contains a string of numbers printed in Magnetic Ink Character Recognition (MICR) font.

- The first sequence (9 digits): This is your routing number.

- The second sequence: This is your unique account number.

- The third sequence: This is the specific check number.

It is important to note that the routing number on a check is designed for ACH and check-clearing processes. If you are setting up a domestic or international wire transfer, the number on your check may not be the correct one to use.

Routing Numbers in the Ecosystem of Digital Finance

As we move toward a more integrated digital economy, the routing number serves as the bridge between traditional brick-and-mortar banking and the world of Financial Technology (Fintech).

Setting Up Direct Deposit and Side Hustles

For employees and freelance professionals, the Chase routing number is the key to automated income. When setting up a direct deposit, your employer requires both the routing number and your account number. This tells the employer’s payroll software exactly which “pipe” to send the money through to reach your “bucket.” This same logic applies to side hustles; platforms like Etsy, Uber, or Airbnb require this information to funnel your earnings into your Chase account.

Integration with Financial Tools and Apps

Modern budgeting and investment tools—such as Mint, YNAB, or Robinhood—frequently use your routing and account numbers to establish a secure link via services like Plaid. By providing your Chase routing number to these apps, you allow for the automated movement of capital into investment vehicles. This connectivity is the backbone of “Online Income” strategies, allowing users to automate their savings and investments without manual intervention.

Risk Management and Financial Security

In the world of business finance and personal wealth management, the security of your banking identifiers cannot be overstated. While a routing number is public information (anyone can look up Chase’s routing numbers online), it becomes a risk when paired with your private account number.

Routing Numbers vs. Account Numbers: The Security Balance

A routing number identifies the bank, while an account number identifies you. Together, they are the keys to your financial vault. Because routing numbers are shared by millions of people, they are not inherently “secret.” However, if a malicious actor gains access to both your routing and account numbers, they can potentially initiate unauthorized ACH withdrawals.

To mitigate this risk, Chase and other major institutions have implemented multi-factor authentication (MFA) and fraud monitoring. However, as a user, you should be cautious about where you enter this information. Only provide your Chase routing and account numbers to trusted, encrypted platforms.

Protecting Your Financial Data from Fraud

One common scam involves “Wire Transfer Fraud,” where a bad actor sends a fake invoice with their own routing and account numbers, posing as a legitimate business or real estate agent. Always verify routing instructions over the phone with a known contact before sending large sums of money. Additionally, regularly reviewing your Chase statement for “Micro-deposits”—small transfers of a few cents used by apps to verify your account—is an excellent way to ensure that only authorized entities are linking to your financial core.

Conclusion: The Anchor of Your Financial Identity

The Chase routing number may seem like a mere string of digits, but it is a sophisticated tool that ensures the stability and fluidity of your financial life. From the regional legacy of the Federal Reserve system to the high-speed requirements of modern wire transfers, these numbers represent the intersection of historical banking traditions and future-facing digital security.

By understanding how to identify, verify, and protect your specific Chase routing number, you empower yourself to manage your money with greater confidence. Whether you are building a business, managing a household, or investing for the future, mastery of these fundamental financial tools is the first step toward long-term fiscal health and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.