In the modern financial landscape, the phrase “I’ll Venmo you” has become synonymous with settling debts, splitting dinner bills, and managing shared household expenses. Since its inception, Venmo has transformed from a niche startup into a cornerstone of personal finance for millions of users. At its core, Venmo is a peer-to-peer (P2P) payment platform that bridges the gap between traditional banking and digital convenience. However, understanding the financial mechanics behind the app—how it handles your money, the fees it charges, and its implications for your personal budget—is essential for any savvy consumer.

The Mechanics of Peer-to-Peer Payments

To understand how Venmo works from a financial perspective, one must first view it as a digital wallet that sits between your traditional bank account and the person you are paying. It acts as an intermediary, facilitating the movement of funds without the delays typically associated with wire transfers or the physical limitations of cash.

Linking Bank Accounts and Cards

The foundation of a Venmo account is its connection to your existing financial ecosystem. Users can link three primary sources of funding: a bank account via ACH (Automated Clearing House), a debit card, or a credit card. From a money management standpoint, the choice of funding source is critical.

Linking a bank account or a debit card is the most cost-effective method for personal finance, as Venmo does not charge a fee for these transactions. In contrast, using a credit card incurs a standard 3% transaction fee. This fee is a pass-through cost from the credit card issuers, and for a disciplined budgeter, it represents an unnecessary expense that should generally be avoided unless in emergencies.

The Venmo Balance vs. Instant Transfers

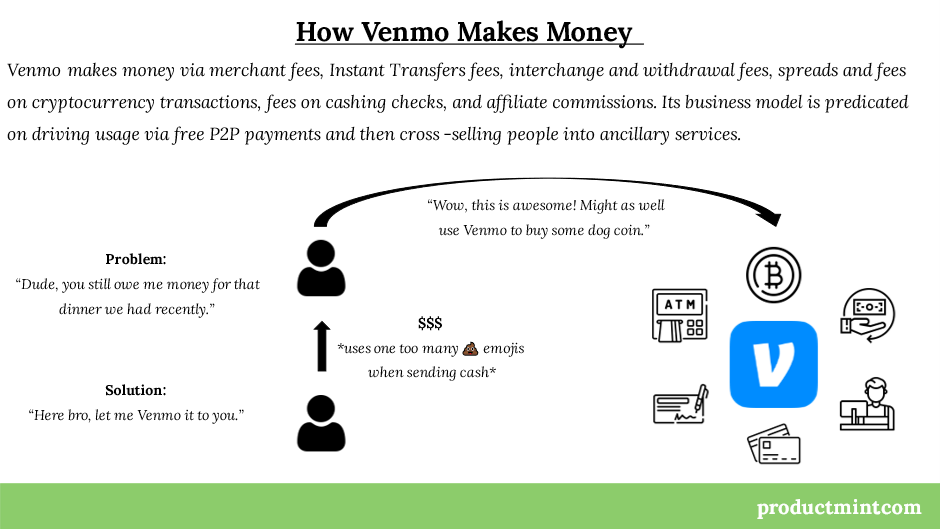

When someone sends you money on Venmo, the funds do not automatically land in your bank account. Instead, they reside in your “Venmo Balance.” This balance represents a digital ledger of funds held by Venmo (and its parent company, PayPal) on your behalf.

You have two choices for what to do with this money: leave it in the Venmo ecosystem to fund future payments, or transfer it out to your bank. If you choose to transfer, you face another financial decision: the Standard Transfer or the Instant Transfer. A Standard Transfer is free but takes one to three business days to clear the ACH network. An Instant Transfer, utilizing the “Original Credit Transaction” (OCT) functionality of debit cards, happens within minutes but costs a percentage of the total amount (currently 1.75%, with a minimum fee of $0.25 and a maximum of $25). For those focused on maximizing their net worth, the Standard Transfer is the superior financial choice, while the Instant Transfer serves as a liquidity tool for urgent needs.

Understanding Costs, Fees, and Limits

While Venmo marketed itself early on as a “free” app, it operates within a complex financial framework that includes various costs and operational limits. Understanding these is vital for maintaining a healthy financial life and avoiding surprises during tax season or large transactions.

Standard vs. Instant Transfer Fees

As mentioned, the 1.75% fee for Instant Transfers is one of Venmo’s primary revenue streams. While a few dollars here and there may seem negligible, frequent users can easily lose hundreds of dollars a year to convenience fees. From a personal finance perspective, these fees are “leaks” in a budget. Planning your cash flow three days in advance to accommodate a Standard Transfer is a simple way to optimize your finances.

Sending Limits and Verification

Venmo is not a bottomless pit of liquidity; it is subject to federal regulations regarding money laundering and fraud. New users typically start with a lower weekly spending limit (often $299.99). Once a user completes the identity verification process—providing their Social Security Number, zip code, and date of birth—the limits increase significantly.

For a verified user, the combined weekly limit for payments and purchases is typically around $60,000, though individual P2P payments are often capped at $4,999.99. Understanding these limits is crucial for users who intend to use Venmo for high-value transactions, such as paying a landlord for a security deposit or purchasing a used vehicle.

Venmo for Business and Side Hustles

As the gig economy has grown, Venmo has expanded its reach into the realm of business finance. This shift has introduced new tools for entrepreneurs but also new responsibilities regarding financial reporting and transaction protection.

Professional Profiles and Tax Implications

For freelancers, consultants, and small business owners, Venmo offers “Business Profiles.” Unlike personal accounts, business profiles allow users to accept payments for goods and services formally. However, this comes with a transaction fee (typically 1.9% plus $0.10).

From a money management perspective, the biggest shift in recent years involves IRS reporting requirements. Under current tax laws, payment processors like Venmo are required to report gross payments for goods and services that exceed a certain threshold (historically $600) by issuing a Form 1099-K. This means side hustlers must be diligent in their bookkeeping. Using a dedicated Business Profile ensures that personal gifts from friends are not conflated with taxable business income, simplifying the tax-filing process at year-end.

Transaction Protection for Goods and Services

When you send money via a personal Venmo account, the transaction is generally considered “final” and “unprotected,” much like handing someone a twenty-dollar bill. However, when paying a Business Profile—or marking a personal payment as “Goods and Services”—the transaction may be covered by Venmo’s Purchase Protection Program. This program can provide a refund if an item doesn’t arrive or is significantly different than described. For the consumer, paying the small fee associated with a business transaction can be viewed as an insurance premium against fraud.

Integrating Venmo into Your Personal Finance Strategy

Venmo is no longer just a way to pay someone back for coffee; it is a multi-faceted financial tool that can be integrated into a broader wealth-management strategy.

Budgeting with the Venmo Debit and Credit Cards

To compete with traditional banks, Venmo offers a physical Debit Card (linked to your Venmo balance) and a Credit Card. The Venmo Debit Card is an excellent tool for those who want to “bucket” their spending. By keeping a specific amount of “fun money” in your Venmo balance and using the debit card for social outings, you can effectively wall off your discretionary spending from your primary checking account.

The Venmo Credit Card takes this a step further by offering a tiered cash-back system (3% on your top spend category, 2% on the second, and 1% on others). For many, the “Top Category” might be dining or groceries. If managed responsibly—meaning the balance is paid in full every month—the cash back can be funneled directly into the user’s Venmo balance or even used to purchase cryptocurrency within the app, turning a liability (spending) into a small asset (rewards).

Security Measures for Protecting Your Wealth

Financial tools are only as good as the security protecting them. Because Venmo is directly linked to your bank account, it is a high-value target for bad actors. To safeguard your money, several best practices are recommended:

- Enable Multi-Factor Authentication (MFA): Ensure that any login attempt requires a secondary code sent to your mobile device.

- Use a PIN or Biometric Lock: Even if someone gains physical access to your phone, they should not be able to open the Venmo app without a fingerprint or code.

- Privacy Settings: By default, Venmo transactions are public. From a financial privacy standpoint, it is wise to set your transactions to “Private.” This prevents strangers (or even friends) from seeing your spending habits, which can be used in social engineering scams.

In conclusion, Venmo works by simplifying the movement of money, but its simplicity masks a sophisticated financial ecosystem. By understanding the flow of funds, the structure of its fees, and the requirements of its business tools, users can move beyond simple transactions and start using Venmo as a strategic component of their financial lives. Whether you are splitting a bill or running a side business, the key is to remain aware of the costs and to use the platform’s features to enhance, rather than complicate, your personal finance journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.