In an increasingly digital world, where transactions often happen with a tap or a click, the physical check might seem like a relic of a bygone era. Yet, checks continue to play a vital role in personal and business finance, serving as a tangible record of transactions, a means for secure payments, and a foundational element of our banking system. At first glance, a check appears straightforward: a space for the payee, an amount, a date, and a signature. However, the true operational power and security of a check lie in the often-overlooked sequence of numbers printed along its bottom edge. These magnetic ink character recognition (MICR) numbers are not just random digits; they are a critical financial language, providing the essential instructions for banks to process funds accurately and securely.

Understanding these bottom numbers is more than just a matter of trivia; it’s a fundamental aspect of financial literacy. From setting up direct deposit and paying bills online to safeguarding against fraud and managing business expenses, knowing what each segment of these numbers represents empowers you to navigate your financial life with greater confidence and control. This article will delve deep into the anatomy of a check’s bottom line, demystifying the routing number, account number, and check number, explaining their significance, and offering practical insights into their use and protection in both traditional and digital financial landscapes.

The Essential Trio: Understanding MICR Lines

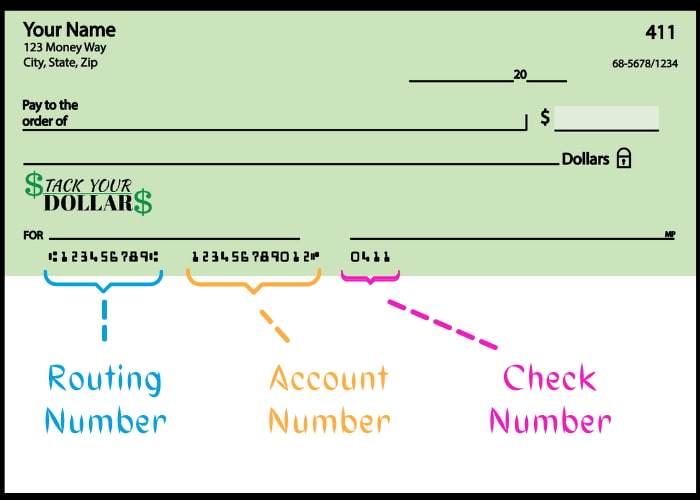

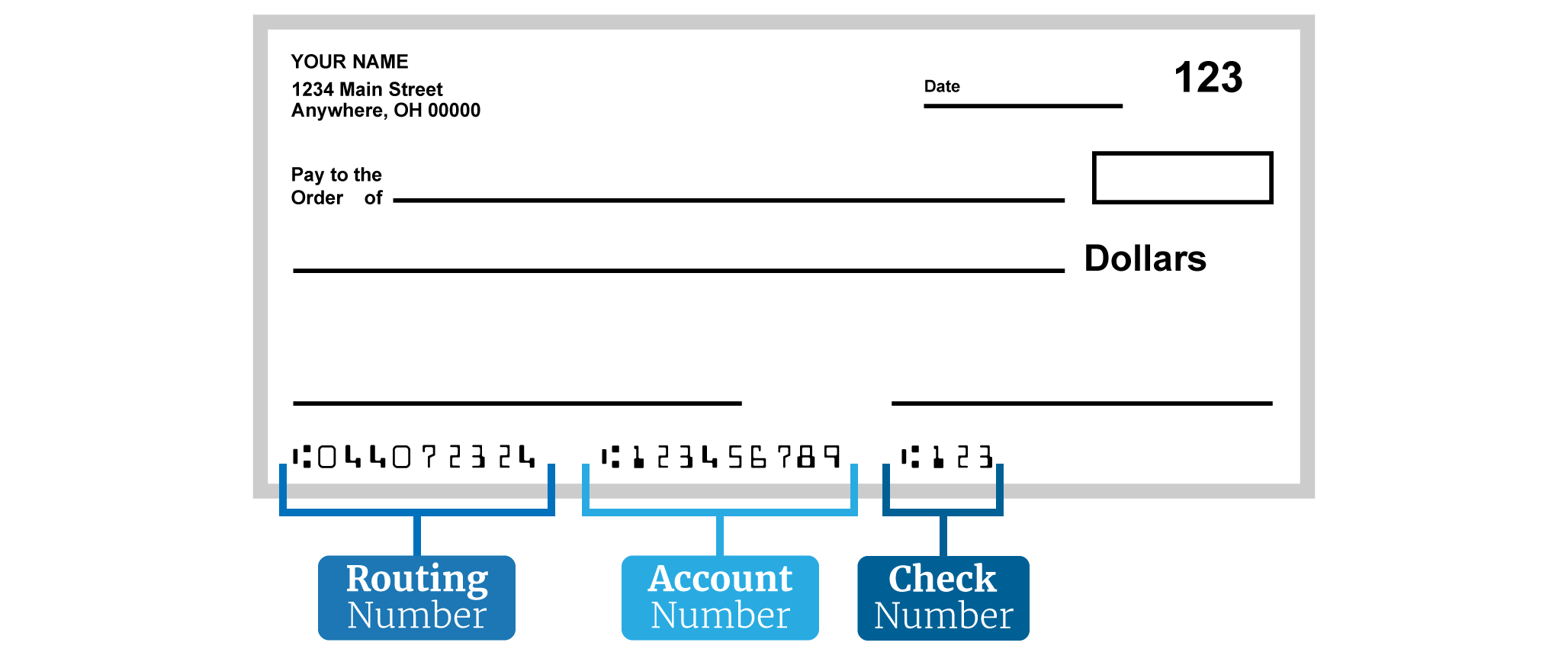

The string of numbers at the bottom of a check, printed in a distinct font using magnetic ink, is known as the Magnetic Ink Character Recognition (MICR) line. This specialized printing allows high-speed scanners to read the information quickly and accurately, even if the check is slightly crumpled or creased. The MICR line is universally structured and comprises three distinct, crucial pieces of information that facilitate the entire check processing system.

The Routing Number: Your Bank’s Digital Address

The routing number, also known as an ABA (American Bankers Association) routing transit number, is typically the first set of nine digits on the far left of the MICR line. Think of it as your bank’s unique digital address within the vast network of financial institutions. Every bank or credit union in the U.S. has at least one routing number, though larger banks may have several for different regions or types of transactions.

This number serves a singular, critical purpose: to identify the financial institution that holds the account from which the funds are being drawn. When you write a check, the routing number tells the recipient’s bank exactly where to send the request for funds. Similarly, when setting up direct deposit, electronic bill payments, or ACH (Automated Clearing House) transfers, the routing number ensures that funds are directed to the correct bank. Without it, transactions would be lost in a financial labyrinth, unable to find their intended destination. It’s a cornerstone of the modern payment system, enabling the efficient flow of money between different banks and accounts across the country.

The Account Number: Your Unique Financial Identifier

Immediately following the routing number, or sometimes sandwiched between the routing and check numbers, is your individual bank account number. This sequence of digits is unique to your specific checking account at your financial institution. While the routing number identifies the bank, the account number identifies you (or your business) within that bank.

The length of an account number can vary significantly from one bank to another, often ranging from 10 to 12 digits, but sometimes more. This number is your personal key to accessing funds and managing transactions. It’s used in conjunction with the routing number for virtually all electronic transfers, including direct deposits of paychecks or government benefits, automatic withdrawals for loan payments or utilities, and initiating wire transfers. Because it directly identifies your funds, the account number is a highly sensitive piece of information that requires careful protection to prevent unauthorized access or fraudulent activity. Its uniqueness ensures that your money is credited or debited from precisely the right place, safeguarding the integrity of your personal or business finances.

The Check Number: Tracking Your Transactions

The check number, typically the last set of digits on the MICR line (and also printed in the upper right-hand corner of the check), serves as a sequential identifier for each individual check within your checkbook. It’s usually a three- or four-digit number that allows you to keep an organized record of the checks you’ve issued.

While the routing and account numbers are static for your account (unless you change banks or account types), the check number changes with each new check you write. Its primary function is for personal record-keeping and reconciliation. When you record a check in your check register or banking app, you list it by its check number, along with the date, payee, and amount. This enables you to track cleared checks, identify missing transactions, and reconcile your bank statements with ease. Furthermore, in the event of a dispute or fraud, the check number provides a specific reference point for investigations. From a financial perspective, consistent tracking of check numbers is a crucial habit for maintaining accurate financial records and gaining a clear understanding of your spending and payment history.

Why These Numbers Matter: Security, Transactions, and Verification

The MICR line isn’t merely a technical detail; it’s the operational backbone of check-based financial transactions. The precise identification offered by these numbers is fundamental to the speed, accuracy, and security of how money moves within the banking system. Their importance extends beyond traditional paper checks into the realm of digital banking and fraud prevention.

Facilitating Seamless Payments

At the core, the bottom numbers on a check enable seamless payment processing. When a check is deposited, bank tellers or automated systems scan the MICR line. This instant digital reading extracts the routing number to identify the paying bank, the account number to pinpoint the specific payer’s account, and the check number for tracking. This automated process vastly speeds up what would otherwise be a labor-intensive, manual reconciliation task, significantly reducing the time it takes for funds to clear and become available. For businesses, this efficiency translates into quicker access to receivables, improved cash flow, and streamlined accounting. For individuals, it means faster payment for services and reliable direct deposits.

Preventing Fraud and Ensuring Security

The design of the MICR line also plays a critical role in financial security. The use of magnetic ink makes it difficult for ordinary printers to replicate, adding a layer of protection against counterfeiting. While not foolproof, it makes it harder for fraudsters to create realistic-looking fake checks that would fool bank processing systems. More importantly, the precise identification of both the bank and the specific account minimizes the chances of funds being misdirected.

Banks employ sophisticated algorithms and human oversight to monitor transactions and look for anomalies related to these numbers. For instance, if a check is presented with a valid routing number but an invalid account number, or if a sequence of check numbers appears out of order, it can flag the transaction for further investigation, potentially stopping fraudulent activity before it causes financial harm. Understanding your own account numbers and regularly reviewing statements allows you to act as an additional line of defense, quickly identifying unauthorized transactions.

The Role in Digital Banking and ACH Transfers

Even as paper checks decline, the underlying principles of the MICR line numbers remain crucial for digital transactions. When you set up online bill pay, direct deposit, or initiate an ACH transfer (like paying a utility bill directly from your bank account), you’re typically asked for your bank’s routing number and your account number. These electronic transfers rely on the same unique identifiers to ensure funds are debited from and credited to the correct accounts.

ACH transfers, which form the backbone of many modern digital payment systems (like Venmo or PayPal when linking a bank account), leverage these numbers to move money between accounts without the need for a physical check. Understanding where to find these numbers on a physical check is therefore a gateway to confidently utilizing various digital financial tools, enabling you to manage your money efficiently in a largely paperless environment. It bridges the gap between traditional banking and the evolving digital finance landscape.

Beyond the Basics: Practical Applications and Common Scenarios

Knowing what the bottom numbers represent is just the first step. Their true value lies in their practical application in various personal and business financial scenarios. From automating regular payments to navigating unexpected situations, these numbers are your guide.

Setting Up Direct Deposit and Bill Pay

Perhaps the most common modern application of routing and account numbers is in setting up direct deposit and automatic bill payments. For direct deposit of your paycheck, tax refund, or government benefits, your employer or the relevant agency will require your bank’s routing number and your specific account number. This ensures that your funds are transferred electronically and securely into your designated account without the need for a physical check. Similarly, when you set up online bill pay with a utility company, credit card issuer, or any other service provider, you’ll typically provide these same numbers to authorize recurring debits from your account. This automation simplifies financial management, reduces the risk of late payments, and often provides quicker access to funds compared to waiting for a physical check to clear.

Voiding a Check: When and How

There are instances when you might need to “void” a check. This is often done when setting up direct deposit or automatic payments, where a voided check serves as verification of your routing and account numbers without actual funds being transferred. To void a check, you simply write the word “VOID” in large letters across the front of the check, ensuring it covers the signature line, the payee line, and the amount box. Crucially, do not write over the MICR line at the bottom. The MICR numbers need to remain perfectly legible if the check is being used to verify your account information, as it will likely still be run through an electronic scanner. Voiding a check renders it unusable for payment while still providing the necessary banking details, making it a safe and accepted practice for verifying account information without incurring financial risk.

Reading a Check in the Digital Age: Mobile Deposits and Online Banking

Even with the rise of digital banking, the physical check and its associated numbers haven’t completely disappeared. Mobile deposit features in banking apps, for example, rely on sophisticated optical character recognition (OCR) technology to scan and interpret the information on a check, including the MICR line. When you snap a picture of a check for mobile deposit, the app is digitally “reading” those bottom numbers to correctly route the funds to your account and verify the paying bank’s information.

Furthermore, your online banking portal allows you to access your routing and account numbers for various purposes, often under a “Account Details” or “Direct Deposit Info” section. While a physical check might be less common, the digital representations of its core identifiers are more pervasive than ever. Understanding how to locate these numbers, whether on a paper check or within your banking app, is essential for a seamless experience in today’s hybrid financial world.

Protecting Your Information: Best Practices for Check Security

Given the critical nature of the routing and account numbers, safeguarding this information is paramount to protecting your financial security. These numbers are a direct gateway to your funds, and their compromise can lead to significant financial distress.

Safeguarding Your Physical Checks

The first line of defense is securing your physical checks. Treat your checkbook like cash or a credit card. Keep it in a safe, private place where it cannot be easily accessed by others. Avoid leaving checks lying around in open areas at home or work. When carrying checks, be discreet. If your checks are stolen, fraudsters can use the routing and account numbers to create counterfeit checks, set up unauthorized debits, or even attempt to impersonate you. Always keep track of your check numbers and reconcile them with your bank statements. If you notice any checks missing or an unfamiliar transaction, report it to your bank immediately. When disposing of old checks or statements, always shred them to prevent information from falling into the wrong hands.

Digital Security for Banking Information

In the digital realm, protecting your banking details is equally important. Only share your routing and account numbers with trusted entities, such as your employer for direct deposit, legitimate bill pay services, or reputable financial institutions. Be extremely wary of unsolicited requests for this information via email, text message, or phone calls, as these are common tactics for phishing scams. Always verify the authenticity of the requestor through an independent channel (e.g., calling the company directly using a number from their official website, not one provided in a suspicious email).

Ensure you use strong, unique passwords for all your online banking accounts and enable two-factor authentication (2FA) whenever possible. Regularly monitor your bank statements and transaction history for any unauthorized activity. Be mindful of public Wi-Fi networks when accessing sensitive financial information, as they can be vulnerable to eavesdropping.

What to Do If Your Check Information Is Compromised

Despite best efforts, financial information can sometimes be compromised. If you suspect your check numbers (routing and account numbers) have been stolen or used fraudulently, act quickly.

- Contact Your Bank Immediately: Report the potential fraud to your bank. They can place alerts on your account, monitor for suspicious activity, and guide you through the process of stopping payments or closing compromised accounts.

- Monitor Your Accounts: Keep a close eye on all your financial accounts, not just the one directly affected, for any unauthorized transactions.

- File a Police Report: For significant fraud, consider filing a report with your local police department. This can be helpful for insurance claims or future investigations.

- Notify Credit Bureaus: Consider placing a fraud alert on your credit reports with Equifax, Experian, and TransUnion. This makes it harder for identity thieves to open new accounts in your name.

- Change Passwords: If any associated online accounts might have been compromised, change your passwords immediately.

Prompt action is crucial in mitigating the damage from compromised financial information, underscoring the importance of understanding and protecting these foundational banking identifiers.

The Future of Checks: Evolving Payment Landscape

The financial world is in constant flux, with new technologies and payment methods continuously emerging. While paper checks have seen a decline in usage, their core identifiers and the principles they represent continue to underpin many modern financial processes.

The Decline of Paper Checks and Rise of Digital Payments

Over the past two decades, the use of paper checks has significantly decreased, largely supplanted by more convenient and faster digital payment methods. Online banking portals, mobile payment apps, peer-to-peer payment services (like Venmo, Zelle, PayPal), credit and debit cards, and automated clearing house (ACH) transfers have revolutionized how individuals and businesses exchange money. These digital solutions offer instantaneous transactions, enhanced tracking, and often greater security protocols. The shift away from paper checks is driven by consumer preference for convenience, environmental concerns, and the inherent efficiencies of digital processing.

Checks in a Hybrid Financial World

Despite this decline, paper checks are unlikely to disappear entirely in the near future. They continue to serve niche but important roles. For instance, checks are often used for large one-time payments (e.g., down payments on a house, insurance payouts), situations requiring a physical proof of payment, or when one party doesn’t have access to digital banking. Many businesses still rely on checks for payroll or vendor payments. Furthermore, in certain industries or among specific demographics, checks remain a preferred or necessary payment method. Thus, we operate in a “hybrid” financial world where traditional methods coexist with digital innovations. Understanding the mechanics of a check, particularly its bottom numbers, remains a valuable skill for navigating this diverse payment ecosystem.

Understanding Financial Literacy in a Changing Environment

The evolving payment landscape underscores the critical importance of adaptable financial literacy. While the physical act of writing a check may become less frequent, the underlying concepts of routing numbers, account numbers, and secure transaction processing are more vital than ever. These identifiers form the basis of most electronic money movement. Being financially literate in this new environment means understanding how to:

- Safely use your routing and account numbers for digital payments.

- Distinguish between secure and insecure platforms for financial transactions.

- Protect your digital identity and banking credentials.

- Leverage various payment methods strategically for personal and business efficiency.

The “bottom numbers on a check” are more than just ink on paper; they are a fundamental language of finance that has adapted and endured. Mastering this language equips you with the knowledge to manage your money effectively, securely, and confidently, irrespective of whether your next transaction is with a pen or a tap.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.