In the contemporary financial landscape, the phrase “Venmo me” has become as ubiquitous as “Google it.” Since its inception, Venmo has transformed from a simple SMS-based payment system into a cornerstone of the modern digital economy. For those navigating the complexities of personal finance, understanding “how to do Venmo” is no longer just about splitting a pizza bill; it is about managing a versatile financial tool that bridges the gap between traditional banking and the fast-paced world of digital transactions. This guide explores the multifaceted nature of Venmo through a financial lens, focusing on its utility in personal budgeting, business operations, and long-term wealth management.

1. The Fundamentals of Venmo in Personal Finance

At its core, Venmo is a peer-to-peer (P2P) payment platform that allows users to transfer funds using a mobile app. However, to use it effectively within a broader financial strategy, one must understand how it interacts with established banking institutions.

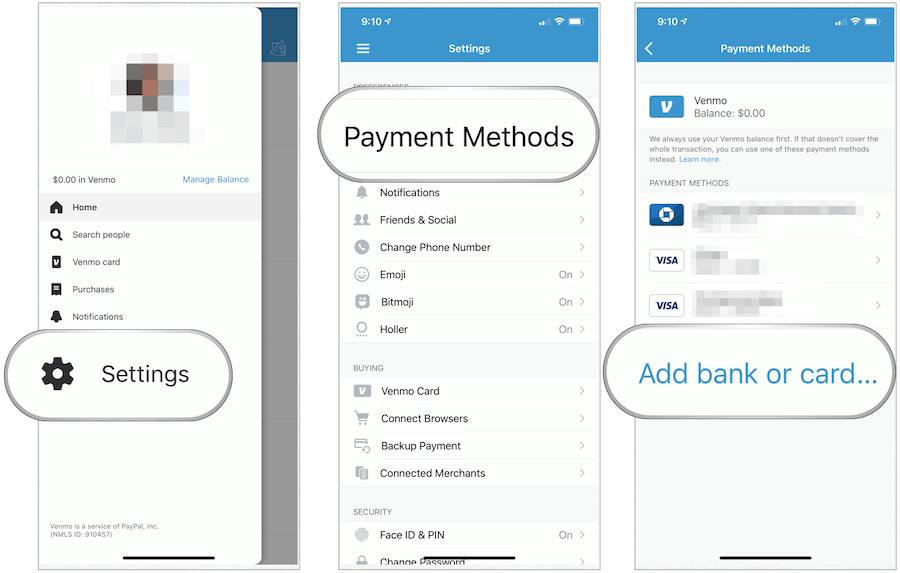

Setting Up Your Digital Wallet

The first step in mastering Venmo is the strategic setup of your account. Unlike a traditional bank account, Venmo operates as a “digital wallet.” When you receive money, it sits in your Venmo balance rather than automatically moving to your bank. From a financial management perspective, it is crucial to decide whether to treat this balance as “mad money” or to discipline yourself to transfer it immediately to a high-yield savings account. Linking your account requires a verified phone number and email, followed by the attachment of a funding source.

Linking Banks vs. Credit Cards: Impact on Your Bottom Line

One of the most critical financial decisions a Venmo user makes is choosing a primary funding source. Venmo allows you to link bank accounts, debit cards, and credit cards.

- Bank Accounts and Debit Cards: Transfers from these sources are free. For the budget-conscious user, this is the gold standard.

- Credit Cards: Venmo charges a 3% fee for payments made via credit card. From a wealth-building perspective, this is a significant leak. Unless you are chasing a specific sign-up bonus that outweighs the 3% fee, using a credit card on Venmo is generally a poor financial move. Furthermore, some issuers treat Venmo transfers as “cash advances,” which carry even higher interest rates and no grace period.

Managing Transfers and Liquidity

Venmo offers two ways to move money to your bank: the Standard Transfer and the Instant Transfer.

- Standard Transfer: This is free and typically takes 1–3 business days. For those who plan their cash flow, this is the preferred method.

- Instant Transfer: For a fee of 1.75% (with a minimum of $0.25 and a maximum of $25), you can move funds to your debit card within minutes. While convenient, frequent use of instant transfers can eat into your savings. Understanding these fees is essential for maintaining liquidity without unnecessary costs.

2. Navigating Venmo for Business and Side Hustles

As the gig economy grows, Venmo has expanded beyond social payments to become a viable tool for entrepreneurs and freelancers. However, using the platform for business requires a different set of rules and financial rigor.

Personal vs. Business Profiles

Venmo now offers formal Business Profiles. While it may be tempting to use a personal account for your side hustle to avoid fees, doing so violates Venmo’s Terms of Service and risks account suspension. A Business Profile allows you to accept payments for goods and services, provides you with professional tax documentation, and offers increased visibility through the app’s social feed. The trade-off is a transaction fee (currently 1.9% plus $0.10), which should be factored into your pricing strategy.

Understanding Transaction Fees and Tax Compliance

The intersection of Venmo and the IRS is a critical area for any modern earner. Per current tax laws, Venmo and other P2P platforms are required to report gross payments for goods and services that exceed certain thresholds (previously $20,000, but moving toward a much lower $600 threshold under proposed regulations).

- The 1099-K Form: If you use a Business Profile or tag a transaction as “Goods and Services,” Venmo will track these payments. If you hit the threshold, you will receive a Form 1099-K.

- Bookkeeping: For the savvy business owner, Venmo’s transaction history serves as a digital ledger. It is vital to categorize these payments immediately to simplify your end-of-year tax filings.

The “Goods and Services” Protection

When you send money to a stranger for a product—say, a vintage camera from a social media marketplace—Venmo offers a “Purchase Protection” feature. By toggling the “Turn on for purchases” button, the buyer is covered if the item is not as described. The seller pays a small fee for this, similar to a credit card processing fee. From a financial security standpoint, this feature is indispensable for mitigating the risks associated with online commerce.

3. Advanced Financial Features and the Venmo Ecosystem

Venmo has evolved into a comprehensive financial ecosystem, offering products that rival traditional banking services. For users looking to consolidate their financial life, these tools offer both convenience and rewards.

The Venmo Debit and Credit Card Rewards Program

Venmo offers two distinct physical cards that link directly to your account.

- Venmo Mastercard Debit: This card allows you to spend your Venmo balance anywhere Mastercard is accepted in the U.S. It also offers “cashback” at select retailers, which is automatically deposited back into your Venmo account.

- Venmo Visa Credit Card: This is where Venmo enters the realm of strategic credit management. The card features a tiered rewards system: 3% back on your top spend category, 2% on the second, and 1% on everything else. Categories include groceries, dining, and bills. For a household that spends heavily in one specific area, this card can be a powerful tool for earning passive income on necessary expenses.

Investing in Cryptocurrency Through the App

In an effort to democratize finance, Venmo integrated cryptocurrency trading into its platform. Users can buy, sell, and hold Bitcoin, Ethereum, Litecoin, and Bitcoin Cash for as little as $1.

- Financial Insight: While convenient, users should be aware of the spread and transaction fees associated with in-app crypto purchases. Furthermore, unlike a dedicated cold wallet, Venmo holds the keys to your crypto. For the casual investor looking to diversify their portfolio with small amounts of digital assets, Venmo provides an accessible entry point.

The Social Feed and Financial Discretion

A unique, albeit controversial, feature of Venmo is its social feed. By default, transactions are often public, showing who you paid and for what (excluding the amount). From a financial privacy perspective, this is a significant concern. High-net-worth individuals and privacy-conscious users should navigate to settings to set their default privacy to “Private.” This ensures that your financial habits, connections, and lifestyle choices remain confidential.

4. Security and Financial Safeguards

In the digital age, financial security is synonymous with financial health. “Doing Venmo” correctly means protecting your assets from the myriad of scams and technical vulnerabilities that plague P2P platforms.

Protecting Your Balance from Scams

Venmo is a frequent target for “accidental payment” scams. A scammer might send you $500 using a stolen credit card, then message you claiming it was an accident and asking you to send it back. Once you send the money back, the original stolen transaction is reversed, leaving you out of your own funds.

- Best Practice: If a stranger sends you money “by mistake,” do not send it back manually. Instead, instruct them to contact Venmo support to reverse the transaction. This keeps you out of the middle of a fraudulent loop.

Multi-Factor Authentication (MFA) and Biometrics

To safeguard your linked bank accounts, enabling Multi-Factor Authentication is non-negotiable. Venmo allows for biometric locks (FaceID or Fingerprint) and PIN codes. In the event your phone is lost or stolen, these barriers are the only thing preventing a thief from draining your linked accounts.

Resolving Disputes and Customer Support

Unlike a credit card, where you can easily “chargeback” a transaction through your bank, Venmo transactions are generally considered final once sent to a friend. This “instant” nature is why Venmo should only be used with people you know and trust. For financial disputes involving a Business Profile or a “Purchase Protection” transaction, Venmo provides a dispute resolution center. Understanding the limitations of these protections is vital for managing your overall risk profile.

In conclusion, “how to do Venmo” is a question of intent. For the casual user, it is a convenient way to settle small debts. For the financially savvy, it is a sophisticated tool for managing cash flow, earning credit rewards, and even exploring the world of cryptocurrency. By understanding the fee structures, tax implications, and security protocols, you can ensure that Venmo serves as an asset to your financial well-being rather than a liability. As the line between social media and banking continues to blur, mastering these digital tools is the key to maintaining a healthy and modern financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.