In the contemporary landscape of personal finance, the transition from physical currency to digital liquidity is nearly complete. Peer-to-peer (P2P) payment platforms have evolved from niche conveniences into essential financial tools that dictate how we interact with friends, family, and businesses. At the forefront of this revolution is Venmo. Owned by PayPal, Venmo has transcended its status as a mere app to become a verb in our daily lexicon. However, setting up a Venmo account is more than just a technical hurdle; it is a foundational step in managing your digital footprint and financial security. This guide provides a professional deep dive into the nuances of establishing, securing, and optimizing a Venmo account within the modern financial ecosystem.

The Evolution of Peer-to-Peer Payments in Personal Finance

To understand why setting up a Venmo account correctly is vital, one must first recognize the role it plays in a broader financial strategy. P2P apps have effectively replaced the “IOU” of the past with instantaneous, trackable transactions. This shift has significant implications for how individuals track their spending, manage shared expenses, and maintain personal liquidity.

Why Venmo is a Staple in the Modern Financial Toolkit

Venmo’s primary appeal lies in its marriage of social connectivity and financial utility. Unlike traditional bank transfers, which can be cumbersome and slow, Venmo offers a streamlined interface that prioritizes speed. For the modern consumer, this means the ability to split a dinner bill, pay a roommate for rent, or contribute to a group gift in seconds. From a financial management perspective, it provides a digitized ledger of casual transactions that are often lost when using cash. By consolidating these small-scale exchanges into a single platform, users can gain a clearer picture of their discretionary spending habits.

Understanding the Security Infrastructure of Digital Wallets

When you set up a Venmo account, you are essentially opening a digital wallet that interfaces directly with your primary banking institutions. Therefore, understanding the security protocols is paramount. Venmo utilizes data encryption to protect user information and employs unauthorized-access safeguards. However, the “Money” niche demands a higher level of scrutiny. Users must recognize that while the platform is secure, the human element—such as falling for phishing scams or failing to set up proper authentication—remains the weakest link. Establishing your account with a “security-first” mindset is the only way to ensure your capital remains protected.

Step-by-Step Guide: Configuring Your Venmo Account for Maximum Utility

Setting up the account is a straightforward process, but there are several decision points that will affect your financial flexibility and the fees you may incur.

Initial Onboarding and Identity Verification

The process begins with downloading the app on a secure mobile device. You will be prompted to sign up using an email address or a mobile number. It is highly recommended to use a dedicated, secure email address that is protected by a strong, unique password.

Once the basic profile is created, Venmo will require identity verification. This is not merely a formality; it is a legal requirement under the USA PATRIOT Act, designed to prevent money laundering and fraud. You will likely need to provide your full legal name, date of birth, and the last four digits of your Social Security Number (SSN). For those intending to use Venmo for higher-volume transactions or to maintain a balance within the app, full identity verification is a prerequisite to unlocking the platform’s full suite of financial features.

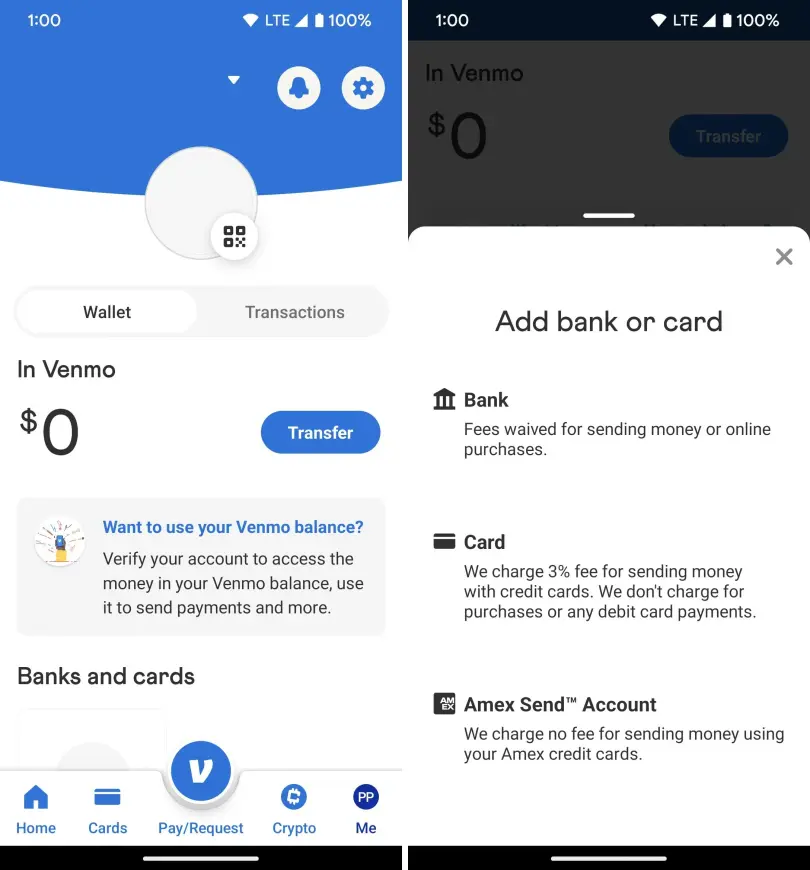

Linking Financial Institutions: Credit vs. Debit vs. Bank Accounts

This is the most critical stage of the setup process from a personal finance perspective. Venmo allows you to link three types of funding sources:

- Bank Accounts: Linking via ACH allows for the seamless movement of funds between your bank and Venmo. This is the most cost-effective method for “cashing out” your Venmo balance.

- Debit Cards: Linking a debit card usually provides the fastest way to fund payments without incurring the fees associated with credit cards.

- Credit Cards: While convenient, using a credit card on Venmo typically incurs a 3% transaction fee. Furthermore, some issuers may treat Venmo transfers as “cash advances,” which carry higher interest rates and immediate accrual.

From a strategic financial standpoint, linking a bank account or a debit card is the preferred method for standard P2P use to avoid unnecessary erosion of your capital through fees.

Optimizing Your Account for Financial Security and Privacy

A common oversight during the Venmo setup is neglecting the privacy and security settings. In the realm of personal finance, data privacy is synonymous with financial security.

Implementing Multi-Factor Authentication (MFA)

Once your account is live, your first priority should be enabling Multi-Factor Authentication (MFA). This requires a second form of verification—usually a code sent to your mobile device—before any login or significant transaction can occur. In an era where digital identity theft is rampant, MFA is your primary defense against unauthorized access to your linked bank accounts. Additionally, enabling biometric locks (FaceID or Fingerprint) on the app itself adds an extra layer of physical security should your device fall into the wrong hands.

Managing Social Privacy Settings to Protect Financial Data

Venmo is unique because of its social feed, which, by default, often makes transaction memos public. From a professional financial standpoint, broadcasting who you pay and when is a privacy risk. It can reveal your location, your spending habits, and your social circle to bad actors.

During setup, navigate to the Privacy menu and set your default transaction visibility to “Private.” This ensures that only you and the recipient can see the details of the exchange. Protecting your financial “metadata” is just as important as protecting the funds themselves.

Navigating Limits, Fees, and Tax Compliance

To use Venmo professionally and effectively, one must understand the regulatory and cost-based constraints of the platform.

Understanding Transaction Limits and the Verification Process

Unverified accounts have much lower rolling weekly spending limits (often around $299.99). Once you complete the identity verification process mentioned earlier, your limit for person-to-person payments can increase significantly, often up to $60,000 per week, though individual transaction limits may apply. Understanding these caps is essential if you plan to use the app for significant expenses, such as monthly rent or large-scale reimbursements.

The Impact of New Tax Laws (Form 1099-K) on Personal Users

A major shift in the “Money” niche recently involves the IRS reporting requirements for P2P apps. As of the current tax landscape, Venmo is required to report gross payments for goods and services that exceed a certain threshold (historically $600) via Form 1099-K.

It is crucial to distinguish between “Friends and Family” payments and “Goods and Services” payments. Payments marked as “Friends and Family” are not taxable, as they are considered personal gifts or reimbursements. However, if you are using Venmo for a side hustle or selling items, you must account for these as business transactions. Misclassifying these can lead to complications with the IRS or potential suspension of your account.

Leveraging Venmo for Advanced Personal Finance Management

Once the account is set up and secured, it can be integrated into your broader financial life as more than just a payment app.

Using Venmo for Budgeting and Shared Expenses

For couples or roommates, Venmo acts as a real-time ledger. By reviewing your transaction history, you can categorize shared expenses like utilities, groceries, and rent. Many modern budgeting apps, such as Mint or YNAB (You Need A Budget), can sync with your financial institutions to track Venmo transfers, allowing you to maintain a holistic view of your net worth and cash flow.

Exploring the Venmo Debit Card and Direct Deposit Options

For those looking to de-bank or streamline their finances, Venmo offers a Mastercard debit card and the ability to set up direct deposit. The Venmo Debit Card allows you to spend your Venmo balance directly at retailers, often providing cashback rewards at specific merchants.

Furthermore, using Venmo for direct deposit can sometimes allow users to access their paychecks up to two days early. While this can be a boon for liquidity management, financial experts suggest using this as a secondary tool rather than a replacement for a high-yield savings account, as Venmo balances typically do not accrue interest.

In conclusion, setting up a Venmo account is a foundational task in the modern digital economy. By approaching the process through the lens of professional finance—prioritizing security, understanding the implications of funding sources, and staying compliant with tax regulations—you transform a simple app into a powerful instrument for financial management. As the line between social interaction and financial transaction continues to blur, the disciplined use of tools like Venmo will remain a hallmark of the financially literate individual.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.