For many property owners, the arrival of a tax bill or a valuation notice in the mail can be a source of significant confusion. Terms like “assessed value,” “market value,” and “millage rates” are often used interchangeably in casual conversation, yet they represent distinct financial concepts that dictate how much you owe the government each year. Understanding the nuance between a tax assessment and property tax is not just a matter of semantics; it is a fundamental pillar of personal finance and real estate investment.

While they are two sides of the same coin, the assessment is the process of valuation, whereas the property tax is the actual levy or financial obligation. Navigating these waters effectively can lead to substantial savings and more accurate long-term financial planning.

The Fundamentals: Defining Tax Assessment and Property Tax

To master your property-related finances, you must first distinguish between the valuation of your asset and the tax applied to that valuation.

What is a Tax Assessment?

A tax assessment is a value assigned to a property by a local government official—usually a tax assessor—to determine the “taxable value” of the home or land. This assessment is not necessarily the same as the price you paid for the house or what a Realtor says it is worth today. Instead, it is a figure used specifically for the purpose of calculating local taxes.

Assessments are typically conducted on a cycle, which varies by jurisdiction. Some counties assess properties every year, while others may only do so every three to five years. The result of this process is the “assessed value,” which serves as the base for your tax bill.

What is Property Tax?

Property tax is an “ad valorem” tax, meaning it is levied according to the value of the asset. It is the actual dollar amount that a property owner must pay to their local government (city, county, or school district). These funds are the primary engine for local public services, including public schools, police and fire departments, road maintenance, and parks.

Unlike income tax, which is calculated based on what you earn, property tax is a wealth tax calculated based on what you own. It is an ongoing cost of ownership that persists even after a mortgage is paid in full.

The Core Relationship Between the Two

The relationship between the two can be expressed through a simple mathematical formula:

Assessed Value × Tax Rate (Millage) = Property Tax Bill.

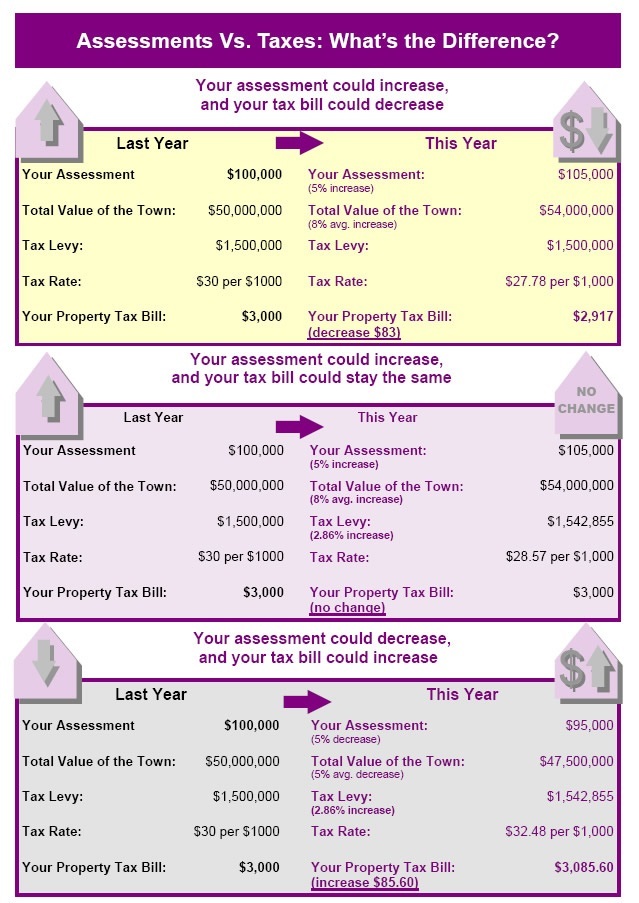

In this equation, the tax assessment provides the “input” (the value), and the property tax is the “output” (the cost). If your assessment goes up, your taxes will likely go up, even if the tax rate stays the same. Conversely, if the local government raises the tax rate, your bill will increase even if your assessment remains stagnant.

How Tax Assessments are Calculated

The process of determining a property’s assessed value is a systematic approach handled by the municipal or county assessor’s office. They use several methodologies to ensure the valuation is as fair and equitable as possible.

The Role of the Tax Assessor

The tax assessor is a government official responsible for maintaining a database of all properties within a jurisdiction and assigning them a value. They do not set the tax rates; their job is purely one of discovery and valuation. They look at property descriptions, deed transfers, and physical characteristics of the land and improvements to build a “tax roll.”

Valuation Methods: Market, Cost, and Income

Assessors generally use one of three approaches to determine value:

- Sales Comparison (Market) Approach: This is the most common method for residential real estate. The assessor looks at “comps”—similar properties in your neighborhood that have sold recently. They adjust for differences in square footage, number of bedrooms, and amenities.

- Cost Approach: This method calculates what it would cost to replace the structure from scratch, including labor and materials, minus depreciation. This is often used for new constructions or unique properties where comps are scarce.

- Income Approach: Primarily used for commercial properties and apartment complexes, this method determines value based on the income the property is expected to generate for the owner.

Assessment Ratios and Fair Market Value

It is a common misconception that the assessed value equals the fair market value. In many jurisdictions, the law requires an “assessment ratio.” For example, if your home’s market value is $500,000 and the local assessment ratio is 80%, your assessed value is only $400,000. Understanding your local ratio is vital for determining if your property is over-assessed compared to your neighbors.

Determining Your Property Tax Bill

Once the assessment is finalized, the local government applies a tax rate to that value. This is where the financial burden is officially calculated.

Understanding Millage Rates

Property tax rates are often expressed in “mills.” One mill represents one-tenth of one percent, or $1 for every $1,000 of assessed value. If your municipality has a total millage rate of 20 mills, you would pay $20 for every $1,000 of your property’s assessed value.

Millage rates are cumulative. Your total bill usually includes separate mills for the county, the city, the local school board, and sometimes specific “taxing districts” for things like water management or library systems.

The Impact of Local Government Budgets

Tax rates are not arbitrary; they are driven by the budgetary needs of the community. Every year, local officials determine how much money is required to run public services. They then look at the total “tax base” (the sum of all assessed property values in the area) and set a tax rate that will generate the necessary revenue. This is why property taxes can increase even when property values are falling; if the town needs more money and the values are down, the rate must go up to compensate.

Exemptions and Abatements

One of the most effective ways to lower a property tax bill is through exemptions. Many states offer a “Homestead Exemption,” which reduces the taxable value of a primary residence. Other common exemptions include those for senior citizens, disabled veterans, or surviving spouses. Additionally, “tax abatements” are sometimes offered to developers or homeowners who renovate historic properties, freezing the tax level for a set number of years to encourage investment.

Key Differences and Why They Matter for Your Finances

Distinguishing between assessment and tax is critical for anyone managing a portfolio or a household budget.

Frequency of Updates vs. Annual Billing

A tax assessment is a periodic event. You might receive a notice of revaluation once every few years. However, property tax is an annual (or semi-annual) obligation. Because these two cycles don’t always align, homeowners can be caught off guard. An assessment increase today might not manifest in your tax bill for another twelve months, leading to a “sticker shock” that can disrupt cash flow.

Control and Appeals

You generally cannot appeal your property tax rate, as that is set by elected officials through the public budget process. However, you can appeal your tax assessment. If you believe the assessor has overvalued your home or made a clerical error (such as listing four bedrooms when you only have three), you have a legal right to challenge the assessment. Successfully lowering your assessment is the most direct way to lower your tax bill permanently.

Impact on Real Estate Investment Strategy

For real estate investors, the distinction is vital for calculating Net Operating Income (NOI). When analyzing a potential rental property, looking at the current owner’s property tax bill is often misleading. If the property is sold, it may trigger a “point-of-sale” reassessment, where the tax office updates the value to the new purchase price. Investors who fail to account for the gap between the old assessment and the new one often find their profit margins squeezed by a much higher tax bill in year two of ownership.

Strategies to Manage and Lower Your Tax Burden

Because property taxes are often the largest recurring expense of homeownership after the mortgage, proactive management is essential.

Navigating the Appeals Process

If your assessment arrives and it seems higher than the actual market value of your home, you should consider a formal appeal. This usually involves:

- Reviewing the “comparables” used by the assessor.

- Providing evidence of damage or structural issues that lower the value.

- Presenting a recent independent appraisal.

Most jurisdictions have a strict 30-to-60-day window following a new assessment to file an appeal, so timing is everything.

Auditing Your Property Record Card

Every assessor’s office maintains a “property record card” for your home. This document contains the data used to calculate your value. Errors are surprisingly common—incorrect square footage, the presence of a finished basement that doesn’t exist, or an incorrect lot size. Correcting these errors is often the easiest path to a lower assessment without needing a full formal hearing.

Long-term Financial Planning

For those on a fixed income or investors managing multiple doors, property taxes must be forecasted. By staying aware of upcoming local bond referendums (which often increase millage rates for new schools or infrastructure) and the local assessment cycle, you can build a more resilient financial plan. Always assume that property taxes will rise by 2-3% annually in your projections, but be prepared for larger jumps following a city-wide revaluation.

By understanding the mechanics of tax assessments versus the reality of the property tax bill, you move from being a passive payer to an active manager of your real estate assets. Knowledge of this distinction is the first step toward ensuring you pay your fair share—and not a penny more.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.